What are global capital markets wrangling with this week August 13 – 17? Also, is August 10 the beginning of Correction 2.0? Will the Emerging Market implosion get worse? writes Ziad Jasani Sunday.

View my weekly strategy session here

Recorded: August 10, 2018.

Duration: 1:30:26.

• Turkey’s economic/currency crisis spilling over to Eurozone/globe.

• US-China trade war.

• US-Russian sanctions.

• Bottom line: Emerging Markets have not made lower lows (yet) and Dr. Copper has been able to hold support at $2.73; two strong “tells” that this mess gets mopped up next week.

Will Oil be manageable by Trump to help with mid-term elections (prices at pumps)?

• Iranian sanctions offer support to price.

• Venezuela, Libya, Nigeria production/distribution woes offer support to price.

• Inventories in the week ahead likely support to price.

• Bottom line: While Oil remains above $66.89 (50% retracement of 2014 drop to 2016 pop) there is a better chance for a short-term bounce to the mid-$72 range.

Is U.S. inflation under-control or ringing-the-equity-sell-off-alarm?

• Core CPI highest since 2008 but probability of a 4th U.S. rate hike in December 2018 went down from 66% to 61% today.

• Soaring shelter/rent costs may eat into disposable income affecting back-half growth.

• Are U.S. Treasury yields now under a ceiling? Meaning, is it time to rotate into defensive/value equities and buy bonds?

• Bottom line: Bonds and Defensive Equity Sectors (XLU, XLP, VNQ, IYZ) have not given us break-out on the CPI data, and yield charts show strong support close by, suggesting this isn’t the time to rotate any further into Defense but fine to hold until the EEM mess gets mopped up.

Strong and rising USD

• Pressuring Commodities, particularly Precious Metals, Emerging Markets, Dow/Industrials/Materials, Technology.

• Adding to loss of confidence in Euro.

• Bottom-Line: While the EUR/USD pair remains above 1.135 we’re more likely to see a softening of the USD timed with Retail Sales Wednesday, August 15 and a swing-low for the euro.

Equity valuations, earnings potential and what if we’re in the back-end of the global expansion cycle?

• Synchronized global growth has ended, global growth is decelerating.

• U.S. trade & foreign policy ensures fractures in growth deepen.

• Valuations are high relative to historical standards (12-month forward P/E S&P 500 at 30% premium to 10-year average).

Bottom line

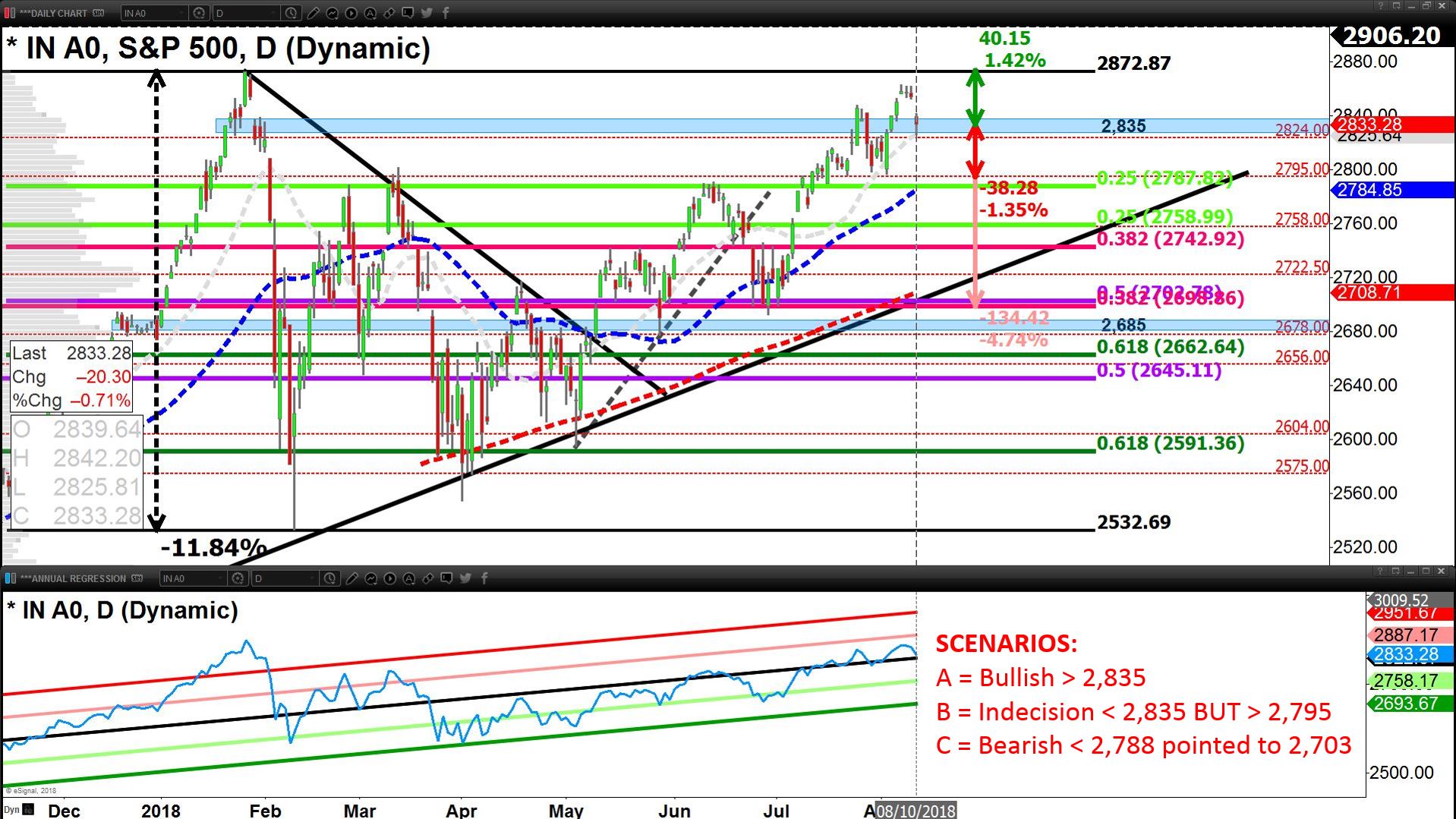

• While the S&P 500 remains below 2,835 and the Globe (ACWI) remains below $73.03 down-side risk is greater than upside; however, a correction forming is less likely as Emerging Markets and Commodities have not made lower-lows as of yet.

• We’re looking for an Equity, Commodity and Currency on the other-side of the USD bounce to take place within a week.

Join Ziad at MoneyShow Toronto Sept. 15 when he discusses Portfolio Management Strategies for Active Investors. Information: ZiadJasani.TorontoMoneyShow.com