In the international export-import business competing currencies force the U.S. dollar higher, a disadvantage for a country wishing to sell products on the world market notes Paul Cretien.

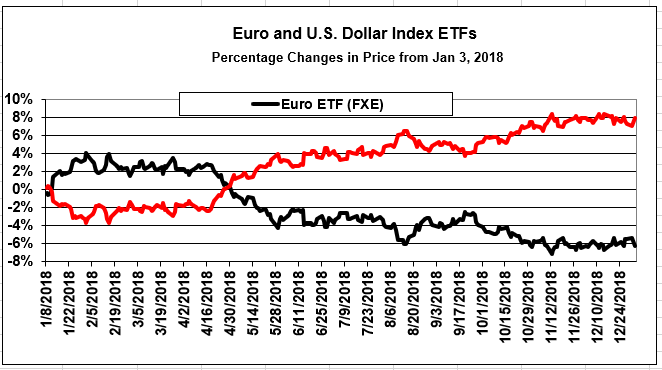

For trading purposes, exchange traded funds (ETFs) on the U.S. dollar index and the euro currency are more than an ordinary pair of securities that have a predictable relationship. The Invesco DB USD Index Bullish Fund ETF (UUP) and the Invesco CurrencyShares Euro Currency ETF (FXE) have a negative correlation that may produce specific trading opportunities (see chart).

The chart shows how the UUP and FXE appear as mirror images as their price changes are almost perfectly negatively correlated. The euro is one of several currencies whose price changes are inverted to those of the U.S. dollar, but the euro is the most powerful of these, having the greatest weight in the index.

There are several profitable trades suggested by this negative correlation. The trades depend on UUP falling in price with respect to the price of FXE over the early months in 2019. Viewing the chart, it is easy to imagine FXE and UUP as two lovers who embraced twice during the year 2018 and are eager to meet again in 2019. Spring and summer are made for romance between two currencies.

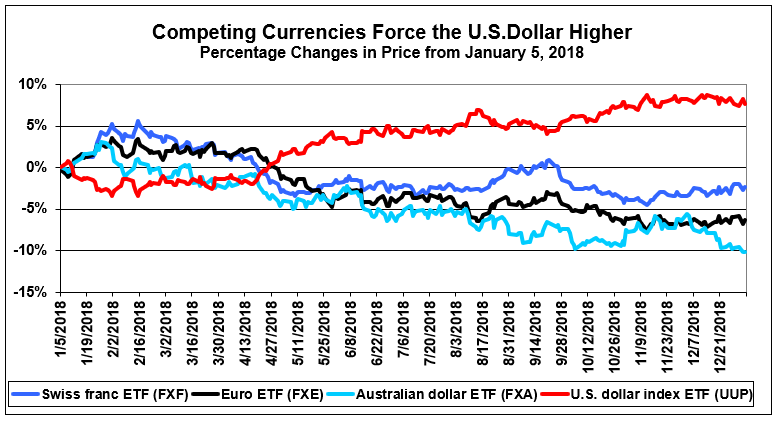

Just as the U.S. dollar is not independent, but is controlled by the inverse relationship with other currencies, the others are also not completely independent. For example, when one currency falls in price (either on purpose in order to improve its export trade, or due to a major geopolitical event as with the British pound following the Brexit vote) other countries that are economic competitors also reduce their currencies’ prices in response.

Three currencies that are competing for low price are the Swiss franc, Australian dollar and the euro. Their combined effect on the price of the U.S. dollar index is shown on the chart below.

In the international export-import business competing currencies force the U.S. dollar higher, a higher currency price is a distinct disadvantage for a country wishing to sell products on the world market. A relatively high price for the U.S. dollar benefits importers, such as American tourists traveling to Europe. For Americans producing goods for sale on foreign markets, it is bad for business.

In 2018 the Swiss franc, euro, and Australian dollar fell by 2.40%, 6.35%, and 10.11% , respectively, while the U.S. dollar index increased by 7.66%. This means, for example, that U.S. export products increased in price by approximately 14% relative to the euro. This is equivalent to a tariff of 14% on U.S. goods exported to European countries. One way to counteract this difference is for the United States to apply a 14% tariff on imports from the other countries. These differentials are what the trade wars going on currently are all about.

To take advantage of the U.S. dollar and euro “mirror image” trade, consider buying puts on the dollar-based UUP ETF, and buying calls on euro-based FXE ETF. This is a classic reversion trade, with the UUP/FXE differential at its highest point over the last year. A time span of three-to-five months may see the two prices coming close together or actually meeting and crossing as they did between April and May of 2018. With this time frame in mind, an expiration date in June 2019 would be appropriate.

One source of options price chains for UUP and FXE is Yahoo finance.com. For the June 21, 2019, expiration date on Jan. 4, 2019, eight strike prices are listed for UUP puts ranging from $20 to $30, with a $25.46 closing price for UUP on Jan. 4. Eighteen strike prices are shown for the June 21, 2019, expiration of FXE calls, ranging from $88 to $119 with a current price of $108.93 for FXE. Thus, there is no shortage of potentially profitable options trades for currency ETFs.