On Monday, after a reshuffling of $2.8 trillion of market cap across three sectors, brand-new sector Communication Services will become a part of the S&P 500 (SPX). It’s a revamping and renaming of the Telecommunication Services sector, writes Lindsey Bell Thursday.

The changes will broaden the sector’s exposure to more growth-oriented companies, thereby making the sector more cyclical in nature and increasing its beta. The move will also increase the expected price-to-earnings (P/E) ratio and significantly reduce the sector’s dividend yield.

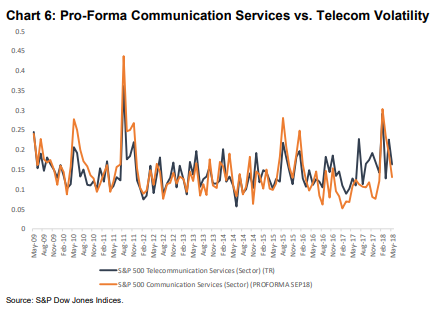

The one thing that will remain unexpectedly similar to the legacy sector will be a low level of volatility. The Consumer Discretionary and Technology sectors will be altered as they donate several of their industry groups to the newly-created sector.

All of these changes will go into effect on September 24 as a result of an update to the Global Industry Classification System (GICS) by S&P Dow Jones Indices and its partner, MSCI.

According to S&P, the new Communication Services sector will include companies that facilitate communication and offer related content and information through various media.

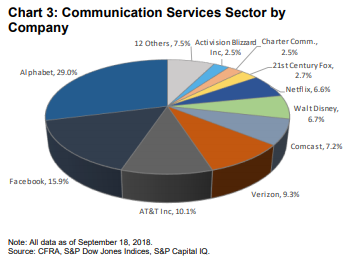

Three companies that currently make up the Telecommunication Services sector, AT&T (T), Verizon (VZ) and CenturyLink (CTL), will remain in the new sector.

Media companies like Twenty-First Century Fox (FOXA), Disney (DIS) and CBS (CBS) will be added, along with Netflix (NFLX) and TripAdvisor (TRIP) from the Consumer Discretionary sector.

Additions from the Technology sector include Alphabet (GOOG), Facebook (FB), Twitter (TWTR) and Electronic Arts (EA), to name a few.

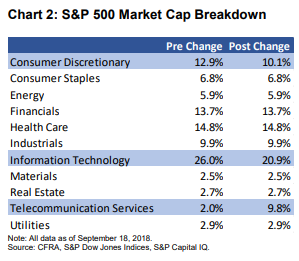

Breaking it down, Consumer Discretionary is losing 21.4% of its market capitalization to the new sector. Additionally, the changes will result in a loss of 19.5% in Technology sector market cap.

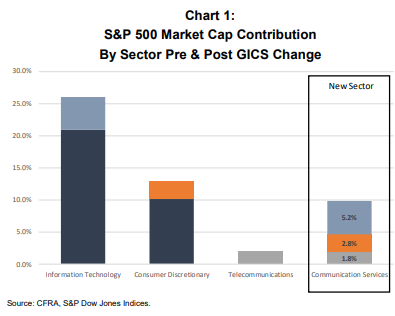

The chart below shows that the new Communication Services sector will represent 9.8% of the S&P 500 index, an increase from 2.0% on September 18. Tech will be the largest component of the new sector, representing 52.7% of the total. Consumer companies, including Netflix, will account for 28.7% of the sector, and the legacy telecommunication companies will only account for 18.6%.

While the weight of the Communication Services sector becomes a heftier component (it will be the fifth largest sector of the S&P 500 index), the weight of Consumer Discretionary and Technology will decline. In addition, Alphabet and Facebook will become the largest companies in the new sector, accounting for almost 45% of the sector. Legacy companies AT&T and Verizon will be the third and fourth largest components, accounting for 10.1% and 9.3% of the market cap, respectively.

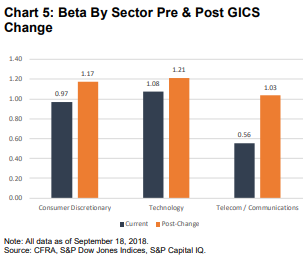

Note: All data as of September 18, 2018. Source: CFRA, S&P Dow Jones Indices, S&P Capital IQ.

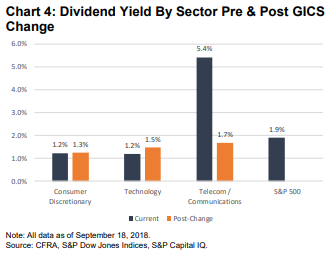

Even as several media companies with above-market dividend yields join the new group, the sharp reduction in AT&T’s and Verizon’s representation will weigh down the dividend yield of the historically defensive sector.

Smaller market caps from the dividend paying media companies won’t offset the lack of dividends at heavyweights Alphabet and Facebook. While Telecom currently boasts a dividend yield of 5.4%, the largest in the index, the dividend yield for the new Communication Services sector will shrink to 1.7%, below the 1.9% offered by the broad S&P 500 index.

A key characteristic of telecommunication companies has been low volatility and low beta. The addition of several media companies and tech stocks will result in the sector’s beta nearly doubling to 1.0, from 0.6 currently. A beta of 1 is in line with the market.

Volatility for the new sector will remain low. As S&P Dow Jones explains in a recent blog post, volatility is manifested by both dispersion and correlation, and while Communication Services will have higher dispersion than telecom, it will have a much lower correlation--thus, offsetting each other and keeping overall volatility low.

Source: S&P Dow Jones Indices.

Consequently, the new Communication Services sector will better reflect the rapidly changing way the world’s population communicates. It will result in a more cyclical, higher beta, lower yielding sector.

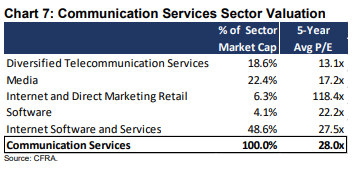

The forward multiple on the new sector could be as high as 28.0x, up sharply from the lower growth, value-oriented telecommunication sector that currently trades at 10.6x.

Source: CFRA.

For investors looking to get ahead of the GICS realignment, the Communication Services Select SPDR (XLC) is a new ETF that tracks an S&P communication services select sector index that consists of a mix of current consumer discretionary (30% of the ETF), tech (44% of the ETF) and telecom (11% of the ETF) companies.

The ETF began trading in mid-June.

View CFRA, services and research including Marketscope Advisor here.

View brief video interviews with Lindsey Bell of CFRA:

Lindsey Bell’s picks: Apple, AI, Nvidia, Intel, semiconductors here.

Duration: 3:14

Q2, Q3, the worst. Q4 good news here.

Duration: 3:53

Recorded: MoneyShow Las Vegas, May 15, 2018.