The Bomb Cyclone that hit the Midwest this Spring can be exploited with options, writes Paul Cretien.

In March severe weather including snow, high winds and rain combined to form a “bomb cyclone” that killed livestock and left Midwest corn fields flooded. The effects on agriculture production will felt for months. It seems probable that prices will rise on cattle and corn due to shortages in each product. Extreme moisture could delay corn planting and push some farmers to switch to soybeans that can go in the ground later.

Lean hogs may feel an even larger price effect because of the need by China to import an increased amount of American pork after having to cull nearly one million pigs this winter due to African swine fever.

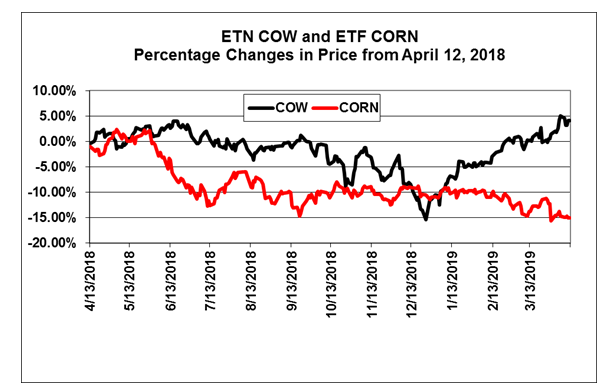

The chart below shows the current trends in the iPath Series B Bloomberg Livestock Subindex Total Return ETN (COW) and the Teucrium Corn Fund (CORN). Chinese demand for pork may have led to COW increasing even before the weather cyclone struck later in March. Corn was declining, but will increase in price due to a shortage caused by the storm and delays for farmers working in saturated fields.

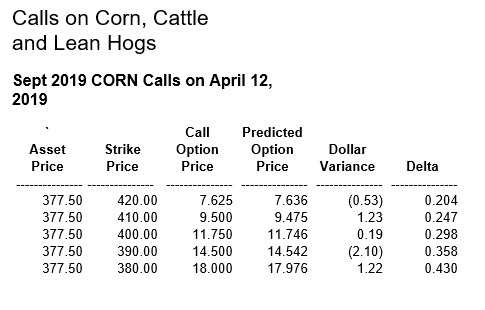

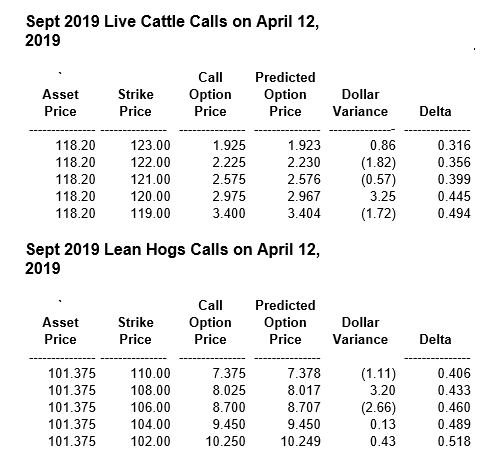

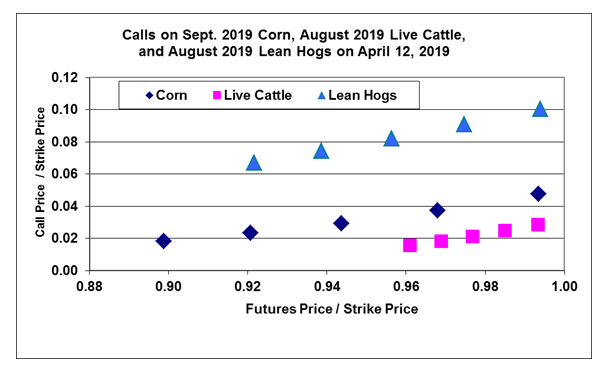

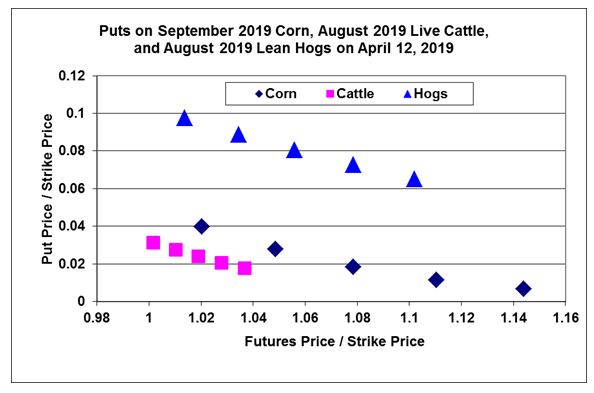

The chart just below shows the differences in price volatility of the underlying futures expected by the options price curve on Sept 2019 corn calls, August 2019 live cattle calls and August 2019 lean hog calls on April 12, 2019.

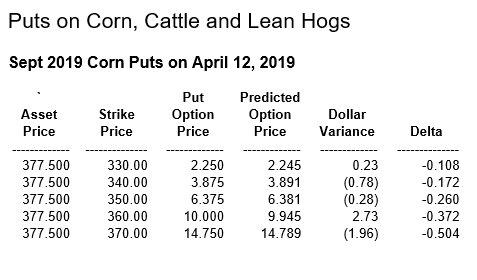

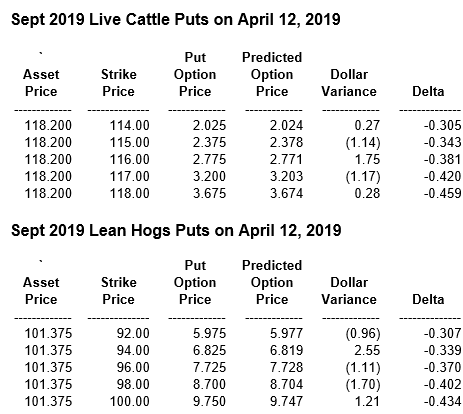

On this chart and on the second chart showing puts for the same products, lean hogs have a higher price curve caused by greater volatility that is valuable to the options market.

On the call and put charts live cattle is resting near the bottom with very low volatility expected by the options market. If the loss of livestock caused by the blizzard bomb cyclone affects market prices, the direction should be an upward price movement.

The tables labeled, “Calls on Corn, Cattle and Lean Hogs” and “Puts on Corn, Cattle and Lean Hogs” below indicate that option prices are close to the predicted price curves. Based on the weather damage and market demand, the likelihood is for increased prices for the agriculture products described above. Therefore we will choose calls for corn, cattle and lean hogs.

On both charts showing options price chains there are no large variations from predicted price curves, so the calls to be selected will be those that are expected to rise faster when the underlying asset price increases. In each case we will select the strike price that has a delta value near 0.50.

According to the chart showing call price chains, the strikes chosen are 380 in corn, 119 in live cattle and 102 in lean hogs 102. Each of these has the highest Delta and will move the most with a corresponding move in the underlying.