Copper is shaping up to be an unlikely star that’s set to be an investment favorite for 2021 and beyond, suggests Genia Turanova, editor of Moneyflow Trader.

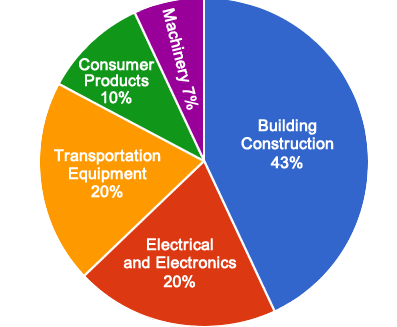

This old-school metal has been used for centuries for everything from plumbing to wiring to machinery… but besides its traditional uses, it now plays a key role in growing industries like renewable energies and electric vehicles (EVs)—including yet-to-be-built charging station infrastructure.

But copper is facing a supply shortage… just when its use for renewable power generation, electric infrastructure, and decarbonization of the economy is on the rise.

Based on copper’s role in power transmission and EVs, it’s estimated that its price could rally 60% more by 2025. Now is the time to start building a position in the metal.

The management team of one of the largest Canada’s mining companies, Teck Resources (TECK), shares this outlook. And it’s getting ready to deliver more copper to the market.

Teck possesses a unique advantage: It owns a copper mine with huge reserves. This mine is more than half completed, and is located in Chile—one of the healthiest countries in resource-rich Latin America. This means it’s close to production… which is a big deal.

With a limited supply of copper available… and copper prices on the rise… the mine closest to completion will win, as will its owners. This is the main reason I like Teck Resources (formerly Teck Cominco).

It’s not just a copper play. It’s a growingcopper play, set to benefit from both higher prices and higher volumes as it brings new projects online. Teck Resources owns the Quebrada Blanca, a large copper deposit in Chile and the world’s largest undeveloped copper project.

Phase 2 of this project (known simply as QB2) is a huge mine just a few months away from completion. It has low operating costs and an expected lifespan of 28 years (longer than most mines).

Analysts expect as much as 19% per-share profit growth for the next few years. Meanwhile, TECK trades some 23% below its recent highs… and is cheaper than its pure-play copper peers.

This discount is especially huge in terms of price-to-tangible book value; TECK trades at less than 1x this value

I think Teck will narrow this discount significantly as soon as progress with QB2 is confirmed and the company’s higher copper exposure gets priced in.

Together with strong copper prices, this could double the stock within a couple of years. Shorter term, I expect a 30%-plus gain and a run above the recent highs of $26.25.