The bull call diagonal spread may be configured in many different ways in different market situations, asserts Kerry W. Given, Ph.D. (aka Dr. Duke). He is the founder and managing director of Parkwood Capital, LLC.

The bull call diagonal spread is only one of the tools in the trader’s toolbox, but it has some unique advantages. We recently closed a diagonal spread on Goldman Sachs (GS) in our trading group for a nice gain and the following discussion will use that position as an illustration of the advantages of the diagonal call spread.

When buying a bull call diagonal spread, we buy a call option farther out in time and sell a near term call option to reduce the cost basis of the call option we purchased. Over time, we may buy back the short option and sell another option, thus further reducing the cost basis of the long option over the course of the trade, and thereby increasing the potential gains.

The principal advantage of the diagonal call spread is that it gives the trader more alternatives for a profitable outcome. If the stock price moves higher as predicted, the diagonal spread will profit, but a sideways move for some period of time will also result in a profitable outcome.

Rolling the short call out at the same strike price week after week or month after month is a powerful advantage of the diagonal call spread. Each roll generates a credit that continues to reduce the cost basis of the long call and grows the profit potential of the position.

The ideal stock price move for the diagonal call spread is sideways and slowly trading higher. This will maximize the cost basis reduction and optimize the position’s gains. A stronger and faster price move higher will force the trader to close the trade early, but this scenario will still result in a profitable trade in most cases.

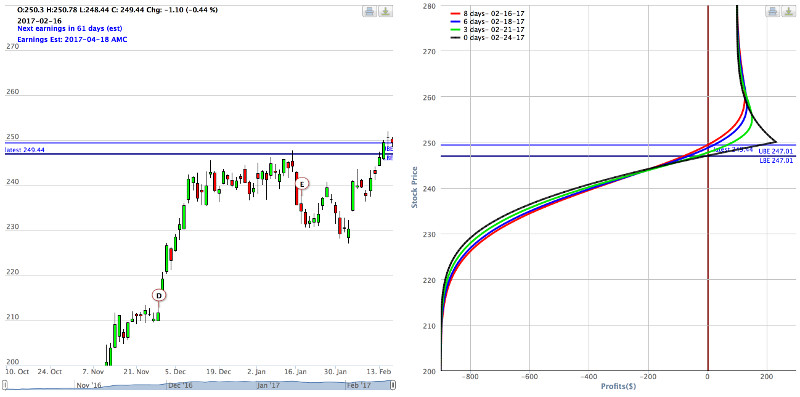

The first, and most important, trade setup rule for the diagonal call spread is to establish the position initially for a debit that is approximately equal to or less than the spread width. On February 16, we bought the Goldman Sachs (GS) March monthly (3/17) 240 call and sold the February weekly (2/24) 250 call.

Our net debit was $900 per contract. I would not have entered the trade if I couldn’t negotiate a debit of approximately $1,000 or less. The spread width was $10, so the spread’s maximum potential value was $1,000. If I establish the position for less than $1,000, I am starting the trade with a potential gain. I will lower the cost basis as I roll the short calls out week to week, but it increases our probability of success if we start with a potential gain rather than bank on reducing the cost basis later to move us into the black.

The risk:reward ratio diagram for this position is displayed below. Note that the break-even is the brown vertical line to the right of the center of the graph. This display turns the risk/reward diagram on its side. The advantage of this display is that one may easily see where support and resistance on the stock price chart fall on the profitability curves for the diagonal spread.

Source: Screenshots provided courtesy of Optionetics Platinum © 2017.

All rights reserved.

In this GS position, we sold a February weekly call and bought the March monthly call. Weekly options have become very popular and certainly add to the trader’s flexibility. In general, selling call options more frequently will bring in a larger amount of premium and lower the cost basis of the long call more over time. But that assumes that the underlying stock price moves as we predicted.

The weekly option is less expensive than the monthly option and this results in the lower break-even price for our position being closer to the current stock price. Therefore, I have less downside protection, at least for the first couple of weeks. In my experience, this disadvantage is minimized somewhat when using stocks with higher levels of implied volatility, but those are the very stocks that are more likely to pull back on us.

The diagonal call spread requires ongoing trade management, and the trader’s price and time predictions for the underlying stock are critical to her success. The most common decision points come as we approach expiration of the short call. If the stock price is close to the strike price of our short call, the most common action is to roll out at the same strike price. Rolling out involves buying back the short call that is nearing expiration and selling the same strike call for the next week. This will generate a credit that reduces the cost basis of the underlying long call and increases the maximum profit potential.

If the credit for rolling out is too small, the trader may try rolling out to a future week or month. Stocks with lower levels of implied volatility may require the trader to always use monthly options to generate sufficient credits.

As the stock price moves higher and the short call moves ITM, the credit to roll out will be reduced. This forces a decision to either close the position, normally for a profit, or consider rolling out and up to a higher strike price call. This roll higher will require a debit, i.e., we are adding capital to be at risk in this position. On the other hand, we are also expanding the spread width, and therefore the potential maximum gain. Hence, the trader’s opinion about the underlying stock’s trend is critical.

In our Goldman Sachs spread, we rolled the February week four $250 call out to the March week one $250 call, and repeated this with March week two, and finally rolled to the March monthly $250 call. At that point, we had a GS March 240/250 call vertical spread. But our cost basis was reduced to $355. We closed the position on March 15 for a net credit of $662 per contract. With a cost of $355, our net gain was $307 per contract, or +86%.

The power of the continuous cost basis reduction is two fold. It not only builds our potential gains, but it also reduces our maximum potential loss as the trade progresses. In this example, GS actually traded lower as the trade progressed (opened at $250.30 and closed at $247.72), but our lower cost basis allowed us to persevere and lock in an excellent gain.

Through this discussion one can see that the optimum stock price trading pattern for the diagonal call spread is sideways to slightly bullish. This pattern optimizes the number of rolls and significantly reduces the cost basis of the position, thus increasing the profit potential.

The bull call diagonal spread may be configured in many different ways in different market situations. We may use the diagonal spread when bullish on a stock for a period of a few weeks or several months. We may sell weekly options or monthly options against a long call that may be a monthly or a LEAPS call. The risk:reward diagram for this trade varies dramatically with one’s choice of strikes and expirations.

The diagonal spread may be profitable even when the stock just trades sideways, and we may easily survive minor pullbacks and continue to manage the trade to a profitable end.

The diagonal call spread is indeed a powerful tool for the trader’s toolbox.