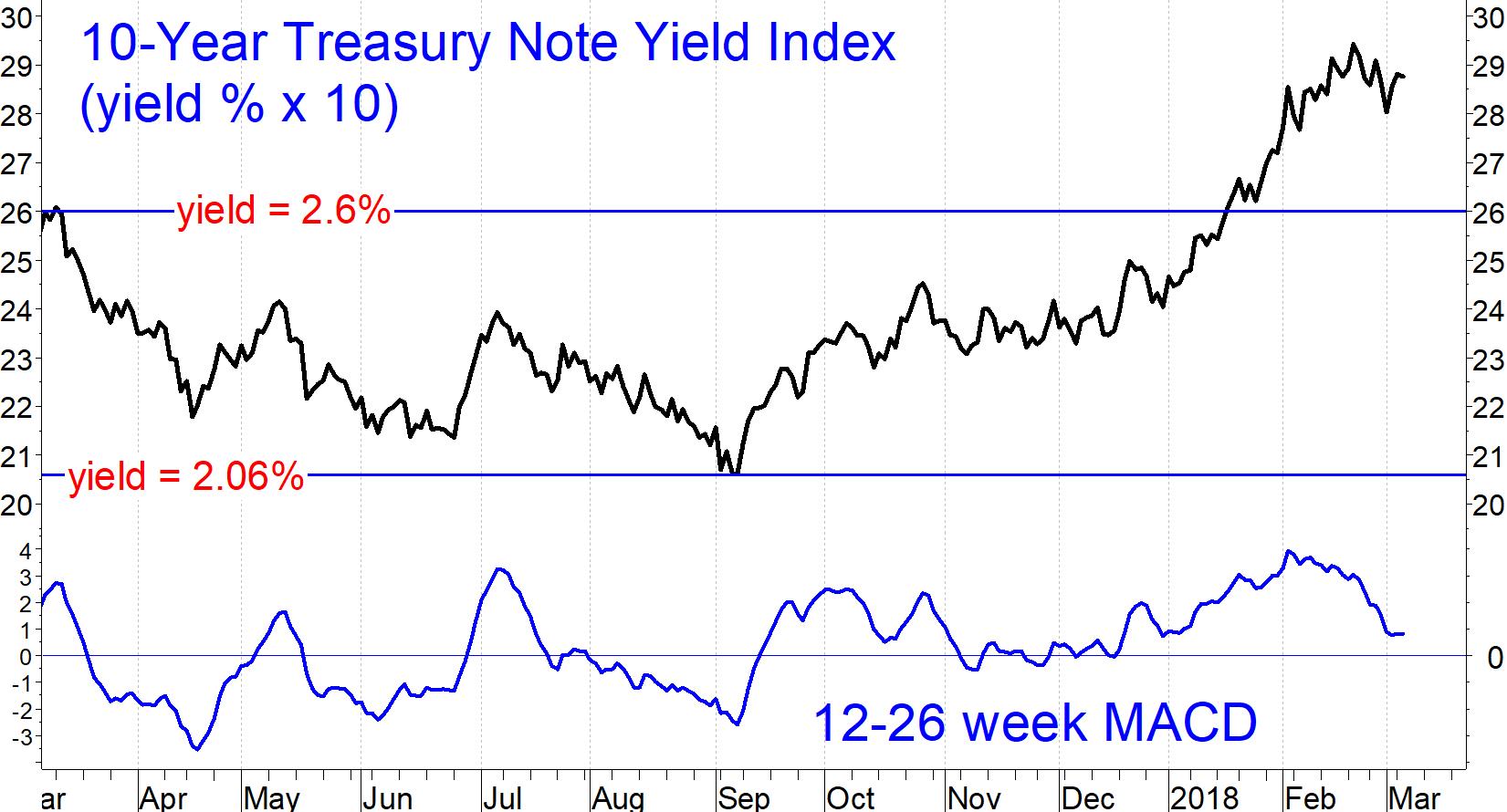

The ostensible catalyst for the Jan. 26-Feb. 8 correction was the rapid rise in interest rates that has occurred this year. Fortunately, 10-year Treasury note yields appear to be stabilizing in the 2.8%-2.9% range, says Marvin Appel, MD, PhD.

Old resistance was in the 2.6% area, where yields topped out in December 2016 and again in March 2017.

This year brought a retest of the 2013-2014 highs near 3%. The 6-19 week MACD of yields is near zero, suggesting a neutral or very slightly bearish bond market climate.

I expect 3% to hold for at least the next several months.

Note that a traditional rule of thumb for estimating “fair” interest rate levels is the level of nominal GDP growth. The U.S. economy is expanding at approximately 2.5% in real terms.

Adding 2% inflation to that gives a fair yield of 4.5%.

So why are yields so much lower even as the federal government has boosted the deficit with tax cuts and expanded spending? I believe that European Central Bank (ECB) yield suppression (quantitative easing) is largely responsible, driving euro investors here in search for yield.

The next threat to bond prices here is when the Europeans turn off their printing presses. That may be a risk starting in the fourth quarter. Until the ECB changes course, our bond markets should remain stable.

Subscribe to investment newsletter Systems and Forecasts here…