The Federal Reserve’s backstop of corporate bonds is costing you yield, reports Mike Larson.

As Corporate Bond Buying Ramps Up, Income Options Dwindle. What to Do?

For every borrower, there’s a lender. But when discussing interest rate cuts, pundits and policymakers always focus on the benefits to the former, not the costs to the latter. And guess whose hide those costs come out of? Income-seeking investors like you!

Consider Monday’s Federal Reserve announcement. This one covered how the Fed will start buying individual investment grade corporate bonds directly, rather than indirectly by purchasing exchange traded funds (ETFs) that, in turn, purchase those bonds.

The move is clearly designed to benefit two constituencies. The first is Wall Street firms and other investors who own bonds that will trade at artificially inflated prices as a result. The second is corporations themselves, whose borrowing costs will artificially drop.

The Fed is assuming/hoping these companies will use the money for something productive – like investment in plant and property, or research and development, or at the very least, just keeping the lights on and workers employed until the Covid-19 epidemic wanes. But the track record of the last several years isn’t very encouraging.

As you know from my work, corporations used a huge chunk of the money they trashed their balance sheets borrowing in the last few years on “financial engineering”. That’s Wall Street jargon for things like overpriced takeovers, record stock buybacks, and other similar actions.

But what does this kind of news mean for you? Simple. If you’re an income-seeking investor, you get hosed! You see, when you buy a corporate bond or ETF or mutual fund that invests in them, guess what? You’re effectively the lender. You’re the “bank.”

You can and should expect to get compensated for the risk the company or companies you’re lending to will default. And that compensation comes in the form of higher yields than you would get on U.S. Treasuries. After all, the federal government has a much lower chance of default than a private corporation.

In times of economic crisis — when credit ratings are falling sharply— revenue and earnings are under severe pressure, and corporate balance sheets are in lousy shape, you can and should expect your yield to be even higher. Why? You’re taking on much more risk of loss as the lender.

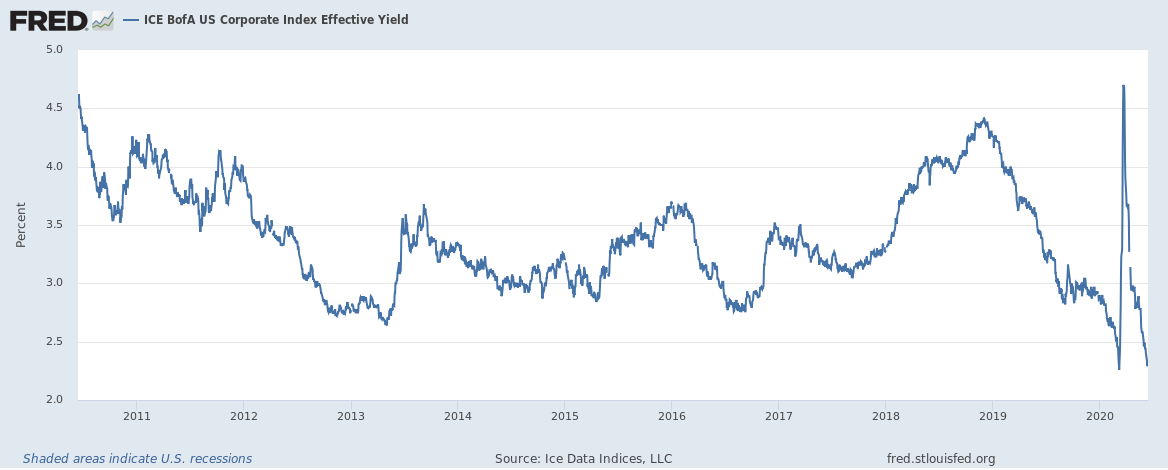

But take a look at the chart below. It shows the effective yield on a broad index of investment-grade corporate debt. Yields shot up to more than 4.5% a couple of months ago – offering you at least a reasonable amount of income in return for assuming greater default risk.

But thanks to the Fed’s recent actions, yields have collapsed right back to where they were in early-2020. We’re talking about roughly 2.3%, the lowest in modern U.S. history. And that’s despite the radical deterioration we’ve seen in underlying corporate default and debt fundamentals since before the worst of the Covid-19 outbreak hit.

It’s not just corporate bonds where we’re seeing yields plunge again. We’re seeing it in municipal bonds. We’re seeing it in emerging market bonds. We’re seeing it in high-yield, or “junk” bonds. In other words, there’s no relief in sight if you’re looking for generous income for reasonable amounts of risk.

Or is there? Are there ways you can boost the income your portfolio is spinning off? With relative safety, and in a prudent fashion?

As an income-focused analyst, that’s precisely what I’ve been trying to do in the Safe Money Report for many years. Learn how to access it below.

Given everything I’ve just told you about the yields available on a wide variety of traditional income-producing investments, one thing is clear: Never in our lifetimes have we seen a greater need for an income-boosting strategy. And based on our research, this powerful and reliable system could be just the answer for you ... right here, right now.

I’m about to roll out my June issue of the Safe Money Report with new ideas and new recommendations designed to ensure you do. Subscribe to Weiss ratings' Safe Money Report here… You can check the Ratings on your investments using the search tool at the top of our website here.