We have gone back into the pattern of seeing corrections last only one or two days, as sharp as they may be, with investors rotating into the broad market as the tech sector gets extended, despite remaining very strong, with no sign of abating, notes Ivan Martchev, investment strategist at Navellier & Associates.

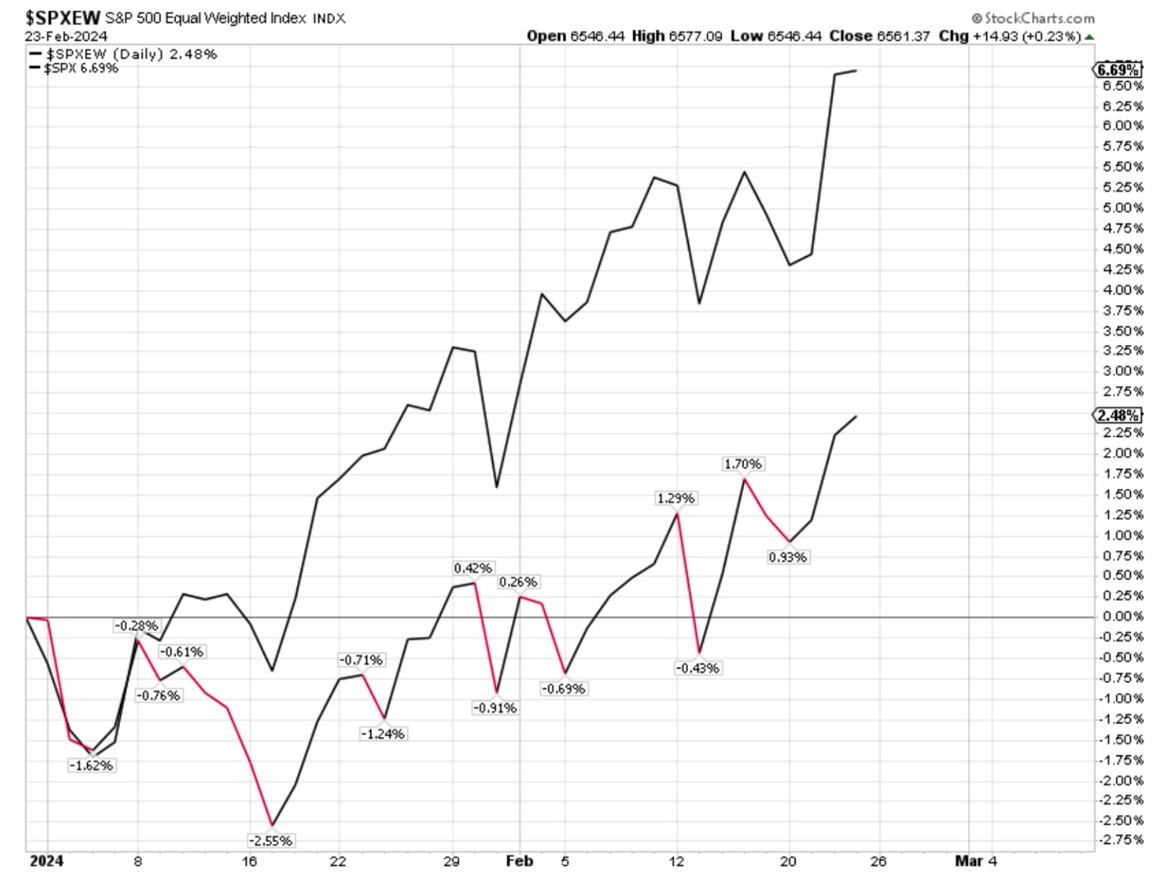

Notice the top line (below), representing the S&P 500 (SPX) Index, atop the line beneath it – the S&P 500 Equal Weight Index (SPXEW), representing the same components of the S&P 500 Index but not weighted by market cap (size). Two stocks make up about 14% of the market cap of the S&P 500 but only 0.4% of the SPXEW, as they are equal to all the other stocks in that index. The large performance differential you see below is basically due to the tech sector.

There was a big rotation into the broad market recently, with the Nasdaq 100 registering a fresh all-time high in the first 30 minutes of trading one day and basically going downhill for the rest of it. Before you begin to extrapolate this for the foreseeable future, the pattern has been that the tech sector gets overheated, it rotates for a day or two, and then starts chopping higher again.

There is no telling when we will get an intermediate-term correction. It is certainly due, but it can come from higher levels.

Meanwhile, I have heard the suggestion that tech is as extended as it was in early 2000. That is not the case. We have surging sales and earnings at the moment, and much lower valuations than we had in 2000, when we had only surging share prices. Nasdaq needs to more than double and possibly triple from here to get as frothy as 2000, which so far has not happened. We hope that won’t be the case, if we want this rally to continue.

The broadening of the market that we witnessed in November and December disappeared in January, but it began to come back at the end of February. So far, I view the glass as half full and I expect further gain for stocks, particularly if we see falling inflation data and Treasury yields that are behaved.