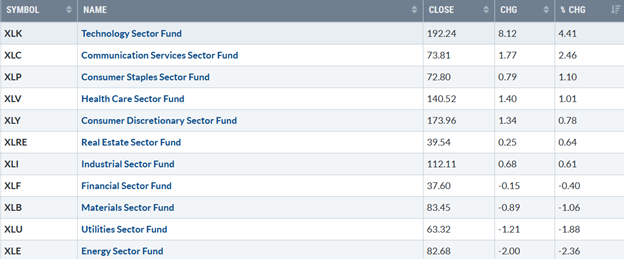

A resumption of the rally. Seven of the eleven S&P SPDR sectors were higher last week, notes Bonnie Gortler of bonniegortler.com.

Technology (XLK) and Communication Services (XLC) were the best sectors, while Utilities (XLU) and Energy (XLE) were the weakest. The SPDR S&P 500 ETF Trust (SPY) was up +1.87%.

S&P SPDR Sector ETFs Performance Summary 1/05/24-1/12/24

Source: Stockcharts.com

Figure 2: Bonnie’s ETFs Watch List Performance Summary 1/05/24-1/12/24

Source: Stockcharts.com

Semiconductors and Technology led the market. International markets were weaker than the US, with continued pressure on China.

Figure 3: UST 10YR Bond Yields Daily

Source: Stockcharts.com

The ten-year US Treasury yields fell last week, closing at 3.950%, above support at the middle channel (green line) and slightly above the downtrend line (green dotted) from October. Rising yields could lead to downside pressure in equities. On the other hand, falling yields could spark a short-term rally.

The major market averages rose, up the past nine out of ten weeks. The Dow rose +0.34%, the S&P 500 +1.84%, +0.3% from a record high, and the Nasdaq up +3.09%. The Russell 2000 Index lagged, down -0.01%.

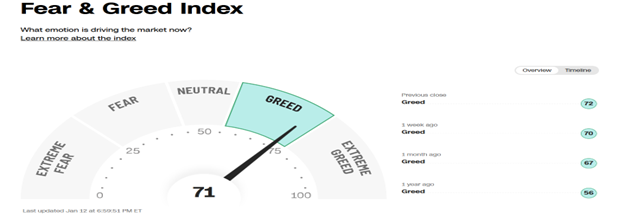

Figure 4: Fear & Greed Index

Source. CNN.com

Investor sentiment based on the Fear and Greed Index (a contrarian index) measures the market’s mood. The Fear and Greed Index closed at 71, down from 74, still showing greed.

Figure 5: Value Line Arithmetic Average

Source: Stockcharts.com

The Value Line Arithmetic Index ($VLE) is a mix of approximately 1700 stocks. VLE broke the October 2022 uptrend in early March 2023 (blue line), and April, May, and June successfully tested the March low and ultimately made a new low in October 2023. The daily trend of VLE shifted from up to down last week (pink circle). VLE gained +0.16%, closing at 9762.14, remaining above the rising 50-day MA (blue rectangle) and the 200-day MA (red rectangle), a sign of underlying strength. Support is 9700, 9400, and 9200. Resistance is at 9800 and 10200. It would be positive if VLE held support at 9700 and then turned up, surpassing this week's high of 9885.10.

Market Breadth Narrowed.

Weekly market breadth was positive on the New York Stock Exchange Index (NYSE) and negative on the Nasdaq. The NYSE had 1578 advances and 1351 declines, with 198 new highs and 67 new lows. There were 2312 advances and 2364 declines on the Nasdaq, with 81 new highs and 259 new lows. If you want to go more in-depth with charts, I invite you to join my Free Facebook group, "Wealth Through Market Charts".

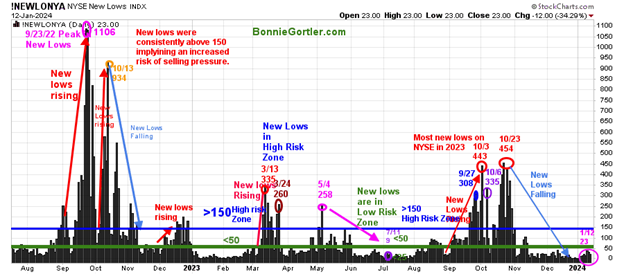

Figure 6: Daily New York Stock Exchange (NYSE) New Lows

Source: Stockcharts.com

Watching New Lows on the New York Stock Exchange is a simple technical tool that helps awareness of the immediate trend's direction. New lows warned of a potential sharp pullback, high volatility, and "panic selling" for most of 2022, closing above 150. The peak reading was 9/23/22 when New Lows made a new high of 1106 (pink circle), and New Lows expanded to their highest level in 2023 on 3/13/23 (red circle) to 335.

New Lows increased last September (red arrow on the right) toward the high-risk zone greater than 150, peaking at 443 on 10/3, the highest reading since October 2022.

New lows had stopped accelerating in early October. However, the decline was not complete until the end of the month as New Lows made only a slight new high, peaking at 454 (red circle) on 10/23/23.

Last week, New lows on the NYSE rose slightly, closing at 23 (pink circle) and remaining in the lowest risk zone below 25. It would remain positive and imply low risk if New Lows stay between 25 and 50. On the other hand, an increase above 150 would be a warning sign of a market correction. However, New Lows will likely take at least a few weeks to expand to greater than 150.

Learn more about the significance of New Lows in my book, Journey to Wealth, published on Amazon.

Figure 7: Daily iShares Russell 2000 (IWM) Price (Top) and 12-26-9 MACD (Middle and Money Flow (Bottom)

Source: Stockcharts.com

The top chart is the daily iShares Russell 2000 Index ETF (IWM), the benchmark for small-cap stocks, with a 50-Day Moving Average (MA) (blue line) and 200-Day Moving Average (MA) (red line) that traders watch and use to define trends. (IWM closed above both). IWM closed at 193.23, down -0.01% last week, remaining above the 50-day MA and the 200-day MA (blue rectangle), both rising, which is positive. Support is at 192.00, 187.50, 182.50, and 177.50. Resistance is at 197.50, 200.00, and 205.00.

MACD (middle chart) is on a sell, above zero, falling, and not yet oversold after reaching the highest momentum reading in December 2023. This implies underlying strength and the likelihood of another rally following once this latest pullback is complete.

Money Flow (lower chart) turned up slightly, remaining in a downtrend after breaking the uptrend (purple circle) from October. MFI is near 20, oversold, an area where rising money flow may begin again. A turn-up breaking the downtrend would be positive for the near term.

Look for a reflex rally this week toward first resistance at 197.50 and potentially more if IWM closes for two days above Friday’s high at 197.10.

Figure 8: Daily Semiconductors (SMH) (Top) and 12-26-9 MACD (Middle) and Money Flow (Bottom)

Source: Stockcharts.com

The top chart shows the Daily Semiconductors (SMH) ETF, concentrated mainly in US-based Mega-Cap Semiconductors companies. SMH tends to be a lead indicator for the market when investors are willing to take on increased risk and the opposite when the market is falling.

The Semiconductor ETF (SMH) was strong after underweight investors stepped in to buy, gaining +4.14% last week following the previous week’s weakness, keeping the short-term upside objective of 185.00 in play.

Support is at 165.00, 160.00, 140.00, and 135.00. Resistance is at last week's high of 174.14, followed by 176.75. MACD (middle chart) is on a sell, above zero, flattening, but not yet oversold where a fresh buy signal could occur. However, it may not reach an oversold level if SMH closes above 176.75. Money Flow (lower chart) is now rising after holding above the uptrend (purple line) but is not yet above the downtrend. If broken, it would be positive for Semiconductor stocks.

Figure 9: Daily Invesco QQQ Trust (QQQ) Price (Top) and 12-26-9 MACD (Bottom)

Source: Stockcharts.com

The chart shows the daily Invesco QQQ, an exchange-traded fund based on the Nasdaq 100 Index. QQQ made a low in October 2022 (red circle), followed by a successful retest of the low in early January 2023 and the start of an uptrend. Last week, Nasdaq 100 (QQQ) closed at 409.56, up +3.23%, remaining above the rising 50-day Moving Average (blue rectangle) and the 200-day Moving Average (red rectangle), a sign of underlying strength. Support is at 406.00, 400.00, 390.00, 380.00, 365.00, and 350.00, with resistance at 413.00, slightly above the high from 12/28/23. The bottom chart, MACD (12, 26, 9), is on a sell, above zero, and rising, remaining overbought. If support is between 400.00 and 406.00 holds, look for buyers to step in.

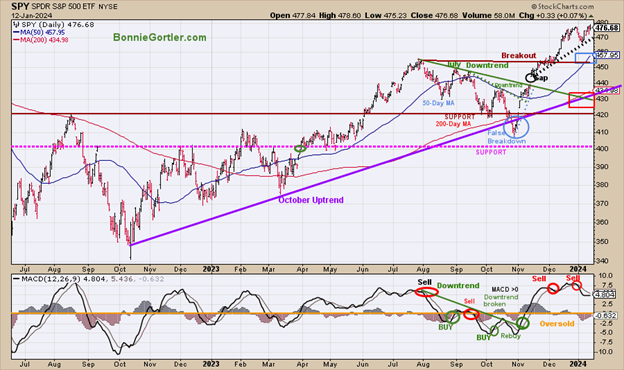

Figure 10: The S&P 500 Index (SPY) Daily (Top) and 12-26-9 MACD (Bottom)

Source: Stockcharts.com

The S&P 500 (SPY) had a false breakdown (blue circle) in October after being in an uptrend (purple line). Two downtrends were in effect and broken to the upside in September (green dotted line) and August (green solid line). The daily trend for the SPY remains up, with an upside objective of 485.00. The SPY closed at 476.68, up +1.87% for the week, remaining above the rising 50-day Moving Average (blue rectangle) and the 200-day Moving Average (red rectangle), a sign of strength. Support is at 470.00, 460.00, 440.00, 430.00, and 420.00. MACD (bottom chart) remains on a sell, above zero, and flattening. It would be a positive sign if support at 460.00 holds and SPY closes above last week's high of 478.60.

Figure 11: S&P 500 Bullish Percent Index

Source: Stockcharts.com

The Bullish Percent Index (BPI), developed by Abe Cohen in the 1950s, is a breadth indicator based on the number of stocks based on Point and Figure Buy signals. The indicator helps you know the market's health and when it's overbought or oversold. When the bullish percent index is above 70%, the market is overbought, and when the indicator is below 30%, the market is oversold. Like other overbought indicators, sometimes it does not get as high or as low.

In 2022 and 2023, the indicator reached 70 (overbought) six times (red circles). All occurrences were near market peaks (red lines). BPI fell from the peak reading of 81.00 on 12/29/23, closing at 74.20 on 1/12/24 (purple circle). A reading over 70, followed by a retracement below 70, would give a sell signal on this indicator. The S&P 500 Index (lower chart) closed at 4783.83, up +1.87% for the week. The October uptrend broke at the end of December (pink line). The S&P 500 support remains at 4600.

In Sum:

BPI remains on a buy. Past performance does not guarantee future results.

Summing Up:

The major averages have risen nine out of the past ten weeks, and Technology and Semiconductors were the best sectors last week. Market breadth is no longer improving on the New York Stock Exchange Index and Nasdaq. Daily momentum indicators have turned down from an overbought condition and have not yet formed a new low-risk buying pattern. Expect volatility as the bulls and bears battle for control in choppy trading this week, with more earnings released and option expiration on Friday. Continue to give the benefit of the doubt to the bulls if the S&P 500 is above 4600.

Remember to manage your risk, and your wealth will grow.

Let’s talk investing. You are invited to set up your Free 30-minute Wealth and Well-Being Strategy session by emailing me at Bonnie@BonnieGortler.com. I would love to schedule a call and connect with you.

Disclaimer: Although the information is made with a sincere effort for accuracy, it is not guaranteed that the information provided is a statement of fact. Nor can we guarantee the results of following any of the recommendations made herein. Readers are encouraged to meet with their own advisors to consider the suitability of investments for their own particular situations and the determination of their own risk levels. Past performance does not guarantee any future results