Even though everyone knows that the markets are unpredictable, that has not stopped investors from consistently searching to find a natural rhythm or seasonality to the market's ups and downs. The Globe Investor's Norman Rothery, has some new ideas about some familiar, old adages.

August brings a new crop of produce to my local farmers' market. This week, I feasted on sweet corn and I anticipate even better things to come when this year's harvest begins in earnest.

The change of the seasons affects many businesses besides farmers' markets. Retailers are a case in point. They have a habit of losing money for most of the year and then making it all back, and more, when shoppers surge into their stores at Christmas.

But the idea that stocks might also have a natural rhythm is a little more controversial. It's obvious that the market isn't perfectly correlated with the seasons, but research points to a weak relationship between the two that some investors might want to try exploiting.

One way is to follow the old adage that investors should “sell in May and go away.” It's a rule of thumb that has a very long pedigree. A 1935 article in the Financial Times referred to the rule as an ancient piece of advice even then.

The rule's persistence provides some evidence that it has been successful in practice, but those who want a more scientific assessment of the matter should turn to Ben Jacobsen and Cherry Y. Zhang of Massey University, New Zealand, who published an extensive study of the seasonality issue in a recent paper called The Halloween Indicator: Everywhere and All the Time.

They examined how an investor would have fared by buying stocks at the start of November, selling them at the start of May, and then repeating the process year after year.

Notably, their study didn't just focus on the US experience. Instead they employed long-term data from 108 of the world's stock markets.

They found that stocks returned an average of 4.53 percentage points more in the winter months than in the summer months from 1919 to 2011. Like many retailers, the markets generated small average losses of 0.18% in the summer, but they gained 4.35% in the winter.

The researchers also looked at truly long-term data from the UK covering almost 320 years. UK stocks gained 2.40% on average in the winter and lost 0.96% in the summer from 1693 to 2011.

You might be concerned that the long-term returns in this study seem rather modest, but you should be aware that they don't include dividends. Data on dividends tend to be rather spotty in historical databases, which prompted the researchers to stick with price data.

The inclusion of dividends in the return calculations would boost the returns in both the winter and summer months substantially, but it wouldn't likely favor the summer all that much. Indeed, the opposite might be the case, because annual dividend payers tend to send money to shareholders near the end of the year, during the winter months.

If you're like me, you're interested in how the home team fared. It turns out Canadian stocks gained an average of 5.29% since 1917 during the snowy season, and they lost 0.28% when the mosquitoes reign supreme.

However, following the sell-in-May approach isn't a surefire way to make money. In the UK, it failed to beat the simpler buy-and-hold method in about 37% of the years from 1693 to 2009. Over the more recent period from 1971 to 2009 it disappointed 38% of the time.

Given the short-term focus of many investors, several bad years in a row could easily dissuade them from the approach, even if it works over the long-term.

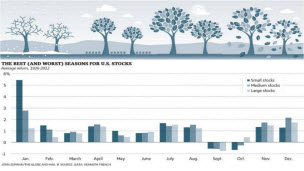

Nonetheless, the paper's tantalizing results prompted me to visit the database of US stock returns, compiled by Dartmouth professor Kenneth French, to get a better sense of how stock returns vary by month. Aside from providing a month-by-month breakdown, his return data include reinvested dividends and allows for a study of stocks by size.

The results can be seen in the accompanying graph, which shows the average monthly returns for US stocks from 1926 to 2012 based on three different portfolios. The first follows the largest 30% of stocks by market capitalization, the second tracks the 40% in the middle, and the third monitors the smallest 30%.

Click to Enlarge

As you can see, Professor French's data suggest that selling in May may not have been the optimal strategy over the period.

The market has done fairly well for most of the year, with the exception of a couple of months in the fall. September was the worst month, but medium and small stocks also saw declines in October. As a result, the idea of holding on until late August holds some appeal. It's also worth noting that the historical pattern suggests investors should start to grow cautious right about now.

(As an aside, the pattern of strong returns at the start of the year for smaller stocks is known as the January effect. It is thought to be largely caused by overly aggressive tax-loss selling of some small stocks late in the year. However, the data on small stocks tend to overlook the presence of large bid-ask spreads, which could make such gains hard to harvest in practice.)

Before you head off to try a little seasonal timing, it is important to point out that the foregoing results do not include trading costs, which may be significant.

Even worse, frequent trading brings joy to the taxman because it tends to trigger capital gains taxes in non-sheltered accounts.

Last but not least, only a few people are psychologically well-suited to such methods and can stick with them over the long term.

But it does make a buy-and-holder like myself think twice about loading up on shares in August. On the other hand, I'm hopeful that more cheap stocks will appear after it's possible to pick up a wee slice of pumpkin pie at the farmers' market.

Norman Rothery is the value investor for Globe Investor's Strategy Lab.