Market skeptics and commenters on social media will watch a single variable move in what they consider an unfavorable way, then jump to the conclusion that the stock market is in trouble. Consider the recent rally in long-term interest rates. That’s gotta be bad news for the stock market, right? Not necessarily, advises Sam Ro, editor of Tker.co.

Maybe the market eventually moves as they predicted. Sometimes that happens. But markets are complicated, and they’ll often move in counterintuitive ways.

Nick Colas, co-founder of DataTrek Research, just challenged the idea that rising rates automatically mean lower stock market valuations. From his note: “You have probably heard this sequence of statements many times: Long-term interest rates are increasing. This means that the present value of future cash flows is declining. Therefore, equity valuations should drop as well.“

Colas dismantled this oversimplification, flagging two big problems with the shoddy argument he just summarized.

“The first is that it doesn’t work in real life,” he wrote. “The second reason that yields and equity valuations move independently of each other comes down to discounted cash flow math.”

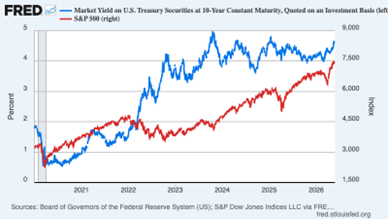

He pointed at 2015 to 2019, when the 10-year U.S. Treasury note yielded an average 2.27%. During that period, the forward price-to-earnings (P/E) ratio for the S&P 500 Index (^SPX) was between 15x and 18x earnings.

He then noted that as of last Wednesday, the 10-year yield was much higher at 4.49%, and yet the forward P/E was also much higher at 21x earnings. In short, the market didn’t do what some skeptics might’ve assumed.

But does this mean the stock market is irrational? No. The takeaway from his analysis is that an increase in interest rates is theoretically bad for valuations – if you don’t consider earnings growth.

“If interest rates go up two percentage points (as they have since 2020) but earnings growth expectations increase by 3%, then equity valuations actually increase,” he wrote.

It’s such a refreshingly simple observation that speaks to a massive mistake some short-sighted market prognosticators keep making. And that mistake is adjusting one variable in a complex formula while holding all other variables constant.