At the end of March, after the S&P 500 Index (^SPX) stumbled more than 9%, CFRA identified a likely turnaround in fortunes. The S&P 500 went on to record its second-best performance in April since 1945. What’s more, history now offers additional encouragement, highlights Sam Stovall, chief investment strategist at CFRA Research.

Q1 earnings growth, at 25%, is now twice as high as the March 31 projection, and full-year estimates are above the quarter-end forecast, with 10 of 11 sectors enjoying upward revisions to forecasts. Meanwhile, following the top 25 gains in April since WWII, the S&P 500 posted a further advance in May, rising 22 times (88%).

(Editor’s Note: Sam is speaking at our July 2026 MoneyShow Virtual Expo. Click HERE to register.)

In response, CFRA raised its 12-month target for the S&P 500 to 7,730 from 7,400, and a year-end 2026 level of 7,575. We stated that the forecast is “reinforced by resilient consumer spending, a stable labor market, an infrastructure renaissance, and AI-related investment that is beginning to translate into tangible revenue growth and productivity gains.”

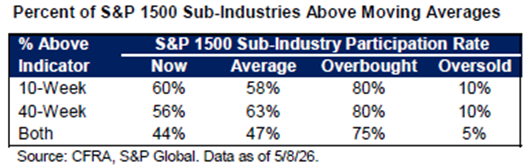

However, before a continuation of the current bull market run, the S&P 500 may need to take some time to catch its breath. As of May 6, the “500’s” Relative Strength Index (RSI is a popular technical momentum oscillator, in which a reading of 30 or lower is considered “oversold,” while 70 or higher is considered “overbought”) closed at 75 and was accompanied by overbought readings for the Nasdaq 100, Communication Services, and Information Technology sectors, as well as 9% of the 155 subindustries in the S&P 1,500.

CFRA thinks digestion of these recent gains would offer this bull the opportunity to “buy the dip” and resume its run. Finally, last week saw minor reductions in the percentages of the S&P 1,500 sub-industries trading above their 10- and 40-week moving averages, as well as above both averages. However, all three readings are still well below “overbought” levels.