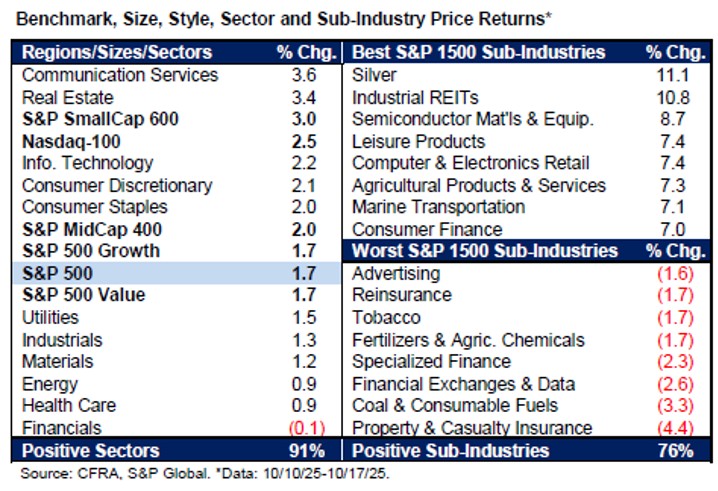

October is living up to its reputation as the most volatile month of the year. Indeed, since 1945, the standard deviation of monthly returns for the S&P 500 Index (^SPX) has been 33% greater than the average for the other 11 months of the year, writes Sam Stovall, chief investment strategist at CFRA Research.

Much of this volatility has been seen in the past two weeks. After enduring a near-3% single-day sell-off in response to President Trump’s Tweet threatening to add an additional 100% trade tariff to China’s existing tariffs, equity markets rebounded nearly 2%. The catalysts: Stronger-than-expected large bank top-line and bottom-line beats, additional AI alliances, and improvements in trucking results.

(Editor’s Note: Sam will be speaking at the 2025 MoneyShow Masters Symposium Sarasota, scheduled for Dec. 1-3. Click HERE to register.)

However, like a tongue and a loose tooth, investors quickly became obsessed with a handful of regional banks that announced write-downs on bad loans, resulting in a sharp, one-day stint of profit-taking. All that reversed on Friday, Oct. 17, as six regional banks within the S&P 500 posted better-than-expected results, with most also reporting strong credit quality.

What’s more, Q3 S&P 500 earnings growth forecasts on the whole were revised higher, according to S&P Capital IQ estimates. They’re now showing a 7.4% rise versus the 6.9% end-of-quarter projection. Stocks were also buoyed by Trump’s statement that the 100% additional tariffs on China’s imports were not sustainable.

Despite Friday’s recovery, Lowry Research, CFRA’s technical analysis arm, advises that “probabilities suggest that there is more time needed to digest the impressive gains made since the April low. Also, Lowry’s Market Health Score has backed down since last month’s peak but at +3 (down from +5 last week) it has only fallen to neutral. Therefore, investors are likely best served by staying in the market.”