Wall Street has been retreating and the S&P 500 Index (^SPX) is underwater. But the energy sector is still cruising ahead in 2026. Pembina Pipeline Corp. (PBA) is a stock I like here, observes Elliott Gue, editor of Energy and Income Advisor.

EIA Model Portfolio stocks are up almost 30% on average year-to-date, one of our fastest starts ever. And with the global (Brent) price of oil well over $100 a barrel, momentum is still running in our favor.

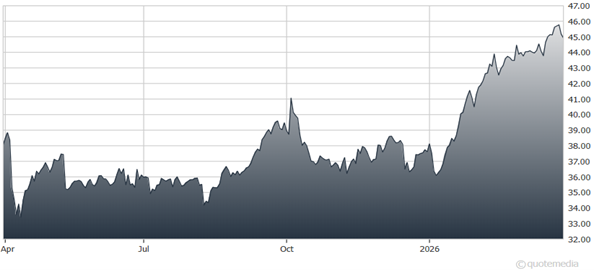

Pembina Pipeline Corp. (PBA)

How long will it continue? The fog of war is hanging over the global economy, and particularly the energy sector. We do know from QatarEnergy’s CEO Saad al-Kaabi that 17% of his country’s LNG export capacity has been demolished for the time being. And the Strait of Hormuz is closed, effectively shutting in whatever is still being produced. That’s bullish for global oil and LNG prices, and by extension energy companies that do most of their business outside the Middle East.

As for PBA, the Canadian midstream posted a 2.7% dip in 2025 EBITDA, near the mid-point of management guidance. Last year included a weaker comparison at its volatile energy marketing operations as energy prices were relatively steady. The company also had a new toll structure at the Alliance Pipeline that hit margins initially, but should boost them in coming years.

Overall, management expects to bring CAD 725 million of new infrastructure online in 2026, all under long-term “take or pay” (capacity-based) agreements that pay regardless of actual volumes. And the company reported successful re-contracting of existing assets as well. Canadian producers continue to ramp up output for export to Asia.

Management previously forecast a “lower contribution” from marketing operations on the expectation of softer commodity prices this year. That may be revised significantly upward due to recent events. But fee-based asset growth alone will fund low-to-mid-single digit percentage dividend increases.

Recommended Action: Buy PBA.