The equity markets are starting the week off with a positive tone thanks to trade deal progress over the weekend. Gold and silver are a bit lower, while crude oil is higher. The dollar is popping, but Treasuries are taking on water.

The US and European Union reached a trade deal in Scotland over the weekend, one that will result in EU exporters paying 15% tariffs (rather than up to 50%) on most products. Tariffs on many US exports to Europe will drop to zero. The EU is the US’ biggest trading partner, with just over 20% – or about $303 billion – of total imports coming from the bloc in the first five months of 2025.

Some European countries complained the deal was too generous to the US. But markets on both sides of the Atlantic rallied because worst-case outcomes were averted. Meanwhile, negotiators from the US and China are meeting in Stockholm this week. The gathering will likely result in another 90-day pause on new cross-border tariffs, one designed to give both sides more time to talk. The previous extension runs through Aug. 12.

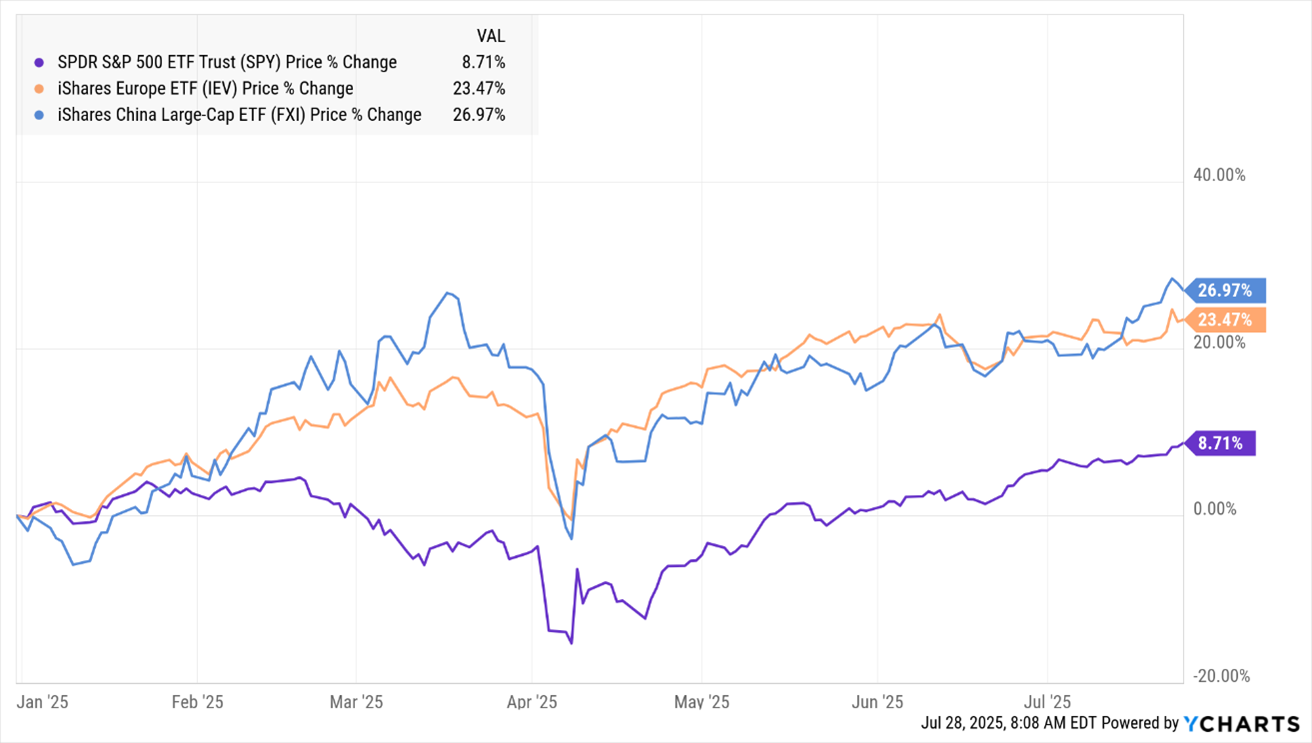

The iShares Europe ETF (IEV) and iShares China Large-Cap ETF (FXI) are handily outperforming the SPDR S&P 500 ETF (SPY) in 2025, as you can see in this chart.

SPY, IEV, FXI (YTD % Change)

Data by YCharts

The Federal Reserve will meet this week to discuss interest rates, with a decision to be announced Wednesday afternoon. Despite heavy pressure from the White House, Chairman Jay Powell & Co. will almost certainly NOT cut rates this week. But Powell could hint that cuts are coming soon. The final three Fed meetings of 2025 conclude on Sept. 17, Oct. 29, and Dec. 10.

Finally, Tesla Inc. (TSLA) and Samsung Electronics Co. just inked a $16.5 billion, multi-year semiconductor production deal. Samsung will supply Tesla’s next-generation AI6 chip from a new factory in Texas, a major step in Samsung’s quest to catch up to industry leader Taiwan Semiconductor Manufacturing (TSM). Samsung shares jumped almost 7% on the news.