What's the best way to generate income, asks mutual fund expert Janet Brown, president of FundX Investment Group. Many investors, particularly retirees, rely on their investments for income.

Some investors focus on dividends, either from bond funds or stock funds, as a way to generate the income they need to cover their expenses. But this can be both inefficient and risky.

For instance, monthly and quarterly distributions often vary, depending on interest rates and the underlying stock or bond yields. This can make for an unreliable cash flow. One month, your dividends might be enough to cover your bills, but the next month, you could be short.

Additionally, if you find yourself seeking a higher dividend yield without paying attention to where that yield is coming from, you risk losing money. Remember that a fund can have a high yield and still have low or even negative returns if its price has declined more than the income it has generated.

iShares High Dividend ETF (HDV) is one recent example: it sorely underperformed the rest of the stock market for the past couple of years. If you’d bought HDV because of its 3.58% yield, you would have missed out on solid returns during that time. Over the trailing 12 months, HDV gained just 5%, while other Class 3 funds were up 15-25%.

A total-return approach to generating income

We believe investors are better off positioning their portfolios for total return, which is the combination of capital appreciation and income. A total-return approach is designed to grow your portfolio over time by selecting funds by returns, not by yield alone.

An efficient way to create a reliable cash flow from your investment account is to set up an automatic withdrawal plan to have a set amount of cash sent to you (or your bank account) each month.

To generate cash for these withdrawals, it's best to shave off shares of funds each month. This can also be automated at most brokers.

Alternatively, you could select shares of a fund to sell based on tax efficiency—selling shares of a fund you’ve held at least 12 months to realize long-term capital gains, or harvesting losses to offset some future or current gains.

Another approach is to use your Upgrading trades to free up income. When a fund you own falls into the Sells, you could put part of the proceeds aside to take withdrawals and invest the rest in a better performing fund.

Don’t use only fixed income for income

It’s best to think of fixed income as a balancing portion of your portfolio allocation rather than as a source of your monthly payouts. This may seem counter-intuitive. After all, aren't bonds called “fixed income”? The coupon yields on individual bonds are indeed fixed, and this results in their lower risk when compared with stocks. Combining stock funds with bond funds is a great way to generate both growth and income.

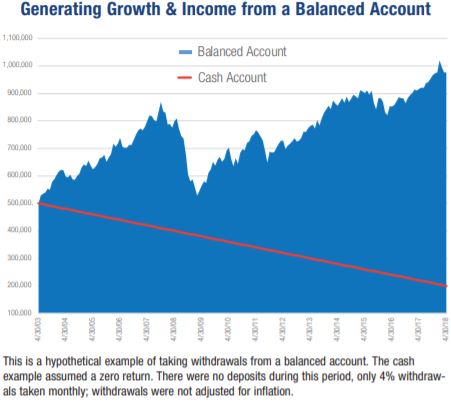

How a balanced account can generate growth & income

If you invested $500,000 in a balanced portfolio (60% in a portfolio similar to NoLoad FundX's Monthly Upgrader Portfolio and 40% in a portfolio like NoLoad FundX's Monthly Flexible Income Portfolio) and you took 4% out of your portfolio each year starting in May 2003, you would have generated $300,000 in income by May 2018, and your remaining portfolio would be worth around $1 million (blue), putting you in good shape for the rest of your retirement.

If you hadn’t invested your $500,000 during this 15 year period, however, and you’d withdrawn 4% a year to cover your expenses, your initial $500,000 would have shrunk to $200,000 (orange line). This means you could have a higher risk of running out of money in retirement or you might have to withdraw less than 4% from your accounts and lower your quality of life.

It wasn't easy to stay invested during this 15-year period, but it paid off: you were able to pay yourself a steady income and grow your portfolio even during some of the most challenging market years ever.

Get monthly investment guidance by subscribing to Janet Brown's NoLoad FundX newsletter here…