We recently welcomed the first grandchild, a granddaughter, into our family. A grandchild, especially an infant grandchild, has at least one substantial asset that the rest of us don’t, observes Bob Carlson, income expert and editor of Retirement Watch.

Time is working in favor of these youngsters. It’s too bad that people don’t come into the world knowing the power of compounded returns and determined to take advantage of it. Parents and grandparents can do their best to ensure the younger generations benefit from compounded returns.

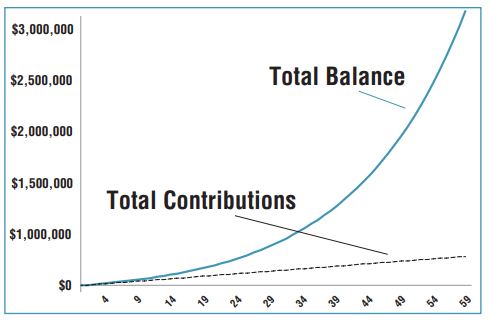

I put together the nearby chart to show how powerful compounded returns are. The chart assumes $5,000 is invested each year from birth through age 60. It also assumes a 6% annual return.

As you can see, as time goes by, compounded investment returns become a much larger share of the fund. By age 60, only $305,000 has been deposited, but the fund is worth just over $3 million.

The investment returns make up 90% of the fund. At age 40, investment returns are 77% of the total, and at age 30, returns make up 66% of the fund.

The younger a person is, the more work the markets will do for them. Real life results will differ a bit, because the money isn’t likely to be invested in something that earns a steady 6% annually.

The fund is more likely to be invested in assets like stocks that have good years and bad years, bull markets and bear markets. But over time, the basic results will be the same. The earlier a person starts investing, the more money the markets will deliver.

Show the chart to the youngsters in your life, or their parents, and ask if they want to let the markets make them millionaires or if they want to earn it the hard way.