If there’s one overarching theme that’s accompanied the Trump rally, it’s the idea of reflation. In fact, if you look at the price action across nearly all asset classes, it reflects the anticipation of inflationary forces, observes Matthew Kerkhoff, editor of Dow Theory Letters.

But are we truly seeing the whites of inflation’s eyes? Or is this a temporary reprieve before deflationary forces again spoil the fun? The answer may be more complicated than you think.

To begin, let’s check in on where inflation currently sits. Using the Fed’s preferred measure, Personal Consumptions Expenditures (PCE), both headline and core (excluding food and energy) inflation levels are trending higher.

And for the first time in over two years, headline inflation is actually higher than core. Also note that both of these measures are bumping up against the 2% level, which is the Fed’s inflation target.

More and more economists are becoming convinced that the Fed has little control over inflation. Case in point: years of zero percent interest rates and trillions of dollars of quantitative easing have not been able to lift core inflation back to target.

In addition, the two primary factors that the Fed points to as drivers of inflation -- labor market slack and inflation expectations -- are now being questioned regarding their efficacy. If these factors are not the primary drivers of inflation, then what is?

Last week five top economists released a report prepared for the 2017 U.S. Monetary Policy Forum. The crux of this interesting paper is that we have less of an understanding of what truly drives inflation than we think.

The authors of the paper summarize their research by saying: "We find that the level of inflation fluctuates around a slowly changing trend that we call the local mean of inflation. Few variables add extra explanatory power for inflation once the local mean is taken into account. This local mean is itself well characterized by a random walk."

Those who have spent some time around financial markets should be familiar with the idea of a random walk, which basically suggests that the movements of an object or variable follow no discernible pattern. In other words, don’t bother trying to predict it, you might as well flip a coin.

The researchers go on to note that labor market slack (one of Janet Yellen’s favorite topics to discuss regarding the outlook for inflation) does have a statistically significant effect on inflation levels, but one that is “quantitatively small.” As for inflation expectations, according to the work of these economists, it plays no role whatsoever.

As someone who has a strong economics and psychology background, I must admit that these findings strike me as odd. The idea that inflation has very little predictability is one that appears anecdotally incorrect, but may be empirically spot on, at least if the researchers did their work properly.

While I tend to trust their analysis, I can’t help but be reminded of Warren Buffet’s advice, “Beware of geeks bearing formulas.”

Nevertheless, there is something to be learned from all research, and we must accept that our prior conceptions of what drives inflation could very well be incorrect. If that’s the case, where does that leave us? There must be somewhere we can look for an indication of how price levels will change.

Indeed there is. Historically, one of the better guides to inflation has actually been the movement in commodity prices. Go figure, right?

Changes in commodity prices often foretell changes in inflation (albeit with a lag), and we’ve seen this recently. Back in 2014, oil prices began to plunge, taking the entire commodity complex with it.

What happened shortly after that? You guessed it, headline inflation levels fell from nearly 2% to almost 0%, where they stayed for over a year. It wasn’t until oil and commodity prices began to rise at the beginning of 2016 that inflation finally began creeping higher.

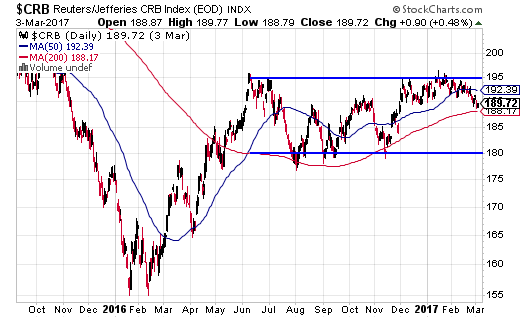

Since then, commodity prices have been in an upward trend, but that trend looks like it may be stalling out.

As you can see in the chart below, commodity prices have been range bound since mid-2016. During that period the 200-day moving average has acted as support on three separate occasions, with the fourth upon us now.

A failure to hold the 200-day MA line would be one of the first indications that the upward trend in commodity prices may be stalling. But either way, the directional break out of this channel will be the telling event.

If prices continue to rise, then the reflation trade is likely to continue. On the other hand, if commodity prices fall back into their prior downward trend, we could see a deflationary (or at least disinflationary) narrative return to the markets. In that event we’d likely see a reversal of the current price trends.

Wrapping things up, I want to circle back to this idea of predicting inflation levels. While we can link changes in headline inflation to things like commodity prices and perhaps developments in our economy (such as the financial crisis), this doesn’t really apply to core inflation.

Take another look at the light blue line in the top chart of this article. Notice that over the last 10 years, it has remained exceptionally constant, ranging from 1% to just over 2%. Now consider what we (and the economy) have gone through during that period:

* We saw one of the greatest and most unsustainable bubbles in home prices collapse.

* We saw trillions of dollars of wealth wiped out of the economy in the largest recession since the great depression.

* We saw the Fed bail out numerous institutions, drop interest rates to zero, and inject trillions of dollars of liquidity into the banking system.

* We saw oil go from over $140 per barrel down to less than $40 per barrel … twice.

* We saw the global economy nearly collapse, and central banks around the world took interest rates into negative territory.

* We also endured a raging bull market from 2009 on that has taken asset prices to all-time highs.

And all the while, core inflation remained constant, barely fluctuating more than a percent. If that doesn’t make you scratch your head, and reconsider the conclusions from the paper previously presented, I’m not sure what will.

All I can say at this point is that it’s clearly evident that we have much more to learn about how different variables interact in this complex web that we call an economy.