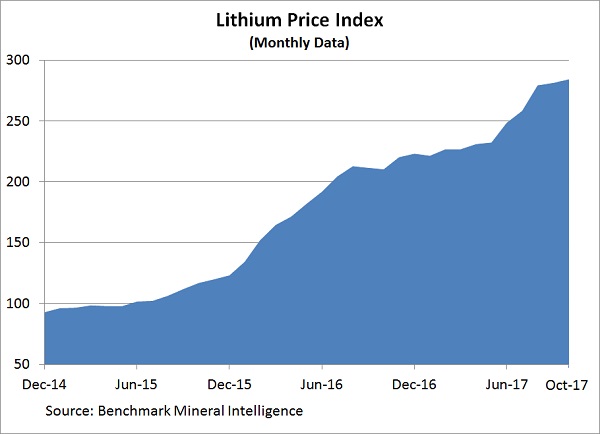

The robust growth of electric vehicles (EVs) continues to place high demand on lithium, which has led to healthy pricing conditions, asserts Scott Chan, editor Real World Investing.

Global EV sales through the first three quarters of the year were more than 764,000, 46% higher than last year’s pace. Total global sales for 2017 will likely surpass the one-million mark for the first time ever.

Concerns over China’s EV subsidy reforms have largely dissipated as the country’s EV demand proves its resiliency. Third-quarter EV sales growth was 49%, easily ahead of both Europe (39%) and the U.S. (31%). However, the uptake of EVs in the U.S. is accelerating, and that’s added to the global lithium demand.

The difference between the U.S. and China, however, is that while American companies don’t seem in a hurry to invest in lithium, Chinese companies are much more aggressive.

In particular, Beijing has instructed Chinese companies to hunt for lithium resources outside China. In the first-ever direct investment into a lithium supplier by an automaker, last September China’s Great Wall Motor purchased a small stake in Pilbara Mineral, an Australian lithium miner.

Additionally, Tianqi Lithium, China’s largest lithium miner, bought a 2% interest in a Chilean miner. And Ganfeng Lithium bought a 20% ownership in an Argentine project.

If China successfully expands control over the lithium supply chain, non-Chinese EV makers — such as the market darling Tesla (TSLA) — could find themselves experiencing difficulty procuring enough material to meet their production goals. They probably would have to pay high prices to acquire the necessary materials, which would put a crimp in profits.

Advertisement

We have avoided recommending Tesla due to our skepticism over its ability to achieve consistent profit growth. Instead, our recommended EV plays are Albemarle (ALB) and BYD Company (BYDDF).

Lithium miner Albemarle has enjoyed quite a strong 2017 so far. The share price has appreciated 57% year to date. BYD has been even better; the share price has rallied 86%.

ALB has rallied largely due to steadily rising lithium prices while BYD’s rally was sparked by the announcement that China plans to eventually phase out traditional cars completely.

Though China’s target for ending all production of fossil fuel cars is likely decades down the road, the long-term commitment overrides the subsidy concern from earlier in the year.

In the case of Albemarle, we do have a little concern about its shared ownership of a major lithium property in Western Australia with the aforementioned Tianqi. Albemarle owns 49% stake in the mining operations while Tianqi owns the majority 51%.

We think China wants as much control over essential materials, such as lithium, as they can, so we can’t rule out some Tianqi maneuver down the road to the detriment of Albemarle. But for now, Albemarle remains a strong recommendation.

We fully expect China to maintain clear leadership in electric vehicles. BYD, the top-selling EV maker in China (and the world) remains our favorite.