The Log-Log Parabola (LLP) Options Pricing Model show variances in options pricing that can produce profitable signals, writes Paul Cretien.

There is a way to determine at any time during the trading day, which options are over-priced or under-priced compared with the other options on an options price chain. The log-log parabola (LLP) Options Pricing Model will show the price variations and assist in the decision of which options to buy or sell.

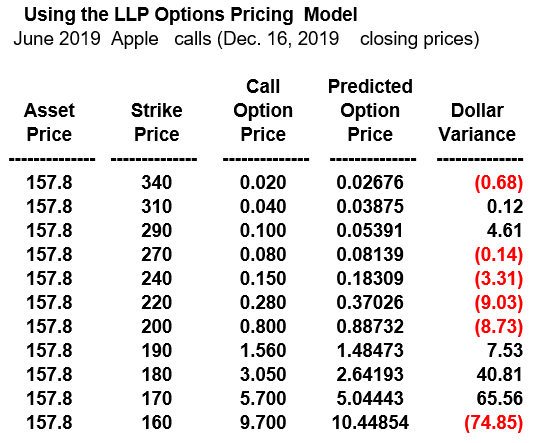

“Using the LLP Options Pricing Model” shows the model applied to Apple (AAPL) call options on Friday, Jan. 25, 2019 (see table). The first three columns are data from the options price chain – stock price, strike price, and the call price at each strike. The LLP model uses this data to compute an option price curve that shows the predicted call price at each strike.

The final column uses the differences between the market price and predicted price at each strike price to calculate the dollar variance – plus or minus compared with the predicted price. For Apple, the variance is equal to the number of option points above or below the price curve multiplied by the dollar value per option point.

The advantage in using the LLP model is that all of the calculations are automatic. The trader inputs the market price data and then reads the dollar price variations. Large plus or minus variations indicate possible trading opportunities. A large minus number encourages a buy and a large positive number recommends a sell.

The exhibit shows two large positive variations along with one large negative number. Apple’s options prices on Monday, Jan. 28, 2019, will be a good test of the recommended trades: Buy the AAPL 160 call and sell the 170 and 180 calls. Trading in both directions shows that the model is also useful for techniques such as straddles and strangles where risk is lower due to the use of offsetting potential price changes. But mostly this is a reversion trade. After two day this trade has been profitable.

The LLP model is a concise Excel program that can be downloaded with instructions by the author. Contact Paul at Cretien619@AOL.com.