Nothing has been more effective in killing bull markets than a deteriorating monetary climate and rising interest rates, cautions Jim Stack, money manager and editor of InvesTech Research.

As the economy heats up, managers begin to complain about supply shortages and delivery delays. These delays are often due to an excessively tight labor market.

In response, employers begin to increase wages to both keep current employees and attract qualified outside applicants. This vicious cycle aggravates underlying inflation pressures.

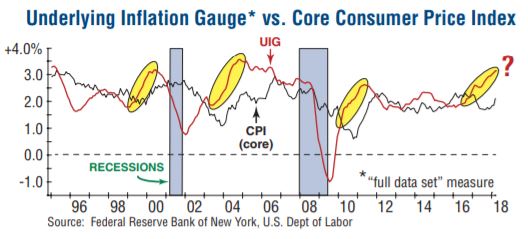

One of the best indicators of leading inflationary pressures comes from the Underlying Inflation Gauge (UIG). The UIG includes a wide range of nominal, real, and financial variables and focuses on the persistency of monthly inflation.

This gauge has proven especially useful in detecting turning points in inflation trends and tends to lead the CPI when it comes to forecast accuracy.

As shown below, the UIG has been signaling strong underlying inflationary pressures that are just now starting to reflect in Core CPI data. Should this trend continue, the Fed will find itself well behind the curve.

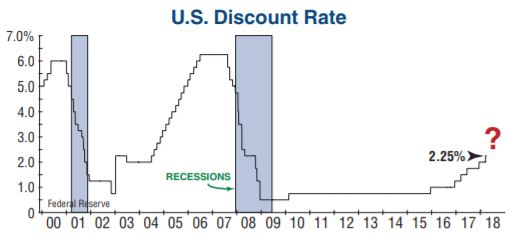

Since 2015, the Federal Reserve has raised the discount rate six separate times (as shown below). Recent Fed meetings have also indicated that future rate hikes are on the way.

It’s important to note that we are not stating that six rate hikes are too many, or that current interest rates are too high. Our focus is on the fact that the monetary environment has taken a distinct turn for the worse, making current equity valuations even more dangerous and susceptible to a future downturn.

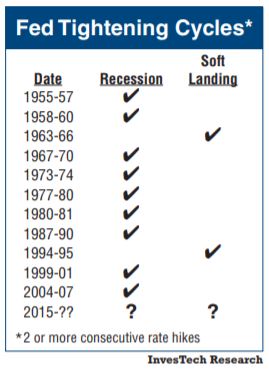

Once started down the track of tightening, the result appears all but inevitable. Out of 11 past tightening cycles, nine have resulted in a recession while only two created a soft landing that allowed the Fed to ease and avoid a contraction.

As shown in the table below, the Federal Reserve has a dismal track record of simultaneously slowing the economy and finding a way to avoid a full-blown recession. While the Federal Reserve likes to think they are preemptive with interest rate hikes, in most economic cycles they react too late and do too little.

Based on history, the current investment landscape is not conducive to a positive risk/return scenario. While each cycle has its own unique characteristics, one of the key contributors to equity market returns in this cycle has been cheap money and historically low interest rates.

As the monetary “punch bowl” continues to be removed, we believe the combination of increasing inflationary pressures and an unfavorable interest rate climate makes the current environment particularly hazardous.

At this stage, the strength in the economy and lack of major divergences prompt us to continue giving this bull the benefit of doubt. Yet the level of market risk today is high and rising. While a new bull market high may still lie ahead, now is the time to take incremental steps to prepare for the next major downturn.

Not only is it the second longest and second largest bull market on record, but the degree of overconfidence or overexuberance is disconcerting — at both the investor and consumer level.

In addition, the amount of margin debt (money borrowed to buy stock on margin) all but guarantees that when the time comes to exit, that door will be too small. In our view, the spike in volatility over the past two months is a taste of the bear market pain to come.

However, with that warning comes our caveat that key technical and leading macroeconomic evidence is not yet confirming a bear market. In other words, it would likely be premature to sound the death knell for this aging bull market.

So while we have reduced our allocation to 72% earlier this year in anticipation of this badly overdue correction, at this point we will still refer to it officially as a “correction” until evidence confirms otherwise.