“The early interpretation is that the Fed has shifted from a bias toward hiking interest rates to a completely neutral and data-dependent outlook,” says Matt Weller.

With seemingly every member of the Federal Reserve emphasizing that the central bank would be “patient” following its December interest rate hike, it came as no surprise that the Fed left interest rates unchanged today. And, despite the speculation that Chairman Jerome Powell and Company could revisit their balance sheet rundown strategy, the central bank was quiet on that front as well.

In other words, there were no surprise changes to monetary policy itself in today’s Fed meeting. That said, there were some interesting hints about how policymakers see monetary policy evolving over the rest of the year. The key changes to the FOMC statement follow (emphasis mine):

- Economic activity rising at a “solid” rate (downgrade from “strong)

- Added a clause acknowledging that “[M]arket-based measures of inflation compensation have moved lower in recent months…”

- Removed comment on “some further gradual increases” in interest rates

- Removed a sentence about “the risks to the economic outlook [being] roughly balanced”

- Indicated that the Committee will be “patient” in determining future “adjustments” to interest rates given “muted inflation pressures”

Here is the actual FOMC policy statement followed by a graphic showing how the statement was revised from the November FOMC statement:

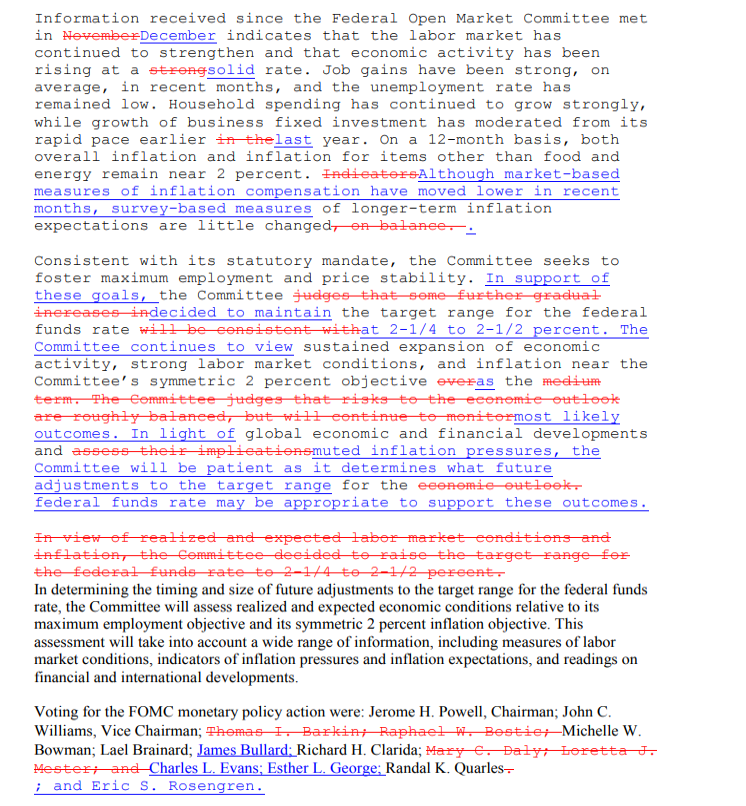

Information received since the Federal Open Market Committee met in December indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Job gains have been strong, on average, in recent months, and the unemployment rate has remained low. Household spending has continued to grow strongly, while growth of business fixed investment has moderated from its rapid pace earlier last year. On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Although market-based measures of inflation compensation have moved lower in recent months, survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent. The Committee continues to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2 percent objective as the most likely outcomes. In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support these outcomes.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were: Jerome H. Powell, Chairman; John C. Williams, Vice Chairman; Michelle W. Bowman; Lael Brainard; James Bullard; Richard H. Clarida; Charles L. Evans; Esther L. George; Randal K. Quarles; and Eric S. Rosengren.

Source: ForexLive

Did you catch that subtle-but-significant shift? In addition to emphasizing its patience moving forward, the FOMC also changed from assuming further increases to interest rates to future adjustments, leaving the door open for potential interest rate cuts if the economy deteriorates in the coming months and quarters.

That’s the big shift that traders have glommed onto, and that’s why we’ve seen a classic dovish reaction to the meeting in markets. Traders immediately bought bonds on the potential for lower interest rates, driving the yield curve down by 2-4 basis points across the curve. As a result, we’ve seen the U.S. dollar gain a quick 40-60 pips against most of its major rivals, while U.S. stock indices have rallied to fresh seven-week highs. Gold has tacked on a quick 10 points to trade at $1,325.

Fed Chair Powell is currently delivering his post-meeting press conference, and he is reinforcing the dovish message of the statement. Crucially, he confirmed a Wall Street Journal report from last week by noting that the Fed is evaluating its balance sheet plan and will be finalizing plans at the coming meetings. He also noted that the central bank’s portfolio will be normalized sooner and at a higher level than previously believed.

Essentially, the early interpretation is that the Fed has shifted from a bias toward hiking interest rates to a completely neutral and data-dependent outlook. This represents a major change in outlook from the central bank, and we wouldn’t be surprised to see ongoing weakness in the U.S. dollar and continued strength in stock indices as traders digest the significance of this shift.