I dropped a MoneyShow Video Market Minute on Friday about the “IPO Overload” – a scenario where the supply of initial and secondary stock offerings overwhelms demand, causing markets to roll over. Today, I’ll present the counterargument: It’s all relative.

Why talk about this at all? SK Hynix Inc. (SKHY) just sold $26.5 billion in shares on the Nasdaq, the biggest US listing by a foreign company ever. SpaceX (SPCX) sold $75 billion in shares a month earlier, the biggest IPO by any company, anywhere, EVER. Plus, a lengthening list of companies is looking to launch billion-dollar-plus deals later in 2026 and 2027. It all adds up!

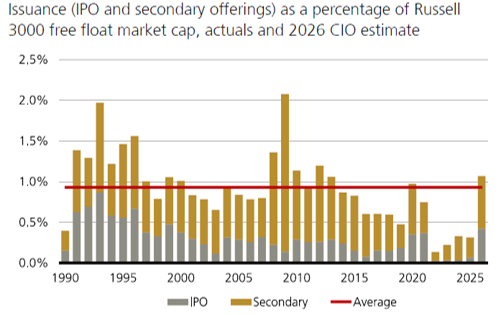

But take a look at the MoneyShow Chart of the Day, which comes courtesy of a deep-dive report from UBS Group AG (UBS) in late June. It compares UBS’ estimate of total issuance in 2026 to the total value of the US equity market (around $72 trillion). The firm also provides equivalent data for the last quarter century.

Total IPO and Secondary Volume / Total Stock Market Value

Source: Bloomberg, UBS

In THAT light, 2026 looks like a solid year for issuance – but NOT a wildly exuberant one. As UBS concludes: “From this perspective, we believe equity markets should be able to accommodate the increase in issuance.”

You can read the whole report to see what else UBS highlights, including still-elevated corporate stock buyback activity. That reduces the net supply of stock floating around in public markets. But the overall conclusion – “It’s all relative” – is worth noting.

Like I said in my video, it doesn’t look like we’ve reached a tipping point YET. Rather, you have to keep an eye on supply and market activity for signs we’re getting close. When we do, dialing down your stock market exposure will make sense.