The initial kneejerk reaction to the Fed announcement for a marginal taper was not met favorably by the Ten-Year Note, says Jeff Greenblatt of Lucas Wave International.

This is diametrically opposed to the stock market reaction, which was generally good. We are focused on the bond market today specifically because the recent low came in on the 144-day window to the April 5th low. It created a higher low, which is potentially bullish, but the pattern will need help in the form of buyers. Right now, we have a thrust off the low and a consolidation, which was not helped by Wednesday’s announcement.

The economy has been on one form of QE or another for over a decade. One has to think it has helped keep the ship afloat because it might be at the bottom of the sea without it. So much attention is being paid to the potential of rising rates, inflationary pressures, and stimulus. The challenge is extraordinarily little is being done for job creation or incentives to start new businesses. Small business generation has always been the economic engine but not now. We’ve experienced excellent job and small business growth in every business cycle at the very least dating back to 1913, which was the creation of the Fed in the first place. But with supply chain issues that is one of the causes of mounting inflation, the cost of just about everything is higher.

Longer-term interest rates are driven by what the crowd believes to be the risk associated with carrying those bonds. It is the cost of money. Obviously, some investors are looking at the longer-term aspect of risk. In coming to that decision, one has to decide if such issues (like inflation) are transitory or structural. Obviously, the Fed believes it's transitory. The supply-chain issue at the moment is likely transitory but that could change. What I’ve heard is many of the shipping companies sitting off the coast of California now have to leave to get paid and drop off their cargo in Florida. Somebody is going to have to pay for that and its going to be the consumer. Depending on how long this issue lasts will determine if the inflation aspect of the supply-chain issue becomes structural. Once it becomes structural, we’ll go back to the bad old days of the 1970s. None of this is priced into the stock market. The employment situation based on mandates causing thousands to quit their jobs does not provide a safe harbor. Powell called the pandemic “an impediment to the labor supply.”

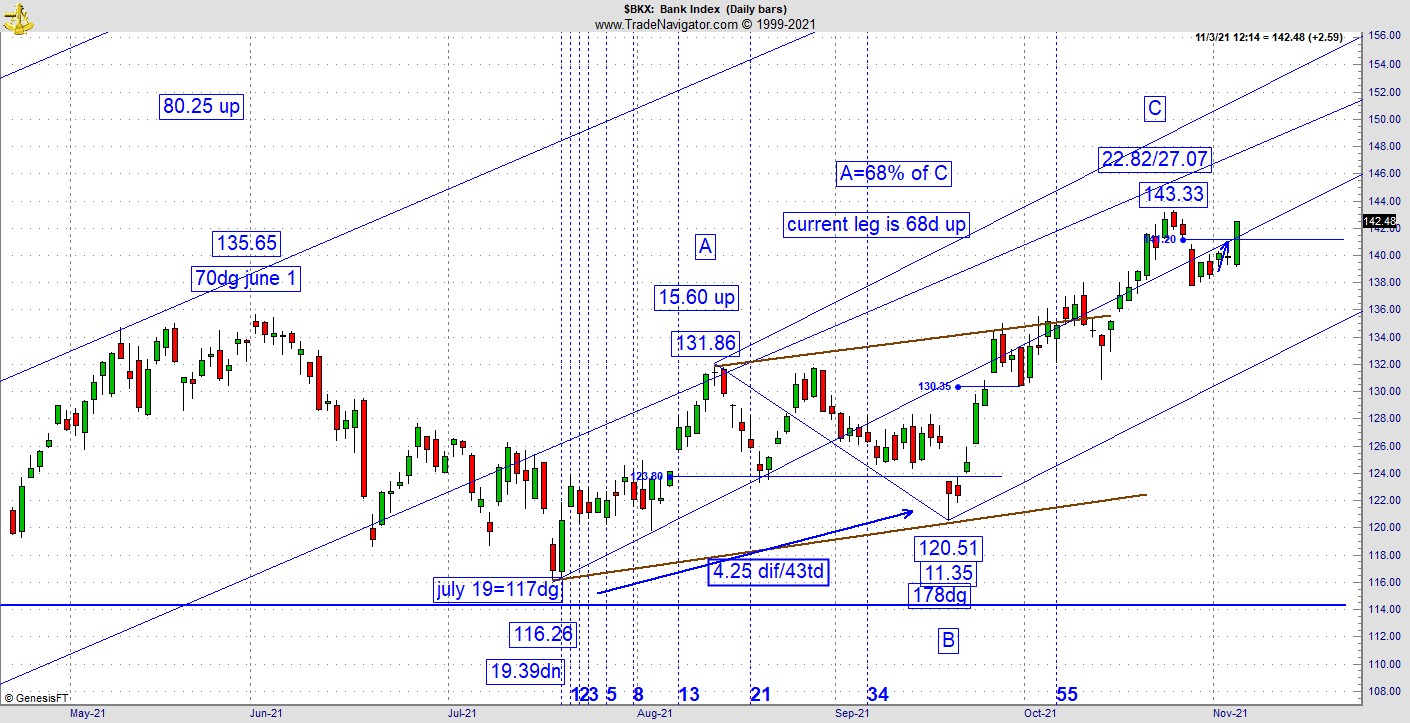

If the 144-day pivot low is taken out it could be a sign the bond market agrees with this assessment. But while the bond market might be flashing a yellow warning sign, the BKX showed initial enthusiasm for the announcement. What we are watching here is a sequence where the two legs up from the July low currently have a ratio where the first leg up (A) is 68% of the third and bigger leg up. By itself that doesn’t mean anything until you see the whole move up is 68 trading days. This cycle sequence caused a reaction in the form of a gap down. On Wednesday, the pattern more than filled the gap. Since the current high in the BKX falls in above the Andrews midline, a new high would mean the BKX is thriving where the path of least resistance is up. Obviously, some think the economy is sustainable. We are going to find out very soon how realistic this is.

On top of this, we are getting incredibly close to the holiday season, and one would be hard pressed to remember any year where there was no correction from early October thru Thanksgiving. The market should rally over the holiday season so if there is going to be a hiccup, seasonal factors suggest it should be soon.

We’ve now made it through September and October without a disaster, which is encouraging. Not even the US dollar got hit. But it’s the bond market that is flashing a warning signal. In terms of our work, the BKX was set up perfectly to drop. The highest probability point on the chart would’ve been for the pattern to fail right at the tip of the gap down. One way to look at the stock market’s reaction to the Fed is some believe the economy might be strong enough to finally wean itself off the decade-long stimulus. Markets should not be behaving this way; the problem is economic growth has not been organic as it’s been fueled by easy money since 2009. The question now is whether it can sustain in the face of so many issues including the 80-year war and revolutionary cycle. Most of what we see that offends us are symptoms of this 80-year cycle.

But the banks are not out of the woods yet. The recent high comes in on a very decent calculation and it looks like its going to have to be tested before we can see how the market wants to play its hand for the next sequence. I call them as I see them. This Fed announcement is a split decision. While the economy is better than it was a year ago, Powell is still concerned about Covid issues. The market started pulling back late Tuesday and couldn’t get any traction overnight as traders were obviously waiting on the Fed. An hour before Wednesday’s close, Dow futures were well above Tuesday’s high. While we have survived through September and October, it's highly questionable as to how much longer the stock market will be able to sustain. Right now, it’s best to think as a trader and not get too embedded on the long side.

For more information about Jeff Greenblatt, visit Lucaswaveinternational.com.