The big story for 2017 is: “Retail is Dead.” So instead of trying to figure out which retailers will survive, the better — and safer bet — looks to be real estate, suggests Marshall Hargrave in Investors Alley's The Market Cap.

Real estate investment trusts (REITs), which are publicly owned real estate tenants, are great investments for owning real estate and finding dividends.

The major retail REITs, mall REITs included, have been gross under-performers in the REIT industry over the last year. These same retail REITs now offer better-than-average dividend yields at very attractive valuations.

For investors looking for some downside protection, REITs offer relative diversification away from the indices that are overweight technology

The bigger catalyst for retail REITs is their ability to adapt to the changing environment. Some of the key retail REITs are getting proactive in offering the best shopping experience possible.

That is, they have been leasing their space to non-retail tenants for office space, medical facilities, gyms and educational institutions. With all that in mind, here are the top three REITs to play the beaten down retail sector:

Simon Property Group (SPG)

Simon Property is the largest REIT period, across any industry. It just so happens that it specializes in malls and outlets. Simon Property pays a solid 4.5% dividend yield and has upped its dividend for seven straight years.

In an effort to combat the declines in mall traffic, Simon Property is focusing on offering a “21st Century” shopping experience by including valet parking, free Wi-Fi, more dining options and expanded entertainment offerings.

With that, Simon Property is still maintaining a solid occupancy rate, coming in at nearly 97% last quarter. And it’s still generating solid funds from operations (the key income measure for REITs).

Its FFO has grown at an average annual rate of more than 10% for the last half-decade. It expects that growth to continue with these its mall revamps.

General Growth Properties (GGP)

General Growth pays a 3.8% dividend yield and has a modest five-year streak of consecutive annual dividend increases. It’s paying out just 60% of its funds from operations via dividends. Like Simon Property, General Growth is maintaining a solid occupancy rate, which stands at just around 96%.

General Growth is opening fitness and lifestyle centers within its malls. The REIT has made a commitment to invest upwards of $400 million a year to redevelop and re-tenant its mall space. Ideally, these redevelopment plans will help boost revenues and drive traffic.

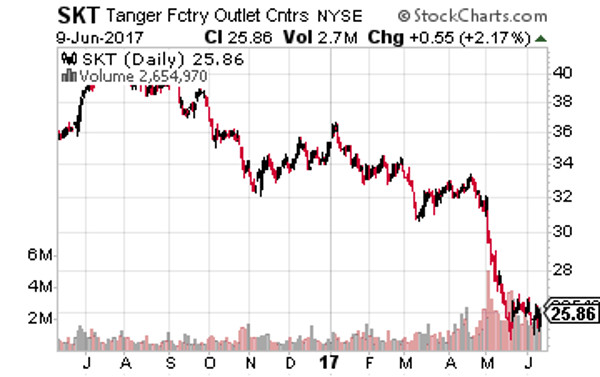

Tanger Factory Outlets (SKT)

Tanger Factory focuses on outdoor outlet centers and it’s the leader when it comes to dividends in the retail REIT space.

It pays a juicy 5.4% dividend yield and has managed to up its annual dividend for 24 consecutive years. Tanger Factory owns nearly 50 outlet shopping centers that it operates under its namesake.

The beauty of outlet stores is that they do well in good economies and bad, as shoppers love a bargain in good times and they love a bargain in tough times.

Hence its 24-year streak of dividend increases — that’s every year since its IPO. It’s also managed to maintain occupancy of at least 95% during that entire time.

In the end, the retail industry has been around for centuries; however, not all the major retailers will survive. Instead of trying to pick winners, the best strategy for investors looking to take advantage of this beaten down area of the market is with real estate.