The stock market has shown resilience, but risks clearly remain as the economic recovery may not happen as quickly as investors expect, cautions George Putnam, editor of The Turnaround Letter.

Convertible bonds and convertible preferred stocks can provide investors with possible participation in future gains in the underlying common stock, along with attractive yields, while providing some measure of downside protection.

Because each security is convertible into a specified number of common shares, if the common stock goes up, the convertible security will trade up as well.

Downside protection comes from the securities’ cash coupons and seniority in the capital structure. Unless the issuer defaults, the holder of the convertible will be paid at least the security’s face value at maturity even if the stock has not risen.

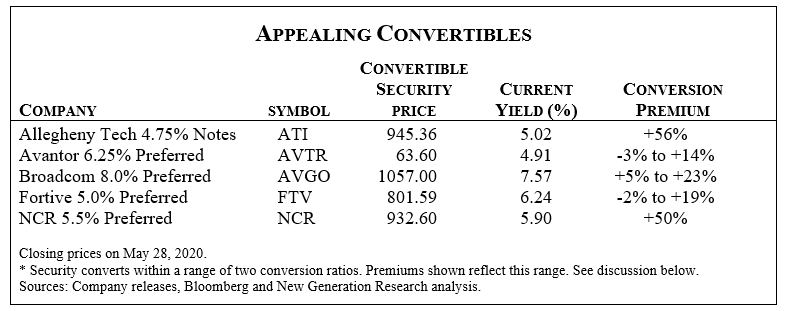

Listed below are five interesting convertible securities with relatively high yields.

Allegheny Technologies 4.75% Convertible Senior Notes due July 2022

Allegheny Technologies (ATI) is a producer of specialty metals including titanium and stainless steel. With over 70% of its revenues coming from the commercial jet market, Allegheny’s prospects have weakened along with aircraft demand.

However, it is likely to generate free cash flow this year, has a manageable amount of debt and will eventually participate in the industry’s recovery.

The convertible notes mature at par in two years, offering 20% upside, even if the stock doesn’t rise, as well as an attractive yield. If the stock rallies to about $14.50, the bond will begin trading as a stock, providing further upside potential.

Avantor 6.25% Series A Mandatory Convertible Preferred Stock

Avantor (AVTR) has a valuable niche as a provider of materials, consumables and related equipment and services to biopharma, healthcare and advanced materials companies.

In May 2019, Avantor completed a $2.9 billion initial public offering at $14. The preferred shares offer an appealing 5% yield (compared to no yield for its common shares).

Holders will have their preferred shares automatically convert the $50 in liquidation preference (or, face value) into either 3.04 or 3.57 common shares in May 2022.

With Avantor’s steady growth prospects, these preferred shares offer investors an opportunity to participate in the common stock’s upside while enjoying a generous yield.

Broadcom 8.0% Series A Mandatory Convertible Preferred Stock

Broadcom (AVGO) designs and produces semiconductors, network infrastructure and software. It purchased the corporate security operations of Symantec for $10.7 billion in 2019.

The convertible’s high yield is appealing when compared to the 4.6% yield on the common stocks. Holders will need to convert the $1,000 in face value by September 2022, with the conversion ratio ranging between 3.03 and 3.54 shares.

Fortive 5.0% Series A Mandatory Convertible Preferred Stock

Fortive (FTV) was spun-off from Danaher Corporation in 2016. The company acquires attractive businesses in a diverse range of industries, using a successful capital allocation strategy and the “Danaher Business System” that focuses on quality, cost and other key performance metrics.

Due to Covid-19, Fortive has delayed two planned spin-offs. The preferred shares convert in July 2021 into between 10.90 and 13.33 shares of common stock. With the company’s attractive long-term future, these convertibles offer a good yield plus participation upon conversion.

NCR 5.5% Series A Convertible Preferred Stock

NCR (NCR) produces bank ATM machines and providing related services, may be temporarily weakened but should eventually recover.

NCR’s convertible preferred shares offer an interesting way to participate, partly by paying a superior dividend yield to the common (which pays no dividend). Holders may convert the securities into 33.3 common shares at their option, with no time limit, providing plenty of time to wait.

Supporting the value, and the high 50% conversion premium, is the right that holders have to redeem the convertibles at the $1,000 face value after March 2024.