Either way we slice it, it likely boils down to a statement from Powell that suggests growth risks are here. The question we’ll need answered: will a weaker USD and lower yields be enough to keep interest in Emerging Markets (EEM) and Int, Developed Markets (EFA) going.

View my Market Strategy Session for this week here.

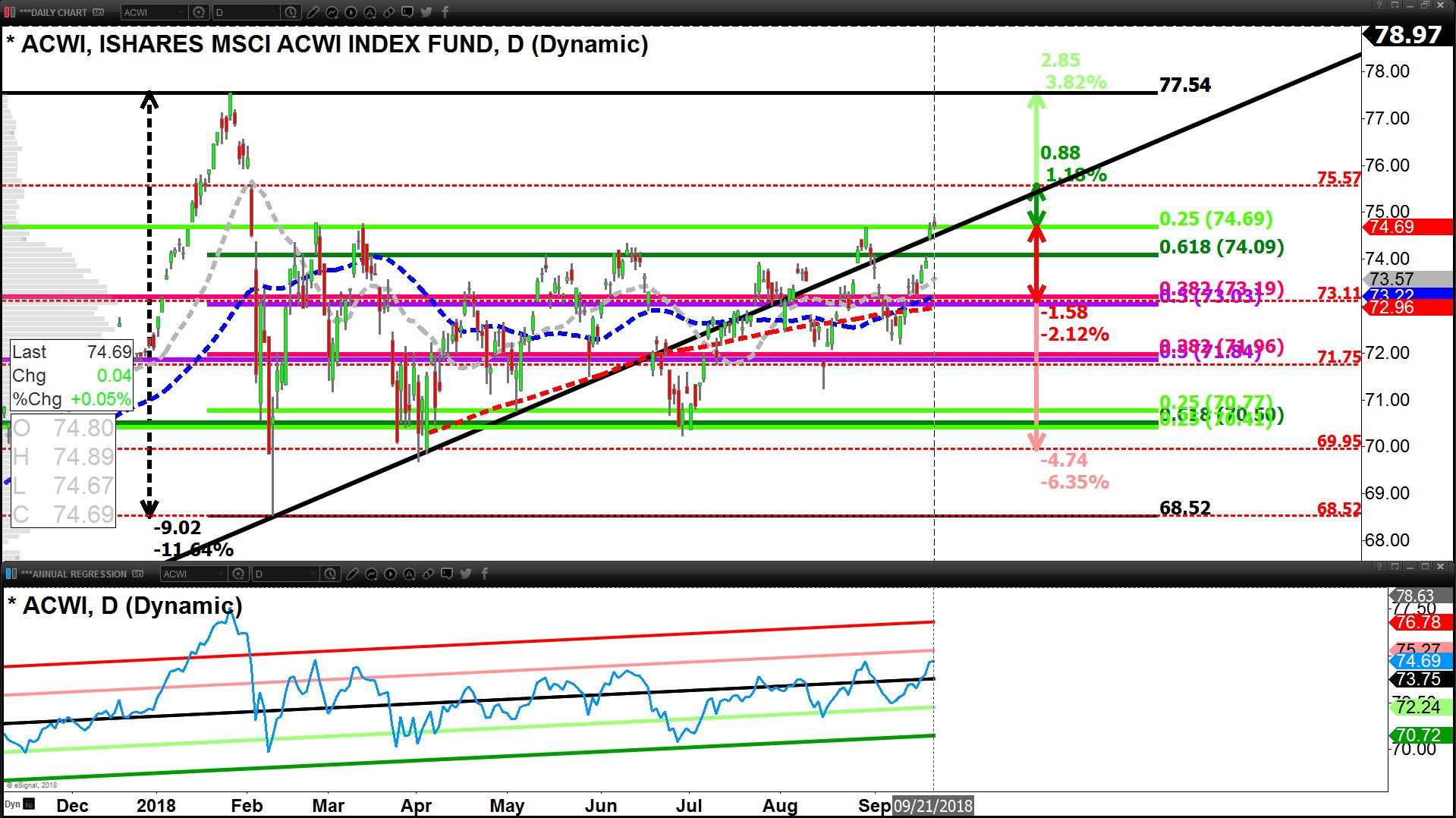

Recorded: Sept. 21, 2018.

Duration: 1:39:55.

Commodity-Market set-up into the FOMC statement

• Dr. Copper (CPER) and related equities took-off into the end of last week, tied to the out-performance we’ve seen from Emerging Markets (EEM). However, Copper did close into resistance of $2.84 forcing us out of longs; a break above points it up to $2.93 otherwise expect a retest of the 50-day average ($2.72); with markets jittery ahead of the Fed we expect the latter

• Oil was slammed down by Trump on Thursday Sept. 20 as he pumped out headlines to manage prices at pumps before midterms. Despite a slight rise on Sept. 21 Oil remained in a 3-candle bearish reversal pattern suggesting to remain short (HOD-T, SCO) while WTI Crude stays below $71.81; above this level a rise to ~$73 is more likely before a more pronounced decline

• Precious Metals (Gold, Silver) held support despite a rising USD (Gold support $1,202-$1,197, Silver $14.13); Wednesday will be Decision Day on precious metals and the backdrop is more positive than negative

• Natural Gas gave us a great bounce last week up to resistance at $2.99 but it remained under to close the week; we closed our HNU-T position. A break above $2.99 implies a move to $3.05 or higher ($3.12); a break below $2.92 implies a move to $2.79

• From a longer-term perspective Commodities are over-valued (regressions against equities back to 2009). From a shorter-term perspective Commodities are cheaper readying to continue the bounce starting on Sept. 7: DBC vs. ACWI (DBC Global Commodity-Complex vs. ACWI Global Equity Market).

The most important Commodity of the bunch, Oil, remains in a bullish pattern, however is likely to be manipulated lower into midterm elections.

• Commodity Summary: This week we see Oil inventories as negative for price action, but it’s all about Fed-Day Sept. 26. If Powell is less hawkish and the USD weakens, the current -82% correlation between Oil/USD would create a pop higher (HOU-T, UCO).

Otherwise we can easily see a re-test of the 200-day average ($65.92) (HOD-T, SCO).

Precious Metals are going get a lot shinier if Powell is less hawkish, we’re getting ready to play the oversold precious metals market long on Sept. 26. (GLD, UGLD, SLV, USLV, GDX, SIL, XGD-T).

While the Global Commodity Market (DBC) remains above its 200-day average ($17.09) we’re net-bullish commodities in the short-to-mid-term (week-to-a-month) but we note the long-term up-trend channel broke, hence we’re going to keep playing swings vs. being invested.

Bond-Market & Defensives set-up into the FOMC statement

• As Government Bond yields confirmed swing-high formations (10-year Treasury yield) to end last week we saw the Global Bond Market bounce up off an incredibly important support structure with long-duration Government Bonds leading the way (TLT).

We got long Bonds (TLT, LQD, XBB-T) and Preferreds (PFF, CPD-T) on Sept. 20 and will maintain positions into Fed-Day Wednesday with the goal being to build our positions. However, Jerome Powell and Mr. Market must give us weaker Government bond yields.

The current chart-setup on the 10-year and 30-year Treasury yield suggests a higher probability for yields to keep pointed down through Fed-Day.

• The recent “rotation” we’ve seeing into Defensives (Bonds, Utilities, Staples, REITs, Telecoms, Healthcare) has been underpinned by a weaker global growth outlook driven by Trump’s trade war, combined with inflation metrics remaining at bay.

Investors have prized Defensive/Value Equity Sectors (IVE, XLU, XLP, IYZ) much more so than Growth-Based Equity-Spaces (IVW, QQQ, IWM) and Long-Duration Government Bonds (TLT v SPY, TLT Long-Term Regression).

This leaves us with two key implications: Long Duration Government Bonds are readying for a bounce, but Defensive Equity Sectors are less likely to participate. Which in turn dampens the idea that Powell can engender a “total reflation rally” akin to Janet Yellen’s from early-2016 (Shanghai-Accord).

• Bond Market Summary: The Global-Bond-Market (BND + BNDX) is holding above a key long-term support structure, where if broken, can easily destabilize the Global Equity Market (ACWI); this outcome is likely if Mr. Market perceives Powell’s Wednesday statement as more hawkish than the last. This known-fact makes it more likely that Bonds bounce this week and yields continue to tilt down.

Add to this that the Global-Bond-Market is dislocated and cheap relative to U.S.-Value-Based-Defensive Equity Sectors (BND+BNDX vs. IVE) and we’re likely to see a rotation out of sectors like Utilities, REITs & Telecoms in favor for long-duration government bonds (TLT) this week (XLU vs. TLT).

Global Currency Market Summary: Will Powell keep markets thinking growth is good and inflation isn’t a concern? Or will he admit that growth risks are here and inflation isn’t coming?

Currency market charts suggest that the yen is readying to gain against the USD (USD/JPY), euro (EUR/USD) and Swiss franc (CHF/JPY).

This implies the message we hear Wednesday introduces “growth-risks,” and we’re readying to buy the Japanese yen (FXY).

• If the USD weakens from Powell’s statement Commodities (DBC) have a better than fair chance to bounce, however, a statement that introduces growth-risks would effectively reduce the demand side of the commodity equation.

Hence, we’re not looking to engage with commodity-laden currencies, U.S. dollar/Canadian dollar (USD/CAD) and Aussie/U.S. dollar (AUD/USD).

Current chart formations suggest the $CAD (FXC) and Aussie$ (FXA) have a better chance of actually weakening this week. We are expecting a move back up to 1.302 to 1.306 on the USD/CAD.

• The most important currency pair in the USD Index (UUP) is the EUR/USD, which sits in a highly over-bought position and has reason to weaken (Eurozone PMI Data Sept. 21). However, a less-hawkish statement from Powell, would effectively engage the inverted head & shoulders pattern on the EUR/USD currency pair pointing it up to 1.1945 (200-day average).

We anticipate the EUR/USD to soften (i.e. stronger USD) in the front half of the week, but are looking for a strong bounce (i.e. stronger euro in the back-half of the week and even more so the week after.

The current oversold position of the USD Index (UUP) supports this thesis, and the break-down below the USD Index’s 50-day average supports the outlook for a stronger euro over the next two weeks.

Enjoy a complimentary-no-strings-attached 30-day subscription to Ziad Jasani’s Daily Insights. Simply send Ziad an email with FREE TRIAL in the subject: ziad.jasani@educatedtrader.com