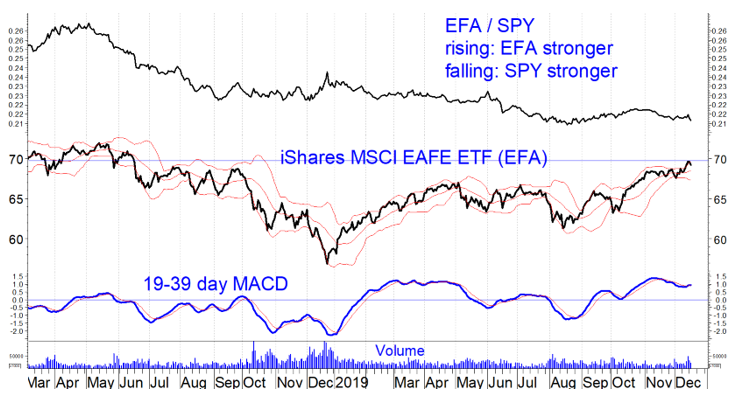

Equities are breaking out around the world despite muted optimism regarding economic growth in 2020. While U.S. stock indexes such as the S&P 500, Dow Jones Industrials and Nasdaq Composite are making record highs, other exchange trade funds (ETFs) are merely revisiting prior peaks. For example, the iShares MSCI EAFE ETF (EFA), which tracks non-U.S. developed markets made an 18-month high this week. The chart below shows that the EFA/ SPDR S&P 500 ETF Trust (SPY) ratio has very slightly risen since August, meaning that after a 12-year period of underperformance, EFA has been a bit stronger than SPY since Aug. 15.

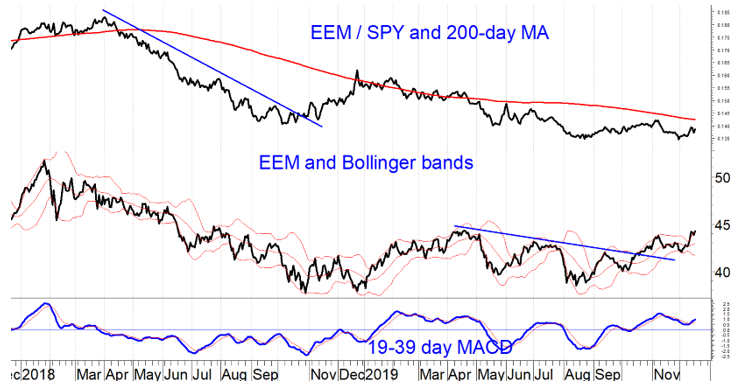

I have heard commentators project superior returns from European equities compared to U.S. in the years to come. That could be true, but for now there is scant technical evidence that either Europe or emerging markets is more attractive. We maintain a model that tracks the relative strength between the iShares MSCI Emerging Markets ETF (EEM) and SPY, and this model continues to favor SPY (see chart below).

Our international equity timing model remains on a sell signal while our U.S. equity timing model is on a buy. Bottom line: For now, stay with large-cap U.S. equities.

Figure: iShares MSCI Emerging Markets ETF (EEM), EEM/SPY ratio and 19-39-9 day (slow) MACD. As with other equity ETFs, EEM recently broke out. However, the EEM/SPY ratio has not changed much since August and remains below its 200-day moving average. This means that SPY is likely to outperform EEM.

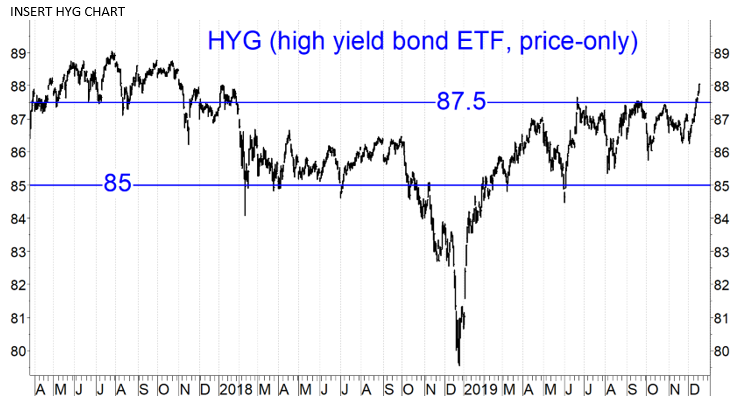

High yield bonds break out too

Corporate high yield bond prices have broken out to their highest levels since late 2018 as illustrated through the iShares iBoxx $ High Yield Corporate Bond ETF (HYG). Correspondingly, high yield bond spreads vs. Treasuries are at 3.6%, their highest level since 2008 as well (see chart below).

These developments are worrisome in that future potential returns from high yield bonds are likely to be relatively modest going forward, at least until after the next several-percent correction in that market. Below-average returns are what we saw from July 2017 through October 2018, when high yield spreads were about the same as they are now.

We recently decided to increase our clients’ allocation to short-term high yield bond funds. The initial impetus for this change was lagging performance by floating rate bond funds. However, I continue to favor short-term corporate high yield funds because of their historically greater safety when traded according to our timing models. During the July 2017 to October 2018 period, the SPDR Bbg Barclays Short Term High Yield Bond ETF (SJNK), a short-term high yield bond ETF, outperformed intermediate-term corporate high yield ETFs and mutual funds such as HYG, JNK, TDHIX, TGHNX and NNHIX.

Implications

“The market can remain irrational longer than you can remain solvent.”—John Maynard Keynes

Stocks and high yield bonds are not necessarily irrational, but they are priced for perfection. Fortunately, there are no storm clouds on the horizon. Our approach is to use trend-following methods to remain invested until technical evidence arises to suggest that a market correction may be at hand. Until then, we are keeping our clients invested, but in portfolios of below-maximal volatility.

Sign up here for a free three-month subscription to Dr. Marvin Appel’s Systems and Forecasts newsletter, published every other week with hotline access to the most current commentary. No further obligation.