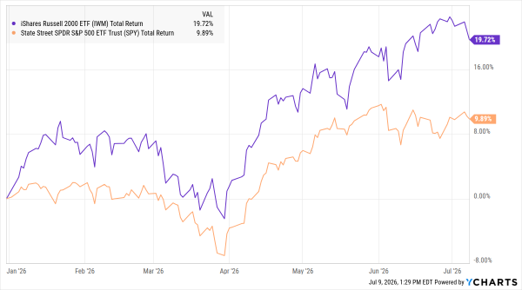

Small caps led the US market at the halfway point for the first time since 2021 – and only the second time in the past decade. Meanwhile, we believe the AI trade remains a long-term secular growth story, a view echoed in our recent Retail Investor Beat survey, writes Bret Kenwell, US investment analyst at eToro US.

The rally builds on the Russell 2000’s strong second half of 2025, when it also outpaced the S&P 500 Index (^SPX), Nasdaq, and Dow. That first-half leadership may be a bit surprising given the strength in AI and tech. It’s even more notable against a tense geopolitical backdrop and, more recently, rising expectations for higher rates.

IWM Vs. SPY (YTD % Change)

Data by YCharts

The strength ran deeper than the headline indexes. The equal-weight S&P 500 outperformed the traditional S&P 500 in a calendar half-year for the first time since the 2022 bear market. That happened even as the S&P 500 hit 20 intraday record highs in the second quarter – and only three sectors (tech, industrials, and health care) made new highs of their own.

Markets have been choppier since the Federal Reserve’s hawkish surprise in mid-June. But equities, especially small caps, have largely taken it in stride.

That resilience now faces a bigger test: earnings season. After a strong first half and a bumpier start to July, results and guidance will likely decide whether volatility sticks around or stability takes back the wheel.

As for retail investor study, it found that respondents believe tech looks overheated in the short term, but is positioned to outperform over the long term. Earnings will need to reinforce that growth narrative, though it may also be prudent for capital to rotate into other quality assets now trading closer to value territory.