Anyone, including me, who thought the stock market might crash last week now knows that the Fed’s QE is at the moment in full control of trading behavior as once the dust cleared from the “Reddit short squeeze,” it was back to business as usual, states Joe Duarte of In the Money Options.

Of course, the whole thing was disturbing and highly inconvenient, but as stock traders the key is to stay with the trend, so we stay selectively long.

Last week it was all about Reddit “trading hordes” making hedge funds sweat, and fears that a major player would fold as margin calls would rain down and create a liquidity crisis. And while the scenario was plausible, and the markets may again be tested by liquidity worries in the future, this time was not THE TIME.

In fact, just as every other TIME in the last four years when we’ve had major volatility in the stock markets, eventually the dip buyers came in buoyed by the notion that the Fed will keep on putting money into the banking system and stocks will once again rise. And guess what? They were right once again and bought stocks aggressively. So, we’re off to the races again.

Of course, each new rally after a significant fright is different. In fact, it would seem logical that this time may be even more different than prior scare-induced declines as the events that unfolded created just enough volatility to change the playing field in terms of who won and who lost. Moreover, bond yields continue to creep higher and nothing awful seems to happen to stocks; a significant departure from historically similar episodes prior to March 2020, as I will describe in detail just below.

So here is the unfolding new set of trends in the complex system known as MEL, the complex system comprised of the markets (M), the economy (E), and people’s lives (L):

- Bond yields are still creeping higher and stocks don’t seem to mind.

- PMI and ISM data continue to document supply-chain problems leading to inflationary pressures in commerce, which is contributing to higher bond yields.

- Demographic shifts in housing, employment, and working environments are not likely to reverse anytime soon as people move from large metropolitan areas and continue to work from home while housing supply tightens, and builders can’t keep up with demand.

- The Fed’s QE will keep the stock market on an upward trend while

- Decreasing supply of key materials and consumer goods in the presence of high levels of monetary accommodation are by definition inflationary—just go grocery shopping.

- Sector rotation will lead to emergence of new leadership in the markets.

- Sector leadership will rotate more often than in previous cycles as events periodically rattle markets.

Can Rising Bond Yields Extend the Bull Market in Stocks?

I have been focusing on the rise of the US Ten-Year Note yield (TNX) for the past few weeks, primarily because most long-term mortgage rates are based on this benchmark. And since housing remains a central cog in what now seems to be a fledgling post-COVID-transition-influenced US economy, this makes sense in terms of MEL.

Yet, as the 1.15% area, which was important resistance, and is now important support, is critical to TNX, an equally important yield is that of the US 30-Year Treasury Bond (TYX), which is now nearing the 2% area. This is because TYX is extremely sensitive to inflation pressures, which is why the 2% resistance area is crucial to what happens next. In other words, breaches of these two key resistance levels will affect both the housing market and inflationary expectations. The only question is how.

MoneyShow’s Top 100 Stocks for 2021

The top performing newsletter advisors and analyst are back, and they just released their best stock ideas for 2021. Subscribe to our free daily newsletter, Top Pros' Top Picks, and be among the first wave of investors to see our best stock ideas for the new year.

As a result, the big question is what will happen to stocks and the housing sector when bond yields breach these critical yield-resistance areas? Here there are two possibilities:

- Stocks will fall or stocks will rise

- The housing market will heat up or screech to a halt

And while traditional relationships would suggest that stocks would fall and housing will collapse in response to rising bond yields, and they certainly may since, as the chart clearly shows this was the way things worked prior to March 2020; it is now possible and even likely in the current environment that a breach of nearby resistance in bond yields could lead to accelerated bond selling, which in turn would lead to more bond money being allocated to stocks, primarily as an inflation hedge while simultaneously juice the housing market as tight supplies and supply chain constraints for new building create a seemingly never ending cycle for higher home prices and higher demand.

I know it sounds implausible. But yet, it’s irrefutable, at least for now that bond money is moving into stocks and that the housing sector is on the rebound. Just look at the chart. Higher bond yields are fueling the advance in stocks, have been doing so since March 2020, and seem likely to continue do so in the foreseeable future unless the Federal Reserve changes its current stance on QE.

In fact, as the chart directly above clearly shows, since the March 2020 bottom in stocks, the S&P 500 (SPX) has been marching nearly in lockstep with the change in bond yields. Indeed, this is fairly clear evidence that the rally in stocks has been fueled by money coming out of the bond market. Moreover, since it coincides with the Fed’s QE acceleration it suggests that the market has been pricing in inflation since the Fed started its QE maneuvers after the COVID crash in March 2020.

What it all boils down to is that the market now believes the Fed’s maneuvers and the changes in MEL will be inflationary. Even more interesting is the fact that the market is expecting stocks to be an inflationary hedge.

So, barring something drastically changing if bond yields are able to decisively crack the overhead resistance levels, the odds would favor not a bear market in stocks but more likely an extension of the bull market in stocks but also perhaps a dramatic increase in its rate of rise.

BlueLinx Holdings is Making Rebar Sexy

As Bob Dylan once said: “the times, they are a changing.” And nowhere is this clearer than in the stock market over the last few weeks. Usually, the equity space is a place where sexy sectors, such as technology and biotech gather much of the momentum, the press, and money flows. But recently there has been a big shift in the MEL system, as I describe above as the markets, the economy, and people’s lives have been dramatically changed by the COVID pandemic. As a result, different sectors of the market have benefitted from this evolving landscape.

A case in point are the shares of BlueLinx Holdings (BXC) a Georgia-based building materials distribution company, which are starting to move decidedly higher ahead of expected earnings on 3/11/21. BlueLinx, which is far from being a household name, is in a business sweet spot at the moment as it distributes anything from wood and wood products to rebar and specialty products to builders, installers, contractors, and home-improvement retailers through its network of 50 outlets.

Most recently, the company delivered record results in its Q3 2020 report delivered on 11/2020 combined with a positive outlook. Moreover, the company cited rising materials prices, rising home improvement, and homebuilder product demand as ongoing and allowing them to have some pricing power and improving margins. And given the supply and demand situation in housing at the moment, it doesn’t look as if much has changed. But perhaps the most important aspect of the company’s fundamentals is its focus on improving the balance sheet debt reduction and increasing their liquidity, two factors, which are likely to make their results even better, especially when it comes to free cash flow and EBITDA.

The stock has been trending up steadily for several months, but the recent pullback due to recent market events has provided an entry point. Moreover, On-Balance Volume (OBV) and Accumulation Distribution (ADI) remain attractive. There is good support at the 20-day moving average as well.

I own BXC as of this writing.

Market Breadth Delivers Upside Reversal

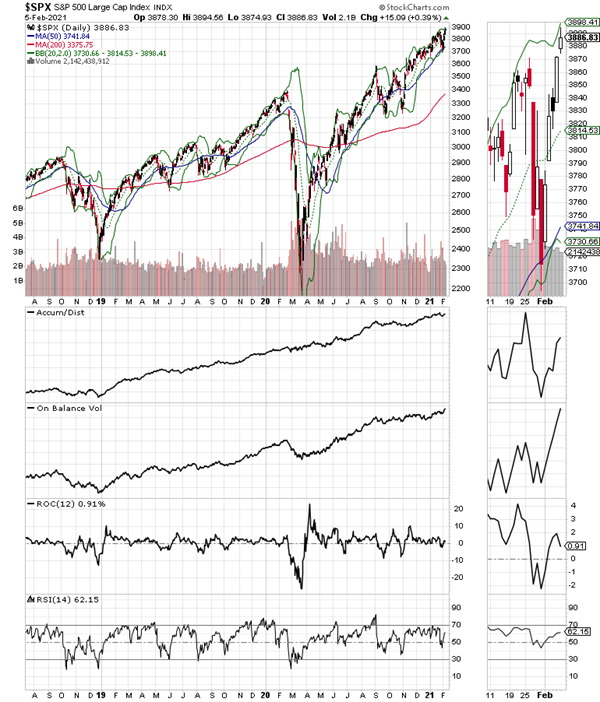

The New York Stock Exchange Advance Decline line (NYAD) recovered last week, making a new high and once again giving an all clear to the uptrend in the stock market.

Remember, as long as NYAD continues to make new highs, remains above its 50- and 200-day moving averages and its corresponding RSI reading remains above 50, the trend is up. This set of observations has been extremely reliable since 2016.

For its part, the S&P 500 also delivered a new high, confirming NYAD while On-Balance Volume (OBV) delivering a reassuring new high and Accumulation Distribution (ADI) showing a decent improvement.

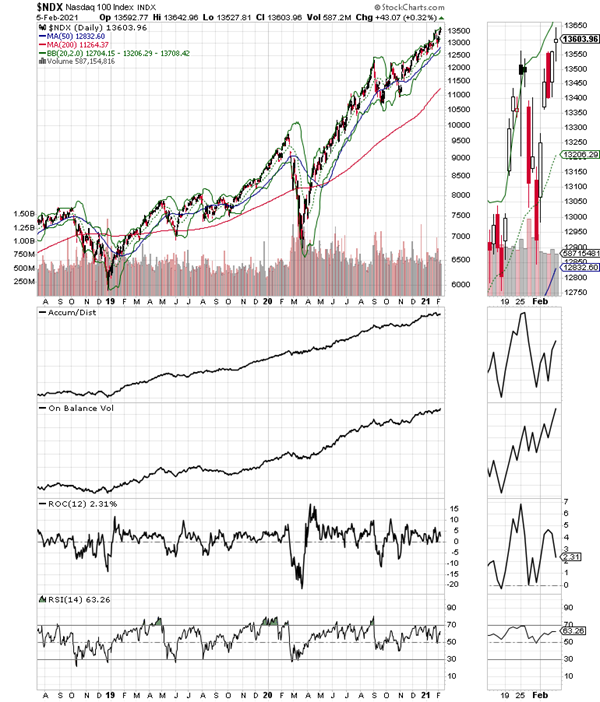

The Nasdaq 100 index (NDX), after a short-term reversal also made a new high last week. Moreover, as with SPX, the OBV made a new high and ADI also turned up showing the rally has momentum.

Bonds Hold the Key to Stocks

The relationship between stocks and bonds has changed and that change brings a new clarity to the market equation. I am not suggesting that this relationship can’t and won’t change again nor that stocks will rise forever.

What I’m suggesting is that if the current trends and relationships remain as they are, stocks could rise for a lot longer than anyone expects because there is so much money that can come out of bonds and into stocks. Thus, from a trading standpoint, it’s more about finding what’s most likely to go up than whether the long-term trend in stocks is up or down.

To learn more about Joe Duarte, please visit JoeDuarteintheMoneyOptions.com.