Bob Savage discusses a possible extension of U.S.-China trade talk and U.S. Deficit.

Healing is a matter of time, but it is sometimes also a matter of opportunity - Hippocrates

Extra time sometimes makes for better outcomes. Tests are usually easier if you don’t have to rush, but trade negotiations might be different. Buying more time just makes the price of failure more expensive. We don’t know and won’t know now until April. Somewhere between the Trump 60-day extension to his trade deal deadline and the stronger Chinese export data, markets got bullish.

Throw in the Trump likely signing of the Congressional wall compromise funding, Japan’s Q4 GDP bounce back and you have nirvana for risk-takers, but they didn’t find much joy in Asia as it was seemingly already priced in. Brent crude oil is up 20% on the year as oil reflects the reborn faith in global growth and perhaps that explains some of the correlation, or perhaps more time isn’t a solution but for Europe which seemingly wins with the US/China trade story. Only problem is that the data from Europe is grim as the German economy only narrowly escaped a technical recession, as the Eurozone job growth slows and as the EU growth looks set for 1% in 2019. Markets are risk-on but not convincingly so as bonds are also bid making this a risk-parity day more passive than active to trade and wait for the US data. What seems most clear about markets is that FX is out of step with the bond and equity story. The USD is more bid than offered and the risk for JPY 112 or EUR 1.12 breaks seems in play today should the data support it. So perhaps we are back to diversity and correlations driving excess returns. For many this will be in the commodity linked currencies with the CAD the front line as it plays out the issues of the day with US trade, China and policy entwined. Watch 1.3130 or 1.3330 for larger confirmation of risk-on or off.

Are markets over the wall of worry?

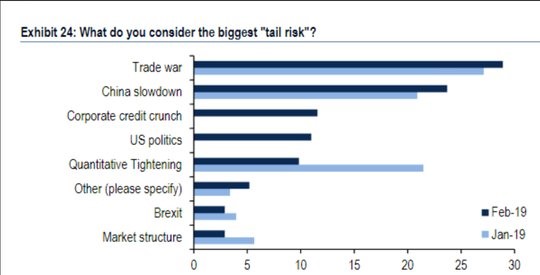

The Bank of America/Merrill Lynch investor survey for February was out this week and its worth checking the boxes to see if markets have managed to overcome all fears from January. The chart (below) makes clear that China growth and US-China trade talks are the giant issue still. The delay in getting this resolved maybe less helpful than headlines suggest. Markets are watching to see if the U.S. Government avoidance of a shutdown and the Trump push for a deal with Chinese President Xi will be sufficient to keep February worries at bay and extend the Q1 rally up in risk beyond the S&P 500 2800 resistance.

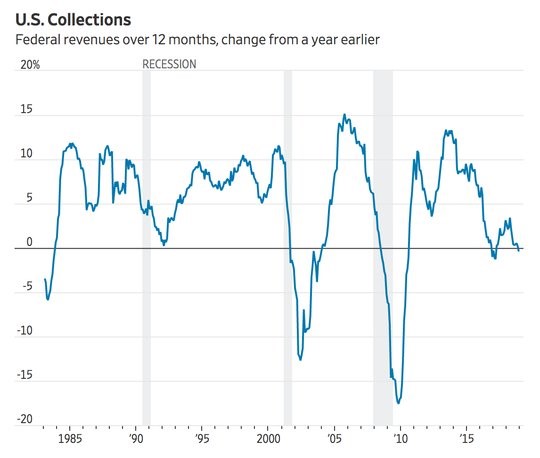

Is the US budget deficit the weak link in the USD chain?

The U.S. dollar bid is often questioned by those that watch the Current Account deficit. The U.S. budget deficit is problematic as it means the United States needs foreigners to fund itself or a more serious push to get U.S. savers to buy the debt. The data from the U.S. Treasury on the full 2017 tax reform effect isn’t encouraging as the revenues didn’t go up as some in the White House hoped claimed reported the Wall Street Journal (see chart). This means the deficit will remain a key issue for politics in the United States and in markets.