Western Asset Emerging Markets Debt Fund (EMD) holds 290 bonds issued by governments like Peru, Indonesia and Colombia. (How’s that for one-click diversification and convenience?) All together, the bonds pay an average of 6.4%, asserts Brett Owens, closed-end fund specialist and editor of Contrarian Outlook.

And it gets better, for two reasons. First, the closed-end fund (CEF) trades for just 90 cents on the dollar. This means that when we buy EMD, this 6.4% paying portfolio actually yields 7%+ (again, thanks to our 10% discount).

Plus, as a CEF, the fund can use leverage, which is a no-brainer when money is this cheap. EMD borrows at LIBOR (which is less than 2%) and plows the money back into its higher paying bonds. It uses prudent 24% leverage, which means it commands about $1.24 in bonds for every $1 in assets it owns.

The discount plus cheap money result in a fund that pays a sweet 8.5%. And our upside potential doesn’t stop there, because the bonds that EMD holds are rising in value, too. After paying its monthly distributions and management fees, the fund’s NAV increased more than 6% last year.

The demand for these types of bonds is heating up. EMD’s average holding doesn’t mature for another 10 years. As interest rates flatten, this fund’s 6.4% paying bonds look better and better. Currency risk is not a problem. The fund is hedged so it is “long” the same US dollars that you and I use to buy it.

This leaves the two main potential risks that we must always consider when buying bonds. The first is credit risk. We use CEF vehicles to buy these bonds because we want professional managers to evaluate this risk for us.

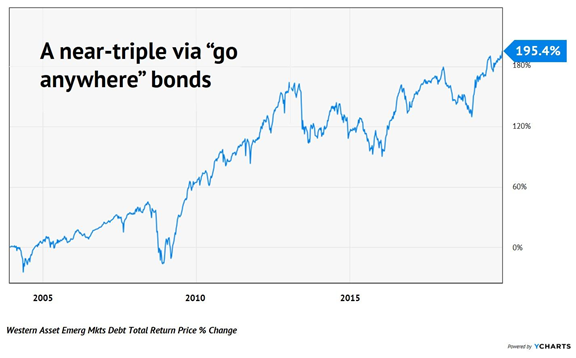

Their fees are “comped” thanks to the fund’s discount. They are also well earned as we can see from EMD’s historical performance. The fund has nearly tripled its investors’ money since inception.

Of course the ride hasn’t been perfectly smooth — which brings us to duration risk, the chance that interest rates move in a direction that works against us.

I believe EMD is well positioned for the year ahead, and that its 10-year average duration (its bonds’ time until maturity) is going to continue to be a big positive for its portfolio (as it was in 2019). The broader trend in interest rates is that they are heading lower. They’ve been sliding for nearly 40 years.

There is a lot of money out there in the world that is desperate for income right now. We can secure an 8.5% yield while setting ourselves up for gains, too, by buying EMD at a 10% discount. I don’t expect this deal to last for long, so let’s buy shares before they get snapped out of the bargain bin.