Stocks are having their best week in more than a year-and-a-half, with both domestic and global names on the rise. Treasuries, gold, and crude oil all got in on the fun yesterday, too.

Today, most equity and commodities markets are flat in the early going. Ditto for the dollar.

On the news front…

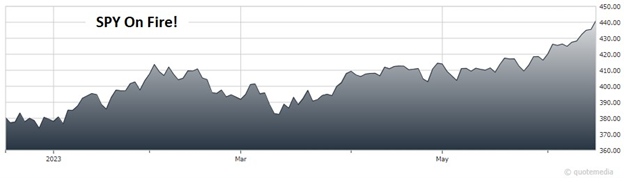

To put the recent run of market gains in perspective, the S&P 500 is on track for its longest stretch of positive days since November 2021. That’s assuming we close in the green today, of course.

Global stocks are having their best week in three months thanks to reports that China is going to open the stimulus taps again. The Wall Street Journal reports stimulus spending could total as much as 1 trillion yuan, or about $140 billion. The central bank there is also cutting interest rates.

If you heard my remarks at our Global Portfolio Strategy Summit in New York back in February...or our MoneyShow/TradersEXPO Las Vegas in April...you know I’ve been advocating a “Be Bold” approach to investing this year. That followed a year-and-a-half where my best advice was “Be Boring”.

Specifically, I’ve been recommending a more aggressive approach to picking assets, sectors, and individual stocks or ETFs to invest in – and putting more cash to work “bargain hunting.” That strategy has paid off so far in 2023 and I believe it will continue to do so in the second half of the year, too.

After a long drought for Initial Public Offerings, the Mediterranean restaurant chain Cava Group (CAVA) sold stock for the first time on Thursday – and got a gangbuster result! The firm sold 14.4 million shares at $22. But they opened trading at $42, and ultimately closed the day up 99%.

A few more successful offerings like that will bring investors back into the market, allowing more companies to raise money via the IPO process. On the flip side, banks are continuing to lend more cautiously amid worries about credit quality in Commercial Real Estate (CRE) and other sectors. That means the overall financing environment is tighter than it was several months ago.