The high-flying tech sector has been under pressure in September. We view the increased exposure to Apple and Microsoft, with their strong cash flow and potential for upside to consensus estimates as a positive for the group into year end, writes Lindsey Bell Thursday.

While September has been a notoriously weak month for the market in general, the downward move in tech (-2.3%) has far outpaced the S&P 500 (SPX) decline (-0.4%) and the performance of the ten other sectors in the index.

Semiconductor stocks and some of the FANG stocks, notably Facebook (FB) and Google’s parent, Alphabet (GOOG), have been the primary source of the weakness.

To be sure, there are fundamental issues in the semiconductor space that have picked up momentum in the past week, from a supply and demand mismatch in memory chips, to a slowdown in higher growth end markets, like automotive.

But to say the party is over for the entire tech sector would be premature in our view, especially ahead of a major change in the construction of the sector.

In large part, the future of tech (and maybe the market?) has come into question with the loss of market leadership from the headline-grabbing FANG stocks as summer got underway.

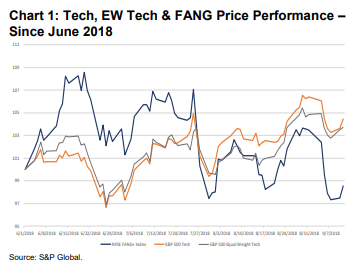

In Chart 1, the blue line shows the NYSE FANG+ index is 1.5% lower since June 1 (at 98.5, where the June 1 starting point is indexed to 100 for comparison purposes).

The FANG+ index has lost 10 percentage points since its June 20 high. To be fair, this index includes more than just the traditional FANG stocks. Apple (AAPL), Alibaba (BABA), Baidu (BIDU), Nvidia (NVDA), Tesla (TSLA) and Twitter (TWTR) are also included in the index’s calculation.

Still, since June 20, Facebook has declined 17.9%, Netflix (NFLX) is 14.6% lower and Alphabet is only 0.6% higher.

What is most notable in Chart 1 is the performance of the S&P 500 technology sector (the orange line). Although the sector’s performance has been affected by some of the heavyweight FANG stocks (Amazon and Netflix are in the consumer discretionary sector), since late July the broader tech sector has outperformed the FANG+ index, gaining 1.2% while FANG+ lost 5.4%.

The combined strength from the technology hardware industry, with Apple as its largest constituent by market capitalization, and software companies Microsoft (MSFT), Oracle (ORCL) and salesforce.com (CRM) helped to offset the declines in Facebook, Alphabet and the semiconductors, pushing the S&P 500 tech sector higher over the summer period.

In Chart 1, the trend for the orange line is clearly upward, while the blue line, or FANG+, has a downward trend.

Additionally, the S&P 500 equal weight index (grey line) has performed about in line with the market cap weighted S&P 500 tech index. The equal weight index is 17.1% higher year-to date, only slightly lower than the 17.8% advance in the traditional market cap weighted tech index.

If FANG or a smaller subset of tech stocks were really driving the overall tech sector, the market cap weighted index would be outperforming by a much more significant margin.

On September 24, the tech sector is going to change dramatically as two of the laggards, Facebook and Alphabet, will move into a newly created GICS sector - the Communication Services sector.

The new sector will replace the Telecommunications sector.

These two companies currently account for 19% of the tech sector. With the removal of those large cap stocks, Apple’s market share within the tech sector will increase to 21%, from 16% currently. It will remain the largest component of the tech sector.

Microsoft will be the second largest component of the revamped sector at 17% of the market cap, up from 13% currently.

The operating performance of Apple and Microsoft will become more critical than ever to the growth potential of the group. With each company transitioning its focus on its highest growth and high-margin business lines--services for Apple and the cloud for Microsoft--the sector will warrant a higher multiple going forward, in CFRA’s view.

Historically, tech trades at about 16.5x on a forward P/E basis, which is in line with the historical average for the S&P 500 index. Today the tech sector trades at 18.2x its 2019 earnings estimates.

While semiconductors will likely continue to weigh on the revised sector, earnings estimates for the semis have been reduced with growth for 2019 at 6.0%. That compares to 26.5% growth expected in 2018.

CFRA remains overweight the tech sector as we prepare for what is a seasonally strong period of the year for cyclical sectors. We view the increased exposure to Apple and Microsoft, with their strong cash flow and potential for upside to consensus estimates as a positive for the group.

Increased momentum from stocks that had lagged earlier in the year should also prove to be a tailwind for the sector into the end of the year.

View CFRA, services and research including Marketscope Advisor here.

View brief video interviews with Lindsey Bell of CFRA:

Lindsey Bell’s picks: Apple, AI, Nvidia, Intel, semiconductors here.

Duration: 3:14

Q2, Q3, the worst. Q4 good news here.

Duration: 3:53

Recorded: MoneyShow Las Vegas, May 15, 2018.