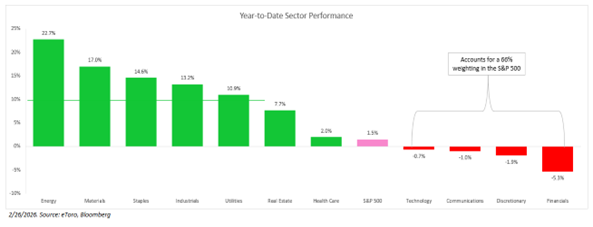

Many investors are scratching their heads over this year’s dispersion trade, but market bifurcation cuts both ways. In 2026, ten of the 11 S&P 500 Index (^SPX) sectors are expected to post positive earnings growth, with energy being the wildcard. That kind of broadening — with price action improving across sectors — is constructive, suggests Bret Kenwell, US investment analyst at eToro US.

In other words, this isn’t a market where just seven to ten stocks are doing most of the heavy lifting, like we saw in 2023. The catch is that laggards can still dominate the index. Even with five sectors already up more than 10% year to date, the S&P 500 is still hovering around flat because four sectors — tech, communications, discretionary, and financials — are down on the year. Together, they account for roughly two-thirds of the index’s weight.

Opportunity may be emerging in wide-moat industries — especially outside of software — that look less vulnerable to AI disruption. We’ve seen notable drawdowns in credit card networks, cybersecurity, rating agencies, stock exchanges, trucking and logistics operators, and travel booking platforms. Yet the “disruption” is still more theoretical than tangible, and in many cases earnings and revenue forecasts remain stable or continue to trend higher.

Within those pockets, several names have been dragged lower on AI fears. But many of these companies are more likely to be AI winners than AI losers — even if the last few weeks of price action have implied otherwise.

One risk no one seems to be talking about: Even if these firms aren’t notably disrupted by AI, there could be a “vibe shift” on Wall Street that affects long-term valuations. If AI worries persist, investors may not be willing to pay the same valuation that these industries have previously commanded. A lower valuation — even amid an undisturbed business — still equates to a stock-price headwind and could draw out or limit an eventual rebound.