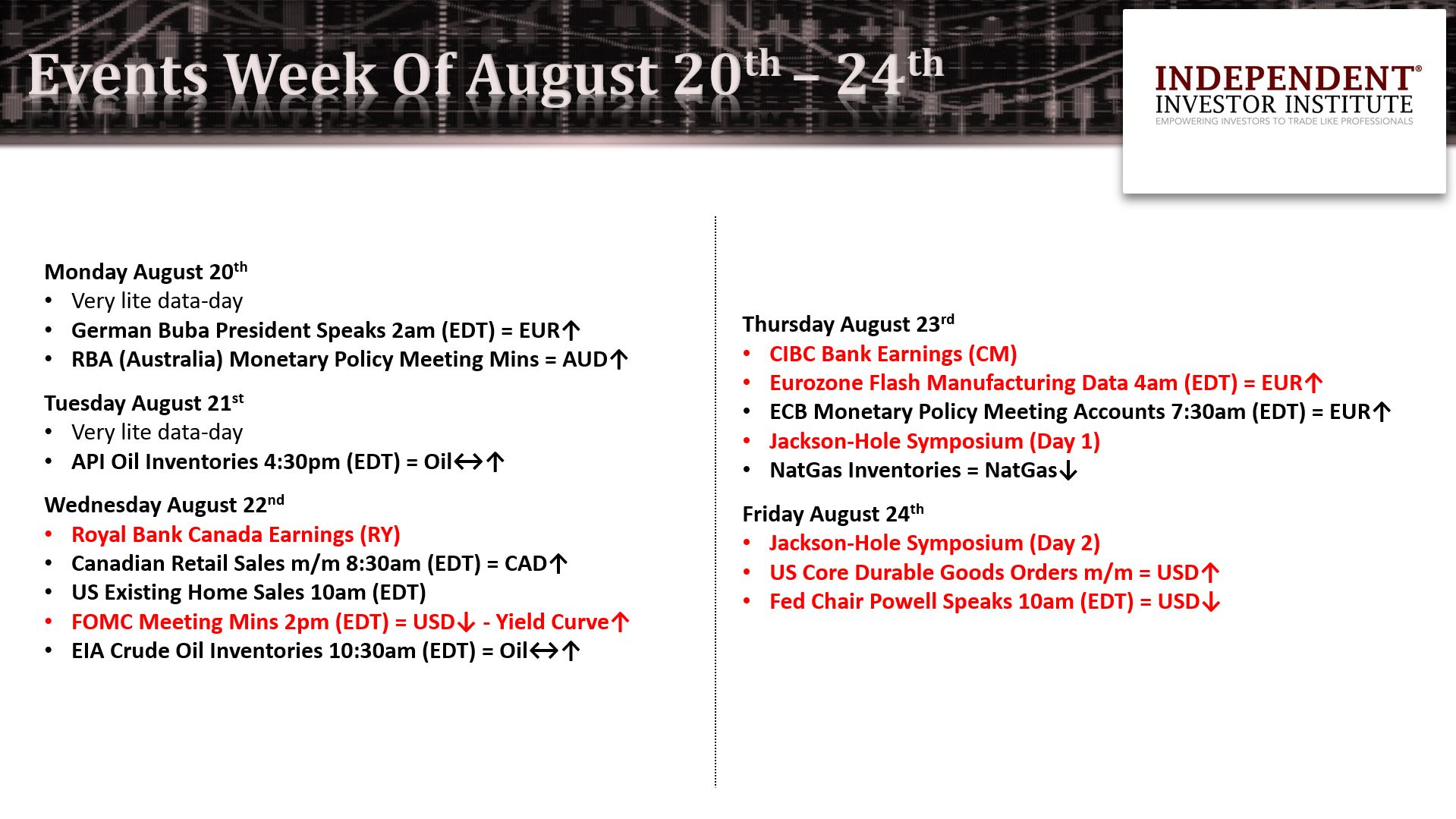

Short-to-mid-term swing-traders will be guided this week via our online coaching sessions as to whether we can stick with our pick-ups from August 17 or we will be forced to join the Dark Side (short), writes Ziad Jasani Sunday. He’s presenting at MoneyShow Toronto.

View my Market Strategy Session video here:

Recorded: August 17, 2018.

Duration: 1:29:31

Swing traders are concerned entering the back half of August 2018. Here are a few of the issues we’re grappling with:

1. Is there any reason for the negative-feedback loop between USD ↑ - Emerging Markets ↓ to end? Will the FOMC Meeting Minutes lean more hawkish this week? Will Jackson Hole be about U.S. confidence or coordinated global-central-banking policy?

2. Has there been any real change/improvement to the growth outlook (globally)? Has the recent out-performance in Value/Defensives vs Cyclicals answered that question?

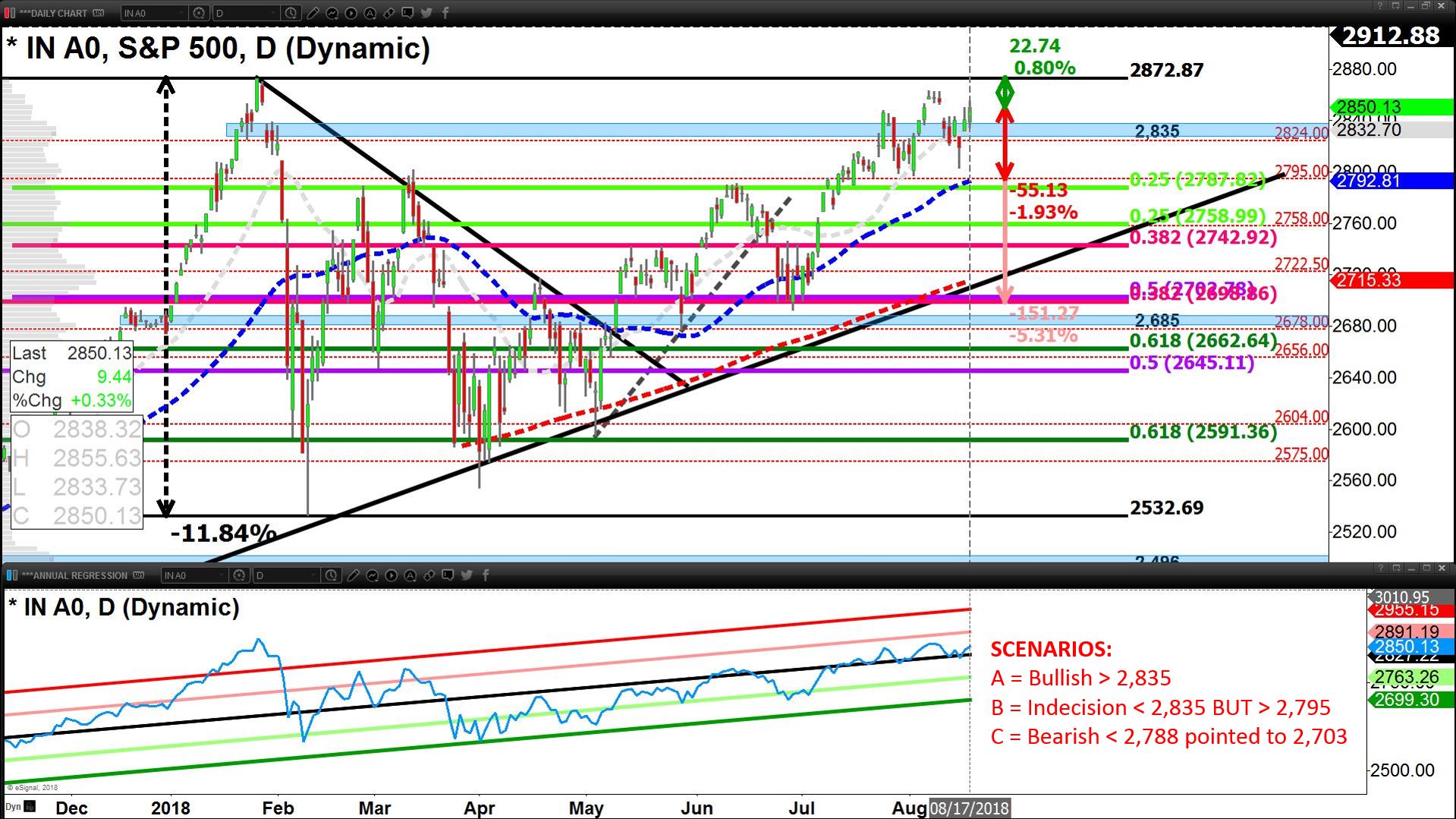

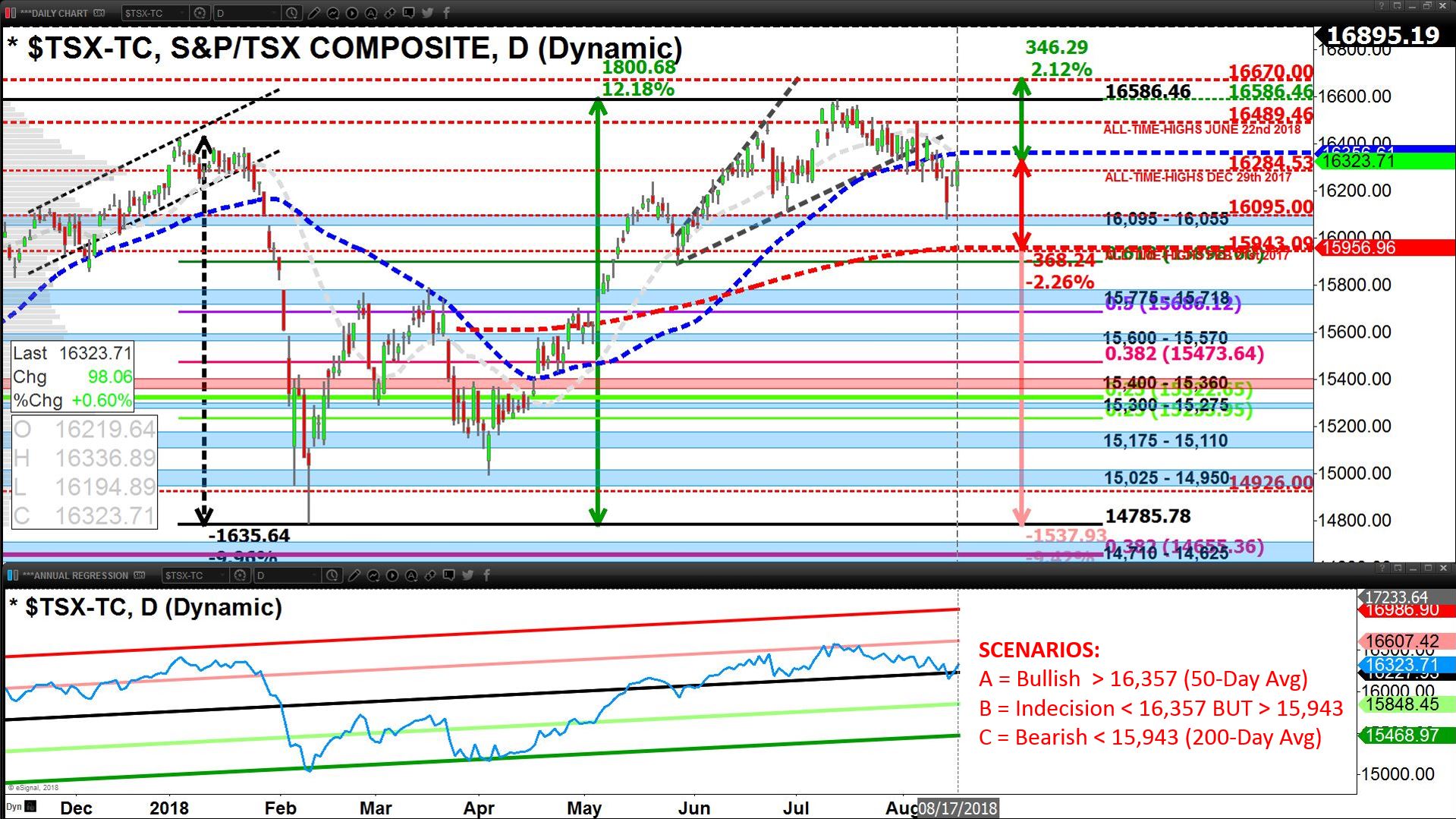

3. Was the turnaround on Friday, August 17 too perfect for swing traders? Since the reversal on August 15, we have been carefully evaluating whether we should simply continue to Hold our short-to-mid-term swing trades (long) or build on them.

Being so close to all-time-highs and seeing concerted outperformance from Defensives, reduced our confidence to Buy until August 17 when more news of the China-U.S. summit on trade (November) came out at 1:55 pm (EDT). The news created a sharp turnaround in the shape of the US-Treasury yield curve (steepened), cracked the USD down -0.5%, shot Commodities up (DBC, DBB), and tilted flows to the World-Ex-US (ACWX, EFA, EEM) alongside the trade-war related spaces in North America (DIA, XLI, XLB, XME, GDX, SIL, XMA-T, XGD-T).

The steeper yield curve allowed Financials to shine (XLF, KBE, KRE, KIE, XFN-T, ZEB-T, ZWBT). Oil perked up and got the pumps primed for Energy Equities to bounce (XLE, XEG-T).

However, Technology (QQQ, XLK, IYW) and Discretionaries (XLY) lagged.

We chose to leg into the aforementioned spaces as “all the stars were aligned” to support a short-term rise in prices. We enter this week knowing full well, that Equities are over-valued, this market is overly headline-sensitive, and the two weeks ahead are some of the most illiquid of the year.

Hence, all positions are short-leashes. However, the setup that triggered on August 17 for the USD to keep weakening, and the U.S. Treasury yield curve to steepen over the next week is compelling, which in-turn created swing-trading opportunity in Cyclical Sectors, Commodities and Equity Markets outside of North-America.

The short-term relative-expense of Defensive (Bonds, Utilities, REITs, Staples, Telecoms) and relative-cheapness of Cyclicals adds to the picture.

The reality that global growth is decelerating, Equity valuations are super-expensive, and that the U.S. Federal Reserve has “no good reason” to pivot less-hawkish continue to stare us in the eye, making every Buy decision more and more difficult.

Short-to-mid-term swing-traders will be guided through this week via our LiveOnline-Coaching sessions as to whether we can stick with our pick-ups from August 17 or whether we will be forced to join the Dark-Side (short); it actually comes down to the tone of the Jackson Hole symposium (ideally less-hawkish) and trade war-related headlines (furthering a truce between U.S.-China).

Join Ziad at MoneyShow Toronto Sept. 15 when he discusses Portfolio Management Strategies for Active Investors. Information: ZiadJasani.TorontoMoneyShow.com