Comfort Systems USA Inc. (FIX) is riding the wave of the data center build-out to new record highs. This Zacks Rank #1 (Strong Buy) is expected to grow sales 31% in 2026. With strong earnings growth, rising estimates, and continued demand, this stock should be on your short list, notes Tracey Ryniec, senior stock strategist at Zacks Investment Research.

Comfort Systems provides commercial, industrial, and institutional heating, ventilation, air conditioning, and electrical contracting services. It has 197 locations in 143 cities across the United States.

On April 23, Comfort Systems reported first-quarter results and beat the Zacks Consensus by 46.2%. Earnings per share were $10.51, versus the $7.19 expected. This was the company’s fourteenth consecutive earnings beat.

Comfort Systems USA Inc. (FIX)

Revenue jumped to $2.9 billion from $1.8 billion in the first quarter of 2025. Organic revenue grew 51% year-over-year. Management remains optimistic, too, citing strong bookings, persistent demand, and a solid pipeline.

Following the earnings beat, analysts raised their full-year estimates. The 2026 Zacks Consensus EPS jumped to $43 from $35.10. That represents 49% earnings growth over 2025.

Estimates for 2027 are also moving higher. The 2027 consensus now stands at $51.40, up from $41. That implies an additional 19.4% rise.

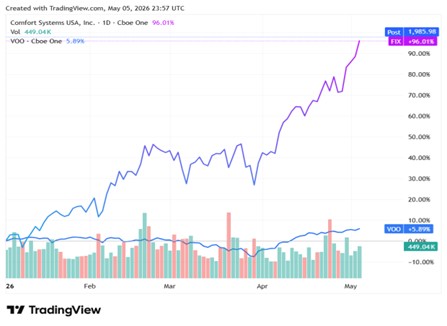

Shares of Comfort Systems USA hit new all-time highs in May, and are up 96% year-to-date. Over the last five years, the stock has gained 2,164%, easily outperforming the Vanguard S&P 500 ETF (VOO), which is up 71% over the same period.

For investors seeking exposure to the AI infrastructure build-out, Comfort Systems USA offers a compelling opportunity.