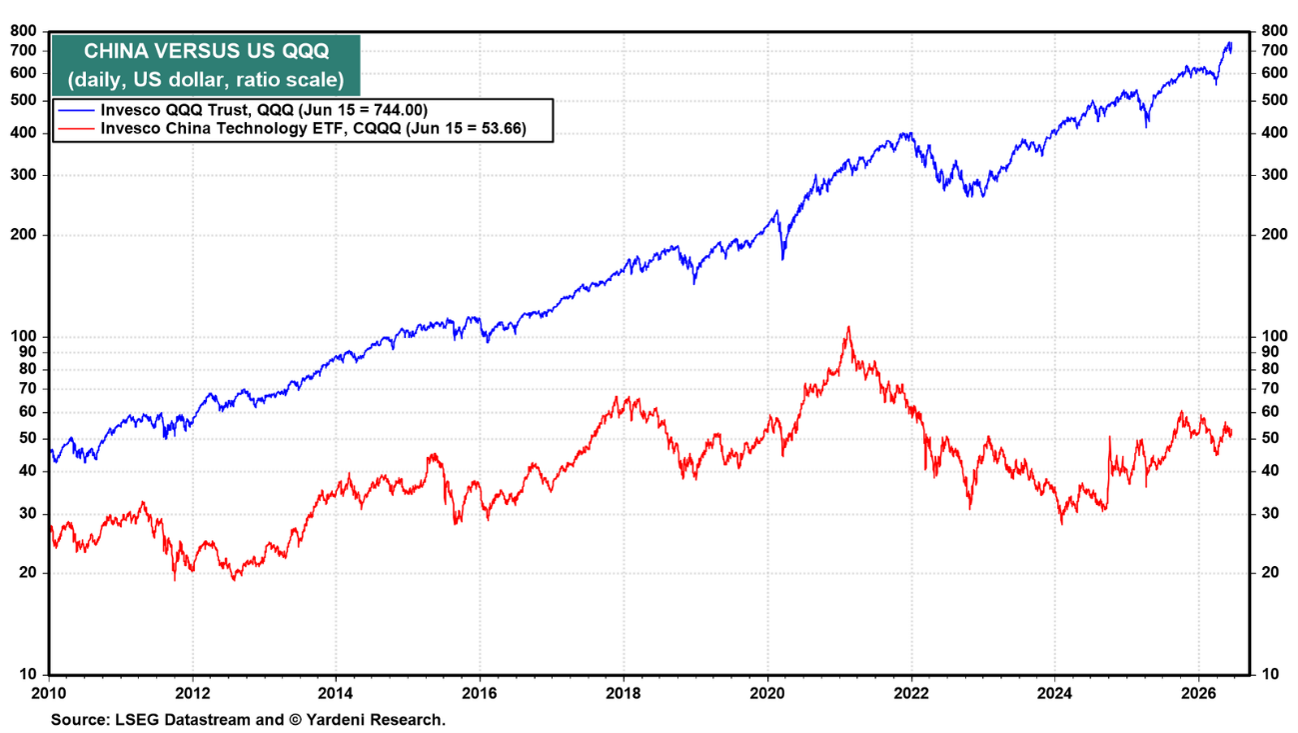

China has accomplished a great deal over the past few decades. Yet this miracle hasn't been reflected in China's stock market. Consider the underperformance visible in the Invesco China Technology ETF (CQQQ), which has been flat since the Great Financial Crisis, writes Ed Yardeni, editor of Yardeni QuickTakes.

China transformed from a poor, insular, rural economy to the world's second-largest economy. Its transformation has been hailed as an economic miracle. But over the same period the CQQQ languished, the US Invesco QQQ Trust (QQQ) is up seventeen-fold!

(Editor’s Note: Ed Yardeni is speaking at the 2026 MoneyShow Masters Symposium Las Vegas, scheduled for July 19-22. Click HERE to register.)

The divergence has occurred because China has an authoritarian command economy, while the US has an entrepreneurial capitalistic economy. US entrepreneurs are far freer to innovate, take risks, and prosper. Their Chinese counterparts operate under a government that tightly limits their freedom to run their enterprises optimally and to accumulate private wealth (and power).

Much of China's prosperity since the 1970s occurred during periods when the government allowed capitalism to flourish. Under President Xi Jinping, the government increasingly imposed authoritarian and arbitrary economic policies to maintain its control and to limit the power of entrepreneurs.

On the other hand, the government did nothing to stop the formation of a huge speculative bubble in the property market during the 2010s. When it burst, it caused a huge negative wealth effect that has been depressing consumer confidence and spending in recent years. Consumer confidence crashed during the pandemic in China and has yet to recover.

That negative wealth effect is evident in China's real retail sales growth, which has been declining on a year-over-year basis in recent years – and was down 1.2% in April. This is the first time real retail sales growth has been negative when excluding the pandemic years.

Sluggish domestic demand has, in turn, created significant excess industrial capacity. The weakness in China's domestic demand is further confirmed by bank loan growth, which dropped to 5.5% YOY in May, the lowest since 2001.