Owning and operating a gold mine is expensive. Land rights, machinery, labor, permits and others expenses add up to hundreds of millions of dollars before the first nugget of gold is pried from the earth, states Jason Simpkins, editor of Outsider Club.

That’s why miners typically carry huge debt burdens. But what if you could avoid that whole mess? Streaming, or royalty, companies do.

Rather than spend billions on tools and labor, streaming companies make upfront payments to miners for the right to purchase silver and gold at cheap prices in the future.

Basically, they capitalize mines for a share of the spoils down the road. It’s a good business and three stocks, in particular, have proven that.

I’m talking about Wheaton Precious Metals (WPM), Franco-Nevada (FNV), and Royal Gold (RGLD). These three companies are the standard bearers of the streaming model. So let’s take a look at each.

Wheaton Precious Metals is the largest precious metals streaming company in the world. Though, you probably know it by its previous name, Silver Wheaton. The name change just went into effect to reflect the broadening of the company’s holdings.

While silver was the core of Wheaton’s business five years ago, the company has recently capitalized on streaming opportunities in gold to boost its revenue and add balance.

For example, Wheaton now claims 75% of the gold produced by Vale (VALE) at its Salobo mine in Brazil. It also paid Panoro $140 million in upfront cash for 25% of its gold production and 100% of its silver production from the Cotabambas Project in Peru.

Gold is currently trading at $1,259 per ounce, more than three-times Wheaton’s cost. And as the price of gold rises, its profit margins expand. The company is paying about $4 per ounce for silver, which is currently trading at $17 per ounce.

Over the next five years, Wheaton expects attributable output to be about 29 million ounces of silver and 340,000 ounces of gold per year.

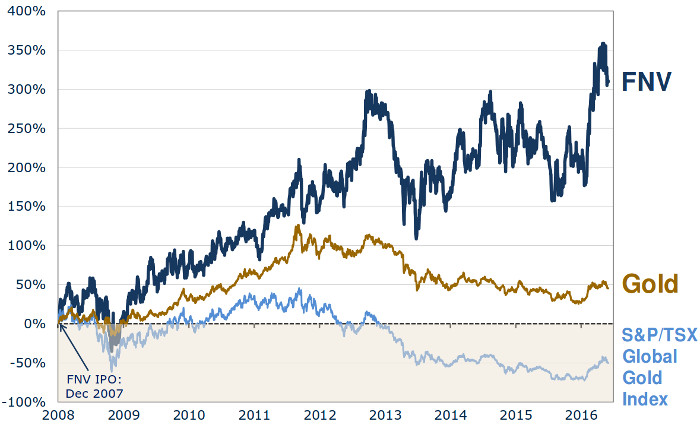

Meanwhile, Franco-Nevada is one of Wheaton’s biggest competitors. It, too, had a strong first quarter. FNV reported 131,578 gold equivalent ounces sold — a new record and a 23.4% increase year-over-year.

In addition, the firm reported record-high revenue, a 50% increase in net earnings, $283 million in cash, no debt, and a dividend increase. In 2016, Franco-Nevada's total purchase cost was just $105.8 million, compared to revenue of $610.2 million.

Looking at these results, it’s easy to see why FNV has greatly outperformed both gold and the broader stock market since its 2007 launch. It’s up 80% since August 2015.

Now, there’s something else interesting about FNV, too. Like Wheaton, it’s diversifying its holdings, but not by re-balancing its precious metals holdings. Instead, it’s adding more oil and gas to its portfolio.

This is a relatively new move that began back in December when Franco-Nevada acquired $100 million worth of oil and gas royalty rights in the Oklahoma STACK play. It followed that up in March, adding a portfolio of oil & gas royalties in the Midland shale play of the Permian Basin of Texas for $110 million.

Of course, 91.5% of the company’s revenue continues to come from precious metals. That’s 71.2% gold, 14.1% silver, and 6.2% platinum group metals. Just 5% is from oil and gas royalties.

Still, the company believes its oil and gas revenue could more than triple in the next decade. And at the same time, it expects to generate 515,000 to 540,000 gold equivalent ounces by 2021.

Finally, we have the last part of the triumvirate, Royal Gold, which scored one of its biggest hits in 2015, when it dropped $610 million on Barrick Gold (ABX).

In return, the streamer got significant interest in Barrick’s Pueblo Viejo mine. That included 7.5% of the gold produced until 990,000 ounces of gold are delivered, and 3.75% thereafter. And 75% of Barrick’s interest in the silver produced at Pueblo Viejo until 50 million ounces are delivered, and 37.5% thereafter.

In the most recent quarter, the firm recorded operating cash flow of $76.1 million, an increase of 15%, revenue of $107 million, an increase of 14%, and a 25% increase in profit.

Once again, we’re looking at a growing business with an excellent track record for dividend payouts. Indeed, Royal Gold has increased its dividend for 16 straight years, growing it at an annual compounded clip of 20% since 2001.

This is the kind of performance that led Royal’s stock to shoot up 4,265% in the 10-year period from 2001 to 2011.