ESG is growing in prominence in the investment world. The term refers to the incorporation of “environmental, social, and governance” factors into investment analysis, notes Monty Guild of in Guild Investment Global Market Commentary.

ESG analysis gives interested investors a window into companies’ behavior and its wider impact in areas that they care about.

In order to align their investment strategy with their values, a growing number of investors want to know more about the environmental impact of the companies in which they invest; how these companies address social issues that are of concern to them; and whether their governance practices are fair and transparent.

All of these are, in our view, laudable goals. Throughout Guild’s history, a number of our clients have held strong convictions that have led them to avoid investing in industries that they believed were reprehensible (for example, companies in the tobacco, alcohol, genetic modification, and biotechnology areas, as well as others).

“Values-based investing” has been part of our firm’s culture for many decades, and we have always adapted to client requests to avoid certain industries. There are no investment decisions wholly separate from an investor’s wider values and convictions.

Put another way, an investment portfolio is the fruit of a lot of life effort — so if it’s put to work, it makes sense that an investor would want it to be put to work at things they value and believe in.

Still, we think it’s important to distinguish that alignment of broader values from the analysis of investment performance. These are two separate spheres that should not be conflated.

Often, there may be a trade-off. Incorporating ESG into investment selection might lead an investor to narrow their portfolio options to a degree that reduces its performance. They may be happy with that outcome — but they should be clear-eyed about the decision they’re making.

Is ESG Outperformance Just A Happy Accident?

Increasingly, though, as ESG gets more mainstream, analysts are working on teasing out the broader effects of ESG characteristics on companies’ economic performance and on the performance of their stocks.

We’re skeptical of some of this research. One reason is that large companies, particularly in growth sectors of the economy such as technology, have the resources, the motivation, and the pre-existing corporate culture to ensure that their ESG rankings are high.

Thus, many ESG-focused funds end up looking almost identical to any plain-vanilla big-cap growth fund. In these cases, the ESG angle seems like little more than an excuse for the funds to sport a higher expense ratio. For example, three of the largest holdings of the ESG Leaders Equity ETF (USSG) are Microsoft (MSFT), Alphabet (GOOG), and Visa (V).

Other surprises sometimes await investors in ESG funds; we’ve noticed that some of them have significant allocations to major oil companies (which can rank high in governance metrics, and can also work hard to improve their environmental metrics as measured by the funds’ architects).

Investors considering such funds should look carefully at their holdings, and not just take the “ESG” label at face value.

Studies showing overall ESG outperformance may therefore be little more than a statistical artifact of the fact that ESG has risen in prominence during a bull market in which big-cap growth has relentlessly outperformed — and investors who jump on that bandwagon may be disappointed in the next downturn, or change of trend.

None of this is to say that investors shouldn’t use newly available ESG data to help inform their investment decisions. But they should scrutinize performance as carefully here as anywhere else, and make their decisions on the basis of a sober, overall view of costs and benefits.

Gender Diversity

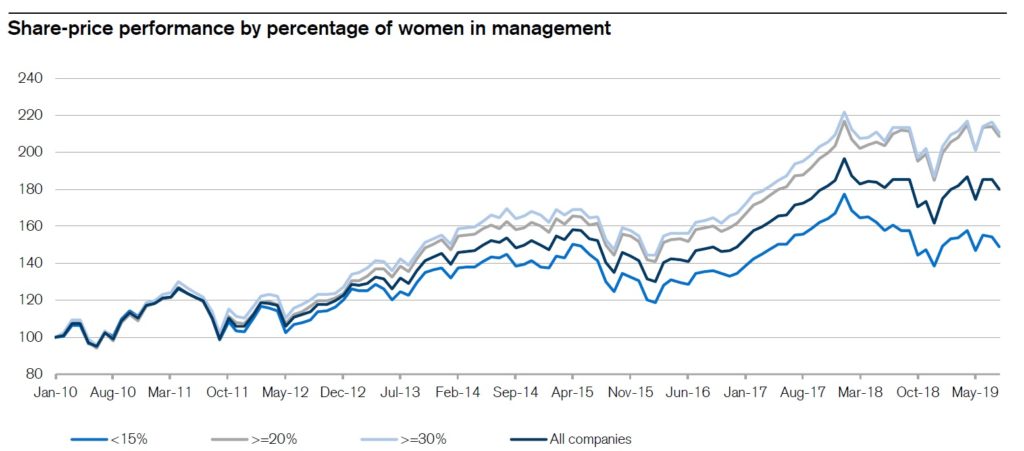

One area of particular topical interest to many investors is gender diversity on company boards and in executive managerial positions.

While many ESG criteria involve subjectivity in the selection of the metrics they track, and are more amenable to “gaming” by companies inclined that way, this one is a little more direct and neutral.

Credit Suisse analysts recently published an annual update to their study of gender representation dynamics in company governance; the upshot is interesting. In essence, companies with higher gender diversity in governance — and especially, higher gender diversity in the “C suite” of upper-level executive positions — tend to rank higher than average in measures of “quality.”

Quality refers to an investment factor that reflects a company’s fundamental strengths — low debt, stable earnings, and consistent asset growth, as reflected in fundamentals such as return to equity, debt to equity, and earnings variability.

In turn, that higher quality ranking does seem to correlate with better overall performance for the equities of these companies.

Of course, as the Credit Suisse analysts observed, this is a case where correlation has been established — but not causation. Do companies with more gender diverse managements have better quality characteristics, and therefore better stock performance? Or — do companies with better quality characteristics tend to have more gender diverse managements? The data don’t allow us to say which way the influence runs.

However, while this may matter to management as it tries to decide whether to push hard for more gender diversity in management, distinguishing “correlation” and “causation” is not as important for investors. Correlation is enough.

On the basis of these data, we can safely include management gender diversity as one sensible, data-grounded metric to use when evaluating a company’s quality — and that’s a primary component of evaluating the potential for the future appreciation of its stock.

Are there likely confounding data included here? Certainly — which is why we never look at a result like this in isolation. But this does seem to be an area where the ESG case may have some hard economic backing, and where there may be scope for investors to include their values without sacrificing performance.

Investment implications: Environmental, social, and governance characteristics are becoming more prominent in investors’ decision making. We caution that investors should carefully and critically examine suggestions that these metrics in themselves lead to outperformance.

However, some recent data suggest that greater gender diversity in management is correlated with higher quality characteristics and in turn with an edge in stock performance. This is one governance metric that performance-focused investors can intelligently include in their analysis toolkit.

Subscribe to Guild Investment Global Market Commentary here…