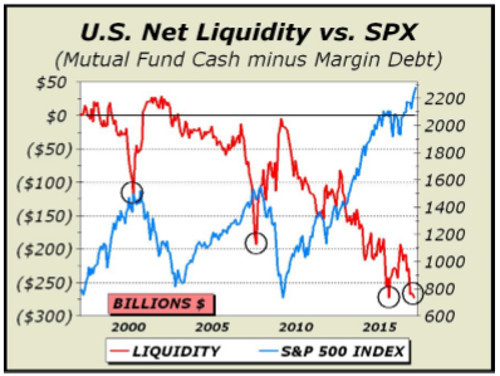

Our assessment of US Net Liquidity vs. the SPX suggests risk on an extraordinary scale, cautions market timer and economist Alan Newman, editor of CrossCurrents.

This chart that is featured below is, by far, the most important picture we have presented in this newsletter in our 27 year publishing history.

Yes, it hasn't mattered that liquidity has the worst levels ever and it hasn't mattered that any number of valuation measures have gone to ridiculous extremes.

Our only logical rejoinder is the word "yet." We grew increasingly worried all through 1999 as Nasdaq's tech stocks took the entire index to bizarre valuations, finally peaking in early March 2000 at an astonishing price to earnings multiple of 250.

In 2007, housing industry analysts felt that there was no ceiling on home prices. Folks were convinced. Buy a second home for only 5% down. No problem, no worries. This was same mantra we heard towards the end of 1972, 2000 and 2007 for stocks.

The same mantra. But prices were cut in half from the highs of each of those momentous peaks and it is becoming apparent that the same eventual fate lies in store for the major indexes at this point.

US Net Liquidity vs. the SPX is not a timing indicator. However, one would have been properly pessimistic at the end of 1999, well below Nasdaq's final trajectory into March.

One also would have been properly pessimistic into the summer of 2007, three months before the final gasp in October.

We are convinced that the trough measuring negative liquidity of more than $270 billion spells massive trouble. There's no way the first two troughs on this chart just happened to coincide with two of the worst bear markets in history. Negative liquidity is has more impact upon prices than any other circumstance.

Markets always fall faster than they rise. The current trough is so far below 2000 and 2007 that the possibility of a better result has contracted significantly.

Simply put, this second trip down has increased the odds for a replay of the prior two markets; as much as a 50% decline in prices from the eventual high.

The expansion of credit/debt over the last 15 years is truly frightening. The five largest central banks cumulatively total more than $18 trillion. They were less than half that size - $8 trillion - just before the collapse of Lehman and are now nine times their size in 2000.

The present environment attempts to support the most massive leverage worldwide than ever before. If expansion of credit/debt continues at this rate, the slightest pullback in demand will likely be sufficient to trigger at the very last, an economic recession.

In the meantime, we are stuck with extraordinary and gross overvaluations. The S&P 500 trade 88% higher than in 2012, yet earnings are down 9%. At this juncture, it all feels like deja vu.