While worldwide markets are being challenged by the backdrop of higher interest rates and ongoing conflicts in the Middle East and Ukraine, one thing has not changed. US stocks are more expensive than global stocks, notes John Eade, president of Argus Research.

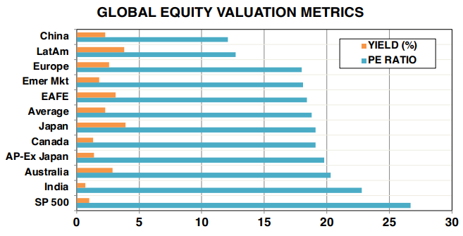

That’s the case even with the market-leading returns from global stocks in 2025-2026. Consider P/E ratios. The trailing P/E ratio on the S&P 500 Index (^SPX) is 27, above the global average of 19 and well above the 12-13 average P/Es for emerging markets stocks in China and Latin America.

A review of yields tells a similar story. The current dividend yield for the S&P 500 is 1%, versus the global average of 2.3% – and European and Latin American yields of 3%-4%.

Taking a step back, reasons that investors generally are willing to pay a higher price for North American securities include the transparency of the US financial system as well as the liquidity of US markets. What is more, global returns can be volatile across individual countries, given currency, security, political, and geopolitical risks.

Indeed, the SPDR S&P 500 ETF Trust (SPY) has outperformed the iShares MSCI EAFE ETF (EFA) over the past five years. But the tide turned a bit in 2025, as investors responded to the uncertainty over US trade policy and as global central banks lowered rates. Last year, foreign stocks were up 28% while US stocks rose 16%.

Meanwhile, the outperformance of emerging markets over domestic markets has continued in 2026. Given expectations for improving economic growth in Europe and Japan in the months ahead, we think that diversified investors should have 20%-25% of their equity allocations in international stocks to take advantage of the value -- and we have been adding global stocks to our universe of coverage.