Any major correction in global markets could see the U.S. dollar get a major risk bid higher. So counting on a weaker dollar to alleviate the emerging market debt burden may be wishful thinking, asserts Jack Crooks of Black Swan Capital.

Quotable

““Anyone who spends too much time thinking about international money goes mad.”

—Charles Kindleberger

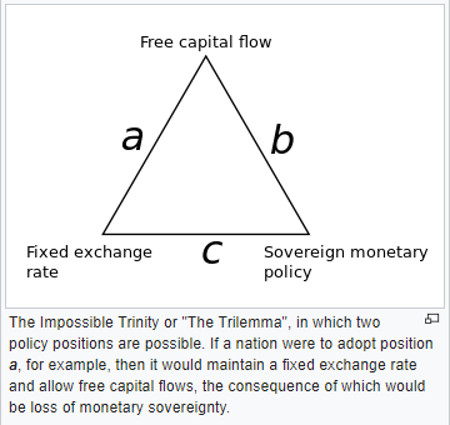

Revisiting the Mundellian Trilemma (Dilemma) & Emerging Markets

The Mundellian trilemma says policy makers can control only two of the three main variables in global finance, but not all three at the same time.

“…it is not feasible to have at the same time a fixed exchange rate, full capital mobility and monetary policy independence. Only two of the three may co-exist (according to the Mundel-Fleming logic),” writes Helene Ray, of the London School of Business, International Channels of Transmission of Monetary Policy and the Mundellian Trilemma.

In fact, in the world where we live, reality has overwhelmed theory—the Trilemma has morphed into the Dilemma. Why? It’s because global financial markets are inextricably linked through investing, funding, collateral, and trade flows to name a few. These linkages create increasingly complicated feedback loops which are not accounted for in modern neoclassical economics.

Even for a major industrialized country with free-floating exchange rates, it is not a given it can maintain a “sovereign monetary policy” within a world of full capital mobility. Let’s think about the UK for example.

Because of the hit to the British pound, thanks to the initial Brexit surprise, consumers are seeing rising prices in the UK. The Bank of England, believing it has a sovereign monetary policy, has signaled it will raise interest rates in order to protect the pound even though domestic economic growth seems to be weakening, and the whopping trade deficit seems to be getting worse.

But because global speculative capital flows have grown so large relative to longer-term investment flows, speculators may anticipate a strengthening pound near-term will likely hurt economic growth and exacerbating the whopping and widening trade deficit. If so, said specs might attack the pound in expectation the Bank of England would have to reverse its prior actions and live with a weak currency for a while. Thus, it could enforce a vicious circle downward in the currency and prove the Trilemma is now simply a Dilemma even for developed world nations with relatively deep capital markets.

As you would suspect, emerging market nations have even less control over their sovereign monetary policy because they lack capital market depth (in addition to other intangibles such as proven fiscal and central banking track records).

Emerging markets still rely on the U.S. dollar denominated funding (U.S. dollar denominated debt is estimated from $3+ trillion); i.e. emerging markets are the periphery and they are still highly dependent on the center country—the United States.

The simple fact hasn’t changed much since either the emerging markets crisis back in 1997 or the credit crunch in 2007; the U.S. is the center of the global financial system with the dollar as the world reserve currency and it takes on the responsibility of world banker and provider of global liquidity in a world where key commodities are still dollar denominated. it is inevitable U.S. monetary policy will be transmitted around the globe (draining sovereign monetary policy from others) and especially to the emerging market world.

Let’s say an emerging market country wishes to reduce interest rates in an effort to stimulate demand locally. It is likely, again because of massive spec capital flows, the country would see its currency depreciate relative to the U.S. dollar, now that the U.S. Fed has signaled more rate hikes, which increase the relative yield for the U.S. dollar.

The potential positive impact of lower rates would be offset by the higher debt service costs for local companies holding dollar denominated debt (transmission of higher costs through relative currency rates). In addition, many U.S. institutional investors stretching for yield because of the U.S. zero bound rate environment are likely already moving (or considering it) out of some of the clearly riskier EM paper back into less risky short-term U.S. paper.

Thus, we effectively have emerging markets with no sovereign monetary policy, and a floating rate currency, subjected to the whims of free global capital flow (no surprise the IMF has touted the benefits of capital controls). Where oh where might that supranational currency bancor be?

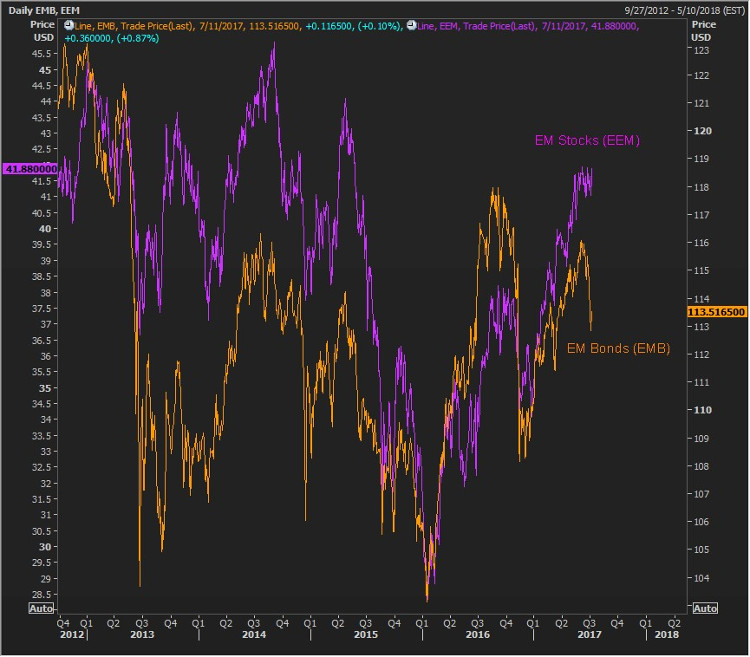

Take a look at the chart below which compares iShares MSCI Emerging Market Index ETF Stocks (EEM) to iShares JPMorgan USD Emerging Market Bond Fund ETF (EMB). These two tend to move together as they are usually dependent the same capital flows from the center (and other industrialized world investors seeking higher yield/return).

Notice the divergence? EM stocks have continued to climb, but because of rising yields globally, EM bond prices have fallen sharply. Who leads, who follows?

Given the relative weakness in Emerging Market Stocks compared to U.S. equities, we suspect if the Fed follows-through with its rate hike campaign into 2018, the pressure on emerging markets will grow considerably as flows to EM markets on yield basis alone moderates. Emerging market bonds will likely lead stocks lower.

The saving grace for emerging markets could be a weakening U.S. dollar. The total amount of credit in U.S. dollars dwarfs similar offshore credit in sterling, yen, Swiss franc, or even euro. And said credit was issued primarily by European-based global banks (84% of dollar-denominated international bank credit has been extended by non-US banks). Thus, any major correction in global markets could see the U.S. dollar get a major risk bid higher.

So counting on a weaker dollar to alleviate the emerging market debt burden may be wishful thinking.

To sum up: Once again neoclassical economics says one thing, but Mr. Market says something else. It’s a real dilemma.

View Currency Currents, commentary, and analysis at Black Swan Capital here…