Today’s minutes poured cold water on a market that thought an interest rate cut was 10 times more likely than a rate hike, says Matt Weller.

Despite a powerful winter storm forcing the Federal Reserve’s Washington DC offices to close, the central bank was still able to release the minutes from its late January meeting.

The release hints at a more balanced outlook than the dovish reading from the meeting itself, with officials emphasizing an increase in downside risks to the economy, as well as generally strong household and labor market data. Beyond the general economic assessment, there were two key takeaways for traders moving forward.

Firstly, the minutes noted that “participants raised a number of questions about market reports that the Federal Reserve's balance sheet runoff and associated "quantitative tightening" had been an important factor contributing to the selloff in equity markets in the closing months of last year.” In other words, the “Powell Put” is alive and well; the Fed appears eager to adjust monetary policy if the central bank sees weakness in the stock market.

The second major takeaway revolves from the following passage: "Many participants observed that if uncertainty abated, the Committee would need to reassess the characterization of monetary policy as “patient” and might then use different statement language." These comments suggest that the Fed will look to remove the term patient from its statement before raising interest rates. While Chairman Powell will no doubt look to use his new press-conference-after-every-meeting policy to prepare markets for any changes to policy in advance, traders should also keep a close eye on the wording of the statement moving forward.

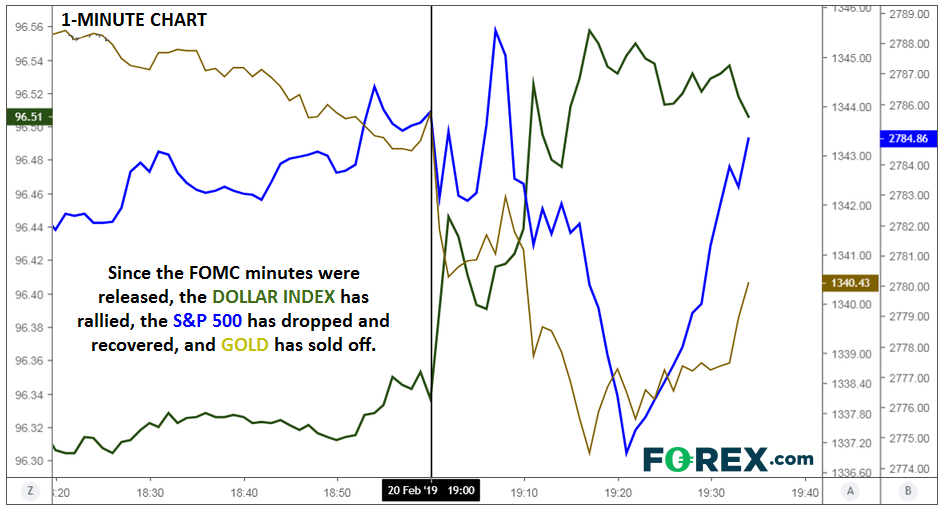

Market Reaction

Today’s minutes poured cold water on a market that thought an interest rate cut was 10 times more likely than a rate hike this year (though “no change” still seems the odds-on favorite). U.S. stock indices saw an intraday dip back to breakeven, the dollar index has turned back higher on the day, and gold is trading lower after four straight days of gains.

Intraday shifts aside, today’s minutes do not represent a major change in posture from the central bank; the Fed still remains neutral and data-dependent, with no changes likely until the latter half of the year. Therefore, markets may have already seen the majority of their adjustments to the new information already. Moving forward, geopolitical developments around US-China trade, the upcoming North Korea summit, Brexit, and EU auto tariffs will likely drive trade.

Source: TradingView, FOREX.com