Today we compare major trading blocs to the global equity market ACWI to spot spaces that are relatively cheaper. Why? Capital flows usually tilt towards relatively cheaper spaces, especially if a macro market swing-low formation takes hold, says Ziad Jasani.

Ziad’s market strategy videos recorded Monday:

Recorded: April 23, 11 am-12 pm

Duration: 1:13:09

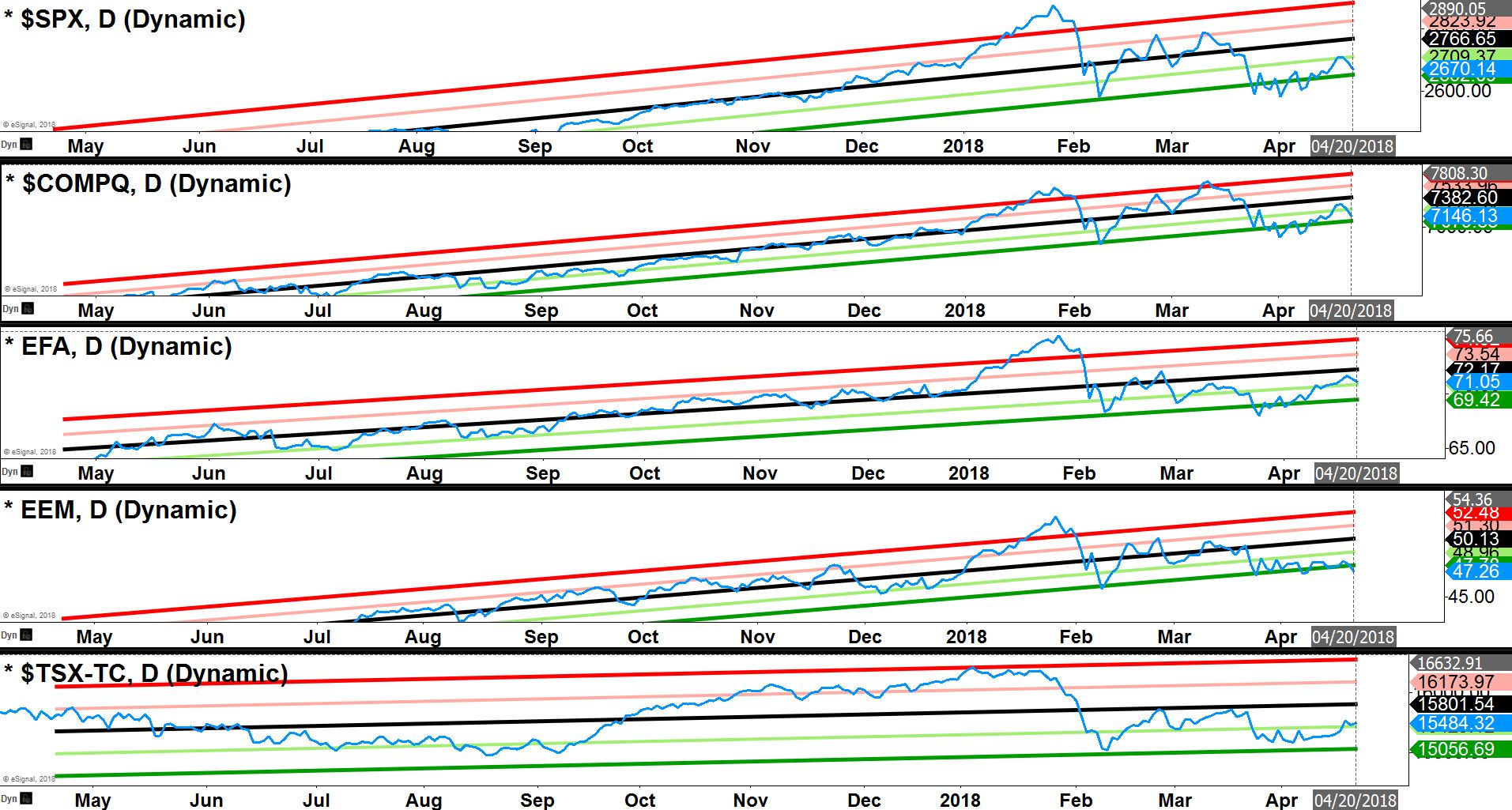

Major Index Direct Price Regression

When humans move very far away from normal routines they tend to come back home. In Markets, we call this “mean-reversion.”

Currently, every major trading bloc presents ~2 standard deviations away (near the green line or cheap) from their normal annual routines (black line in channels). This presentation supports a macro market swing-low formation advancing in the week ahead and pointing each space to their respective homes (black-lines at middle of channel).

But if we end the week below 2 standard deviations cheap, we may be entering the “new-normal” of Correction-Part 2; early signal = S&P 500 < 200-day average.

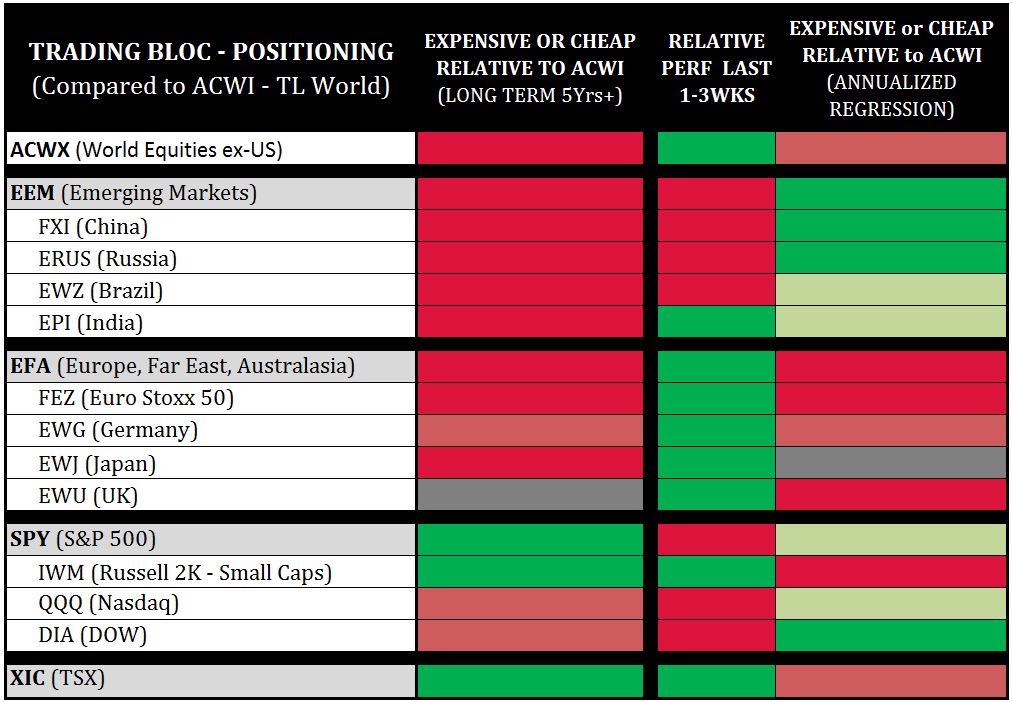

Trading Bloc Positioning

This chart compares major trading blocs back to the entire global equity market (ACWI) to determine which spaces are relatively cheaper.

Why? Capital flows usually tilt towards relatively cheaper spaces, especially if a macro market swing-low formation takes hold.

US Markets: S&P 500 (SPY), Dow (DIA) & Nasdaq (QQQ) present as the strongest opportunity areas, followed by Emerging Markets (EEM), China (FXI), India (EPI) and Brazil (EWZ).

The TSX presents as 1 standard deviation expensive, which implies that if the macro market swing-low advances this week the TSX is likely to under-pace the world.

Since the late Jan.-early Feb. 2018 market correction has resolved to markets (ACWI, SPY) coming back down to their 200-day averages but left in bounce formation from April 6 we are in swing-trading mode with our short-to-mid-term capital and remain Hold with our longer-term holdings.

View the Independent Investor Institute trading ideas and strategies videos here.