The attack on Israel generated a global reaction of shock, disdain, and compassion. Secondarily, investors wondered how this regional conflagration might affect the global economy in general and stocks in particular, says Sam Stovall, chief investment strategist at CFRA Research.

Since WWII, selected military shocks resulted in average declines for the S&P 500 one, seven, and 30 days after the event as a result of the initial surprise and uncertainly. Stocks then recovered 60 days and beyond, after realizing that the fallout from most events would be localized.

However, there have been several instances that triggered or exacerbated US recessions and bear markets, such as the Yom Kippur War in 1973 and Iraq’s invasion of Kuwait in 1990. Add to this the concern from recent inflation reports and the Q3 2023 EPS reporting period and one can understand why investors may think stock price gains could stall.

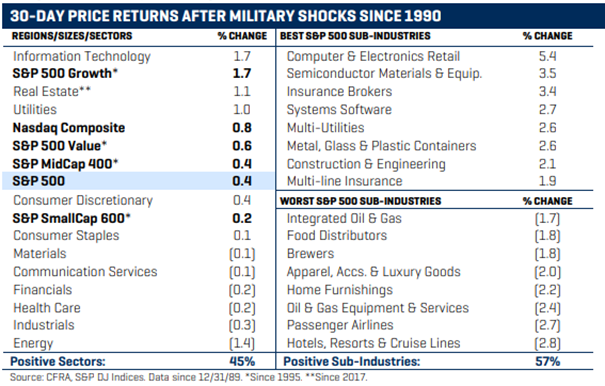

However, in the week through October 12, the S&P 500 was still up 1.0%, along with all sizes, styles, eight of 11 sectors, and 61% of the 153 subindustries in the S&P 1500. Since 1990, the S&P 500 treaded water during the first 30 days following 12 selected shocks, gaining an average of 0.4%, and accompanied by gains for all sizes, styles, and five of 11 sectors.

Not surprisingly, the energy sector posted the weakest average 30-day performance due to the potential disruption of global oil supplies. Conversely, technology held up best, possibly reflecting companies’ and countries’ ongoing desire to improve their preparedness.

On a subindustry level, a slight majority of groups went on to post advances, with a cross section of areas being embraced, while airlines, hotels, and oil were shunned.