Comparing the cost-to-close with initial trade goal is the key when deciding whether to close or roll your covered call, writes Alan Ellman.

When we enter our covered call trades, we make our stock and option selection based on our initial time-value return goal (2% to 4% for one-month expirations). If the strike moves deep in-the-money as share price accelerates, we may consider closing both legs of the trade or rolling the option out or out-and-up.

Rolling options is generally reserved for scenarios close to 4 p.m. EST on expiration Friday. Mid-contract, we may consider the mid-contract unwind exit strategy where we close both legs and enter a completely new trade with a different underlying. On June 19, 2019, a subscriber named Mazin shared with me a trade he executed involving 25 contracts of Facebook, Inc. (FB). This article will evaluate whether the time-value cost-to-close aligns with the initial time-value return goal.

Mazin’s trade

- June 5, 2019: FB trading at $165, Sell-to-open the June 28, 2019 $165.00 call at $5.92

- June 19, 2019: FB trading at $181.92, the $165 call has an ask price of $24.36

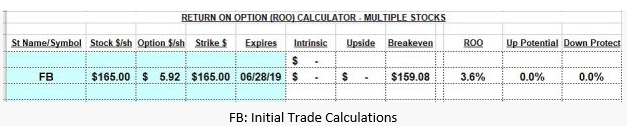

Initial trade construction using the multiple tab of the Ellman Calculator

The goal is to generate a 23-day return of 3.6% (ROO) with the understanding that there is no downside protection of that option initial profit (there is a breakeven at $159.08) and no opportunity for additional income resulting from share appreciation. That’s how the trade was constructed… period. Now, with FB trading at $181.92 and nine days until contract expiration there is an excellent chance that the goal will be realized. The question that remains is whether it makes sense to close the trade or roll the option. Let’s turn to the “Unwind Now” tab of the Elite version of the Ellman Calculator to determine the time-value cost-to-close.

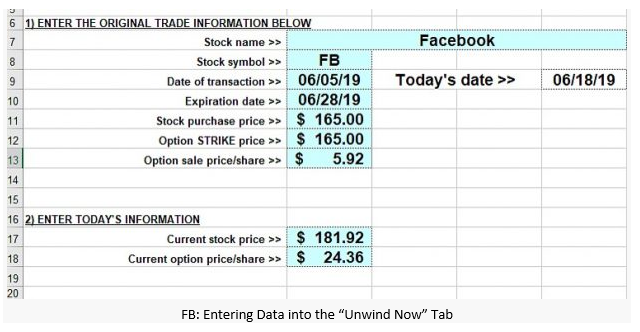

Elite Calculator data entry

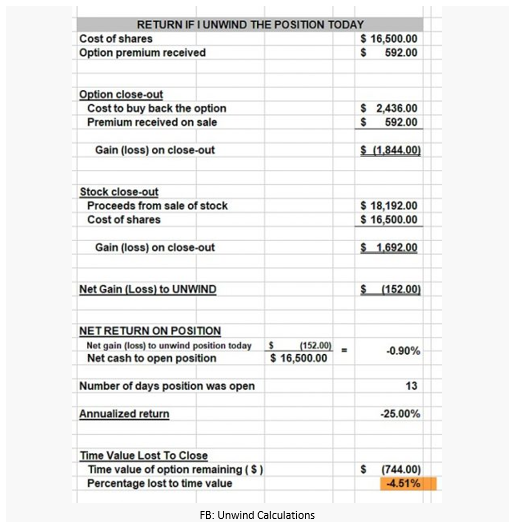

Elite Calculator closing results

The spreadsheet shows a time-value cost-to-close of $744 per-contract, which represents a 4.51% debit, greater than the initial time-value profit generated when the trade was constructed (3.6%). This makes no sense for either rolling the option or closing the entire position (both legs).

Discussion

In most situations, we reserve rolling in-the-money options as we approach contract expiration so that the time-value cost-to-close approaches zero. We also want the cost-to-close near zero when closing the entire position. In the case, 4.51% is way too expensive. The question we should pose to ourselves is this: Can we generate at least 1% more than the time-value cost-to-close by contract expiration? In this scenario, can we generate at least 5.51% in the next nine days? Probably not.

Use the multiple tab of the Ellman Calculator to calculate initial option returns (ROO), upside potential (for out-of-the-money strikes) and downside protection (for in-the-money strikes). The breakeven price point is also calculated. For more information on the PCP strategy and put-selling trade management click here and here.