As we’ve been predicting in recent months, labor market conditions are improving, while inflationary pressures remain elevated. We expect the Federal Reserve will shift to a tightening bias at the June meeting and will probably hike the federal funds rate in July if current trends persist, notes Ed Yardeni, editor of Yardeni QuickTakes.

Don't get us wrong. We expect inflationary pressures to ease later this year, assuming, as we do, that the price of crude oil will settle between $75-$85 a barrel once the war in the Middle East has been resolved. Oil tankers are reportedly already passing through the Strait of Hormuz if their owners pay Iran's "toll."

(Editor’s Note: Ed is speaking at the 2026 MoneyShow Masters Symposium Las Vegas, scheduled for July 19-22. Click HERE to register.)

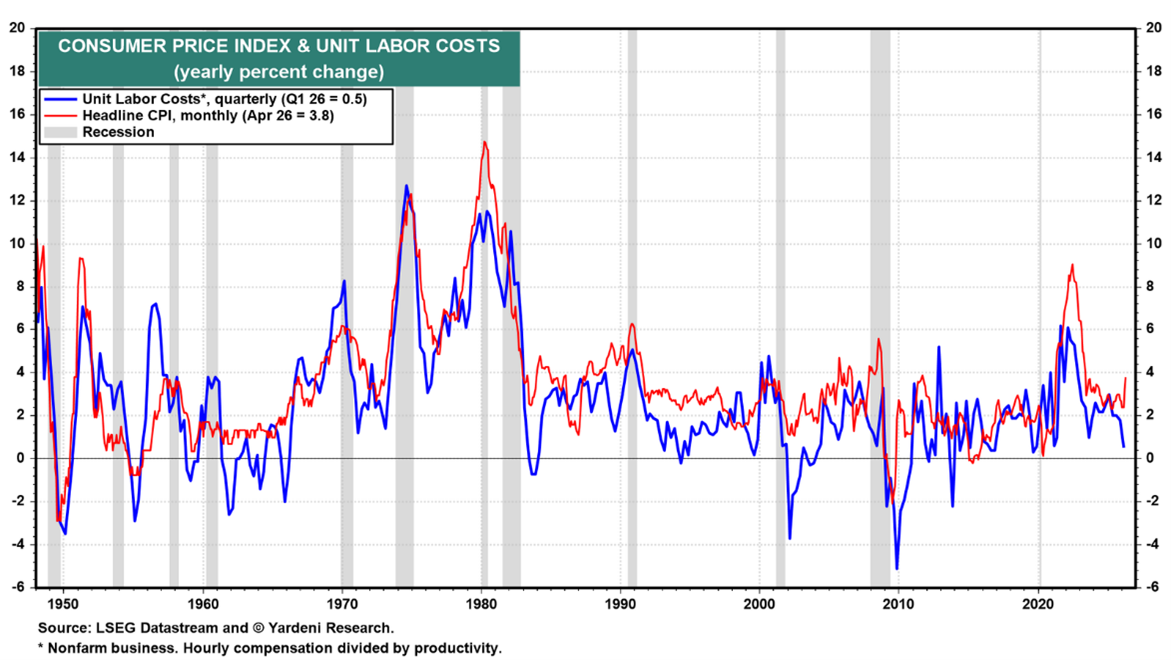

We are also counting on productivity growth to keep a lid on unit labor costs inflation (ULC). So far, so good.

Revisions for Q1 reduced the growth rates of both productivity and hourly compensation. Productivity is still up nicely at 2.8% year-over-year, while hourly compensation increased 3.3%. So ULC inflation is now down to just 0.5% YOY for Q1, as you can see in the chart.

This measure of the underlying inflation rate in the labor market is providing a strong disinflationary offset to the inflationary energy shock from the war. ULC inflation rose sharply during 2021 and 2022. The FOMC should pivot toward tightening monetary policy to avert a renewed wage-price spiral and to cool speculative excesses in the stock market.