Bank stocks got a boost in the first week of October as upbeat economic data resulted in a widening of the yield curve. We expect each bank to perform differently, making it a sector ideal for stock pickers, says Lindsey Bell of CFRA.

Early October optimism quickly fizzled as fears that the Federal Reserve, led by Chair Jerome Powell, will maintain a hawkish stance on interest rate increases through 2019, regardless of the inflation or growth environment.

In the month ended October 9, the S&P 500 banks index declined 2.3% while the S&P 500 (SPX) advanced 0.3%. The sector took center stage on Friday as some of the largest banks kick-off the third quarter earnings season with the release of their results.

While the third quarter has historically been a soft quarter for the banks, a focus on out-quarter fundamentals will determine the future of the group. CFRA expects the operating environment will likely continue to be characterized by solid economic data, deregulation and higher interest rates, which we expect to impact each bank differently, making it a sector ideal for stock pickers.

There has been a divergence in the performance of the regional banks versus the large cap investment banks since late September, with the regionals underperforming their large cap peers for the first time since the start of the year.

In just the past month, the regionals have declined 5.5%, with the big banks only 0.9% lower. The regional banks are more sensitive to interest rates because their loan portfolios represent a significant portion of net interest income (an important measure in revenue calculation). While higher rates mean they can offer loans at higher rates, they have been reluctant to sacrifice the quality of a loan just to drive growth. Additionally, higher rates lead to higher funding costs related to deposits (which have been on the rise).

A compressed yield curve, driven by short-term interest rates rising faster than long-term rates, also doesn’t help. As such, the Federal Reserve’s decision to increase its target fed funds rate by a quarter point for the third time this year at its September meeting and its more hawkish tone toward future rate hikes didn’t bode well for the regional banks.

Both regional and large cap banks are struggling to drive loan growth in the current environment but given the more diverse business lines at the large banks, their reliance on the steepness of the yield curve has declined.

We aren’t expecting a blockbuster quarter from the big banks. Trading revenue will be flattish year-over-year given low levels of volatility, with equity trading showing limited growth and fixed income commodity and currency (FICC) trading expected to decline.

M&A backlog remains robust, but fees should be more meaningful in the fourth quarter. Investors will look past third quarter results at the big banks, to fourth quarter guidance, to determine the trajectory of these big banks. Expectations are for an improving trade environment, higher investment banking fees and loan growth momentum to pick up.

Investor sentiment going into the third quarter earnings season is bearish for both regional and large cap banks. While the industry has been a key beneficiary of the new tax law this year and deregulation is driving impressive bottom line growth, the underlying business trends discussed above aren’t as good as many initially expected.

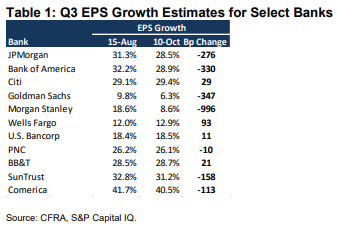

Several big banks, JPMorgan (JPM), Goldman Sachs (GS), Bank of America (BAC) have endured sharp reductions in third quarter growth estimates over the past two months, yet their stock prices have held up better than the regionals.

On the other hand, the regional banks earnings expectations have remained stable over the same period with the stocks moving sharply lower. That could mean that the regionals may react better to earnings, even if the outlook is worse than expected.

For the financials overall, the sector is positioned to have the third best earnings growth in the quarter out of the 11 S&P 500 sectors. Current consensus expects growth of 39.2% from the financial sector in the third quarter, broken out between 22.6% EPS growth from the banks (regional banks, plus JPMorgan, Bank of America, Citi, etc.), 23.8% from diversified financials including Morgan Stanley (MS), Goldman Sachs (GS), Berkshire Hathaway (BRK.B) and other asset managers and 241.0% growth from insurers.

In addition to guidance, we expect investors to focus on cost controls and margin trajectories when third quarter results are released. Discussion of capital deployment plans will be of significant interest as many banks received approval of capital plans from the Fed in June and CFRA believes dividend growth will be key to the bank story for years to come.

Finally, management commentary about the economic environment should remain upbeat, although it may carry a cautious tone given the uncertainty trade talks and higher interest rates have brought to the market.

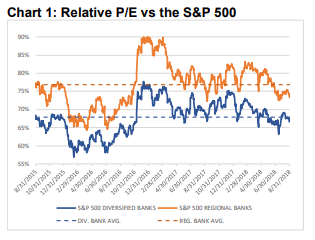

Turning to valuation, the price-to-book ratio (P/B) is the traditional way investors value banks. Currently, the S&P 500 bank index’s P/B is 10% off highs reached earlier this year (on February 23, 2018) and while it is off the 2016 low, the metric is still well below its pre-financial crisis high.

The sector’s next-twelve-month (NTM) price-to-earnings (P/E) ratio of 12.8X is below the 15.4X multiple the sector carried at the start of 2018 and the three-year average of 13.8x. The current multiple is also below the S&P 500 forward P/E of 16.5X. Both the relative and absolute P/Es are at a slight discount to the historical average. Regional banks are trading at a deeper discount than the large banks to on a relative basis at 12.7x currently vs its 13.4x three year-average.

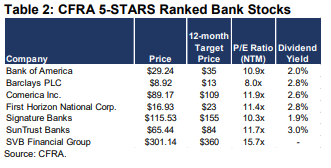

CFRA equity analysts have 5-STARS (Strong Buy) rankings on seven U.S.-based diversified bank and regional stocks (see table).

For more diversified exposure to the financials sector, Financial Select Sector SPDR (XLF) tracks the S&P 500 financial stocks and has approximately 45% of assets in banks, with smaller stakes in insurance and capital markets companies.

Meanwhile, Invesco KNW Bank (KBWB) has 85% of assets in banks, split between diversified banks and regional banks. Both are rated favorably by CFRA for the attractiveness of its holdings and tight bid/ask spreads.